A Look At Janus Henderson Group (NYSE:JHG) Valuation After A 1 Year Total Return Above 50%

Janus Henderson Group PLC JHG | 0.00 |

Janus Henderson Group (NYSE:JHG) stock is in focus after recent performance data showed a total return of 7.3% over the past 3 months and a 1-year total return above 50%.

The current share price of $51.64 comes after a 7.3% three-month share price return. The 1-year total shareholder return above 50% indicates sustained momentum rather than a short-term spike.

If you are looking beyond Janus Henderson Group and want more ideas with strong fundamentals, now could be a good time to scan the market using the 17 top founder-led companies

With Janus Henderson Group posting a 1-year total return above 50% and trading near its consensus analyst price target of $52.67, you have to ask: is there real value left here, or is the market already pricing in future growth?

Most Popular Narrative: 24.6% Overvalued

According to the most followed narrative, Janus Henderson Group's fair value of $41.45 sits well below the last close at $51.64. This frames that recent 1-year return of more than 50% in a very different light.

For investors, JHG is best viewed as a balance-sheet story rather than a growth narrative. If Jackson continues to manage risk conservatively while returning capital responsibly, it can remain relevant, and valuable, even as the insurance system adjusts to new economic and legal realities.

Curious what supports a higher fair value than a pure growth story would imply? The narrative leans heavily on earnings quality, measured profit margins, and a valuation multiple linked to those cash flows. The tension between steady capital returns and modest growth expectations sits at the core of that calculation.

Result: Fair Value of $41.45 (OVERVALUED)

However, this balance sheet focused case can be tested if earnings quality weakens or if market sentiment shifts away from asset managers toward other financial stocks.

Another View: Market Pricing vs Cash Flow Value

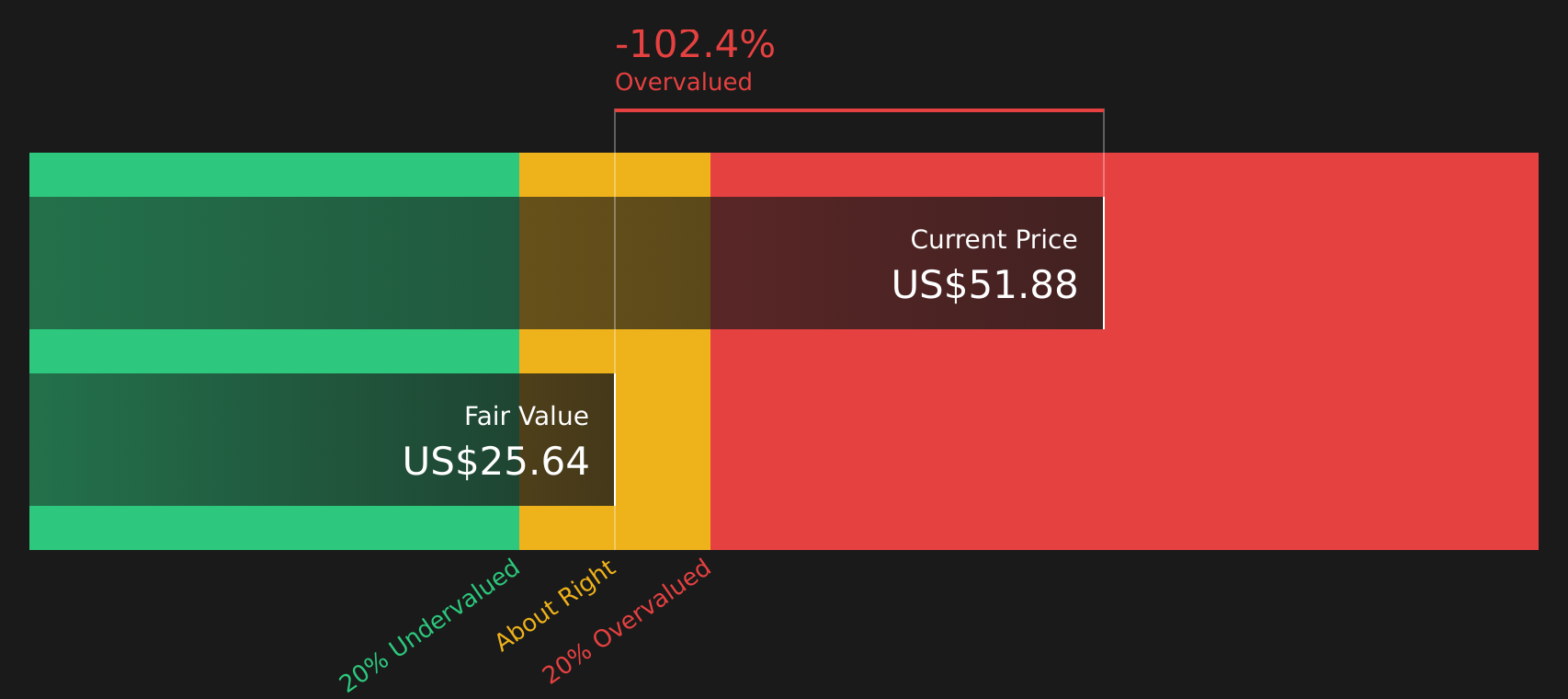

That 24.6% overvaluation call comes from a narrative fair value of $41.45, but the SWS DCF model paints an even tougher picture. On future cash flows, JHG at $51.64 screens as overvalued against an estimated value of $31.75, which raises the question: what exactly is the market paying up for here?

Next Steps

The mix of strong recent returns and mixed valuation signals makes this a stock where opinions can differ. It is worth looking through the details yourself and weighing both the optimism and the caution by starting with these 3 key rewards and 2 important warning signs.

Looking for more investment ideas?

If you stop with just one stock, you risk missing opportunities that could suit your goals even better, so broaden your watchlist before the market moves on.

- Target potential mispriced opportunities by checking companies that look attractively valued on cash flows and balance sheet strength through the 48 high quality undervalued stocks.

- Strengthen your income focus by reviewing stocks with yields above 5% and resilient payouts using the 12 dividend fortresses.

- Prioritise resilience by scanning companies with lower risk profiles and steadier fundamentals through the 70 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.