A Look At John Wiley & Sons (WLY) Valuation As Operational Headwinds Raise Growth Concerns

John Wiley & Sons, Inc. Class A WLY | 39.05 | +0.88% |

Operational headwinds put John Wiley & Sons (WLY) under closer investor scrutiny

Recent commentary on John Wiley & Sons (WLY) points to ongoing declines in sales and free cash flow margins, with weak demand projected over the next year and higher capital needs raising fresh questions about long term growth.

Wiley's share price has climbed 6.41% over the past month but is still down 17.18% over the last 90 days, while its 1 year total shareholder return decline of 21.19% points to fading longer term momentum as investors reassess the business in light of weaker demand and rising capital needs.

If Wiley's recent pressure has you reassessing your options, it could be a useful moment to widen the lens and check out fast growing stocks with high insider ownership.

With John Wiley & Sons reporting modest annual revenue and net income growth but facing weak demand, declining returns and higher capital needs, is the recent share price slide setting up a value opportunity or is the market already discounting future growth?

Most Popular Narrative: 47.7% Undervalued

With John Wiley & Sons last closing at $31.39 versus a narrative fair value of $60.00, the valuation story rests heavily on its shift toward digital and data driven revenue.

The continued shift towards digital learning platforms, inclusive access models, and subscription-based academic content is driving margin improvement and stable, recurring revenue, evidenced by robust adoption of courseware and digital offerings across educational institutions.

Want to see what kind of revenue mix and margin profile that quote is pointing to? The narrative leans on steadier growth, higher margins, and a different earnings multiple than today. Curious how those moving parts combine to support a $60.00 value?

Result: Fair Value of $60.00 (UNDERVALUED)

However, that story can shift quickly if AI licensing proves patchy or if open access and digital rivals eat into Wiley's higher margin subscription revenues.

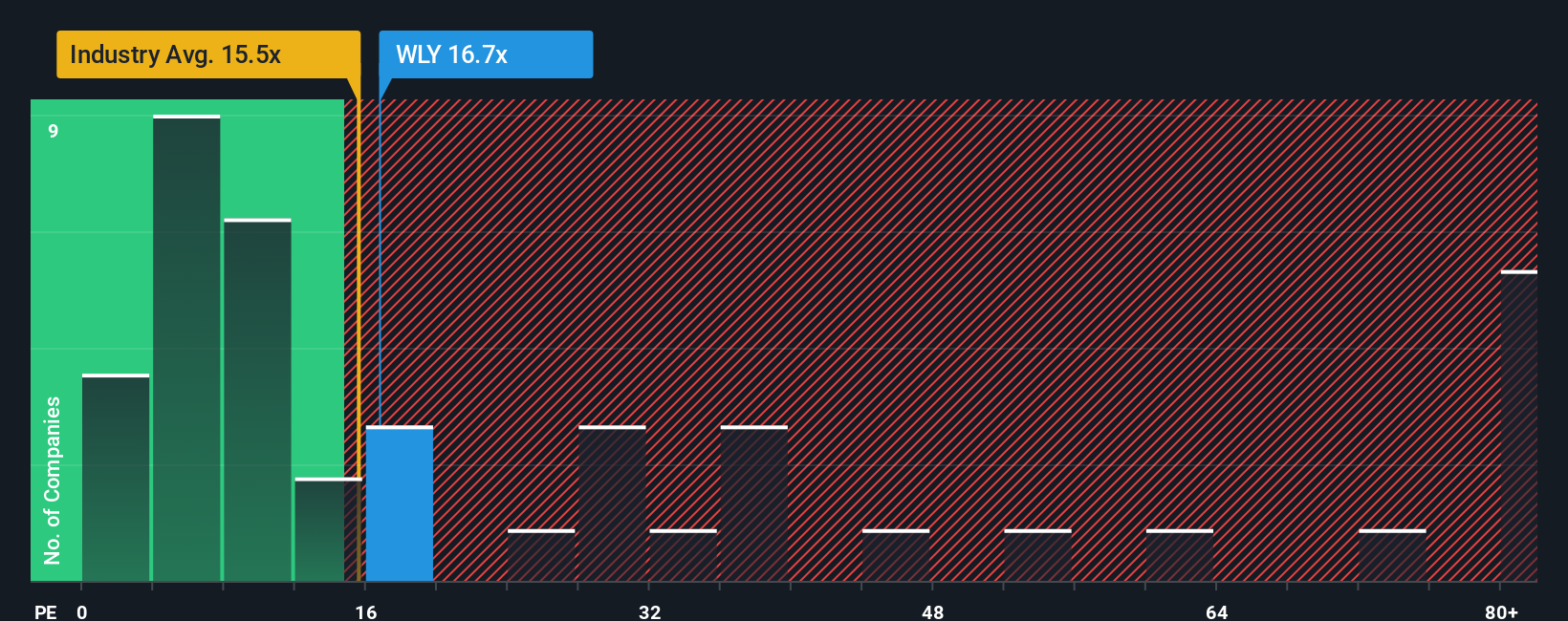

Another View: What Do The Earnings Multiple And Fair Ratio Say?

Analysts see John Wiley & Sons on a P/E of 16.2x, slightly above the US Media industry at 15.8x yet far below a fair ratio of 26.9x and a peer average of 38.3x. That combination points to a mix of caution and possible upside, raising the question of which signal may be more informative.

Build Your Own John Wiley & Sons Narrative

If you see the numbers differently or prefer to rely on your own work, you can build a custom view in just a few minutes by starting with Do it your way.

A great starting point for your John Wiley & Sons research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Wiley is only one piece of your watchlist, this is a good time to widen the net and pressure test your thinking against fresh stock ideas.

- Spot potential value plays early by scanning these 879 undervalued stocks based on cash flows that align with your preferred balance of quality and price.

- Ride major tech shifts by checking out these 24 AI penny stocks that are tied to real-world adoption of artificial intelligence tools and services.

- Add a different source of returns by reviewing these 13 dividend stocks with yields > 3% that offer income alongside potential capital movement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.