A Look At JetBlue Airways (JBLU) Valuation As Card Refresh And Fort Lauderdale Expansion Advance

JetBlue Airways Corporation JBLU | 0.00 |

Credit card refresh and Fort Lauderdale build out take center stage

JetBlue Airways (JBLU) has put its co branded JetBlue Premier World Elite Mastercard and Fort Lauderdale expansion at the heart of its current push to win and retain travelers after Spirit Airlines’ shutdown.

The card now offers larger statement credits, status related tile bonuses and a sizable limited time TrueBlue points offer. Fort Lauderdale is set to see new routes, added frequencies and targeted perks for former Spirit loyalty members.

JetBlue’s latest credit card refresh and Fort Lauderdale build out arrive as the share price trades at US$5.13, with a 7 day share price return of 10.20% and a 30 day share price return of 12.75%. However, a 90 day share price return of 19.34% decline and a 5 year total shareholder return of 72.93% decline underline that recent momentum comes after a long and difficult stretch for investors.

If this kind of repositioning has your attention, it can be a useful moment to see what else is changing in the market through 36 power grid technology and infrastructure stocks

With JetBlue shares still near US$5 despite recent gains and the stock trading below one valuation estimate, the key question now is whether investors are overlooking a potential turnaround or whether the market already reflects expectations for future growth.

Most Popular Narrative: 8.9% Overvalued

JetBlue’s most followed narrative pegs fair value at $4.71 per share, which sits below the current $5.13 price and frames a relatively demanding setup.

Fleet simplification and faster than expected resolution of grounded aircraft will enable JetBlue to resume low single digit capacity growth with minimal capital outlay starting in 2026, improving unit costs and providing margin expansion as operating leverage returns.

Curious what has to go right for that to hold up? The narrative focuses on steady revenue growth, slimmer losses and a richer earnings multiple. The exact hurdles are worth seeing.

Result: Fair Value of $4.71 (OVERVALUED)

However, that fair value narrative still leans on assumptions that could be challenged if fuel costs stay higher for longer or if labor and competitive pressures squeeze margins.

Another View: Cash Flows Point In The Opposite Direction

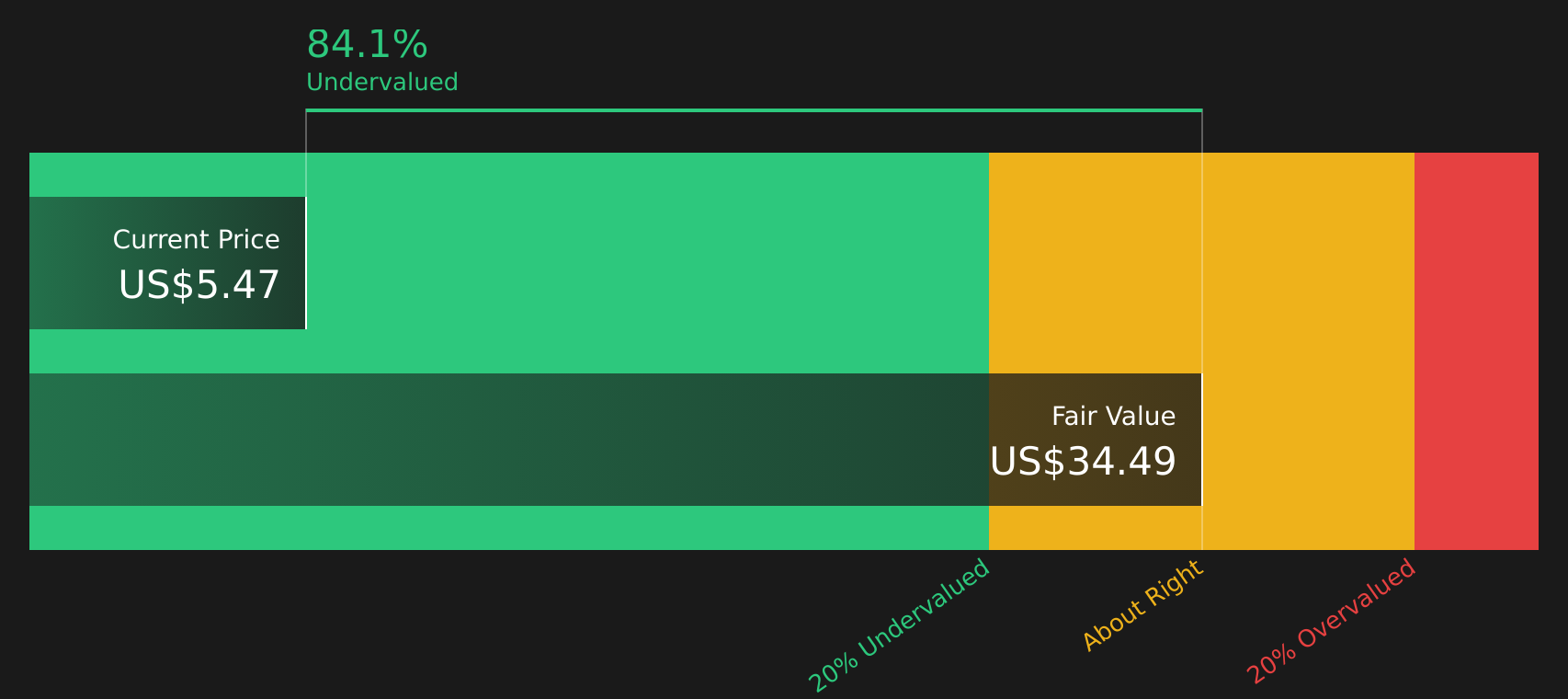

While the analyst narrative flags JetBlue as 8.9% overvalued at $4.71, the Simply Wall St DCF model paints a very different picture, with a fair value estimate of $34.49 per share. That is a very large gap. Which set of assumptions do you find more realistic for the next few years?

Next Steps

Given the mixed signals throughout this story, it makes sense to move quickly and test the assumptions yourself using the 2 key rewards and 2 important warning signs.

Looking for more investment ideas?

Do not stop with a single stock. Use this moment to scan across sectors, compare quality and risk, and line up the next opportunities on your watchlist.

- Target potential upside by reviewing companies flagged as 51 high quality undervalued stocks that may offer a gap between market price and fundamentals.

- Prioritize resilience by focusing on solid balance sheet and fundamentals stocks screener (44 results) to see businesses with stronger financial footing and fewer balance sheet surprises.

- Cut through noise by focusing on 72 resilient stocks with low risk scores so you do not miss stocks that score better on risk while others chase headlines.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.