A Look At Kaiser Aluminum (KALU) Valuation After Strong First Quarter Earnings And Sharp Share Price Gains

Kaiser Aluminum Corporation KALU | 0.00 |

Earnings event and recent stock move

Kaiser Aluminum (KALU) just posted first quarter results that included US$1,106.8 million in sales and US$62.5 million in net income. These figures appear central to the stock’s recent move.

The strong first quarter report and recently affirmed US$0.77 per share dividend have coincided with a sharp shift in sentiment, with the 1 month share price return of 46.36% and 1 year total shareholder return of 186.66% indicating momentum building from both a short and longer term view.

If this kind of move has you looking for other opportunities, it could be worth checking a screener focused on 8 top copper producer stocks

With Kaiser Aluminum trading at US$163.03, above the average analyst price target of US$143.67 but at a large discount to one intrinsic value estimate, you have to ask: is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 53.1% Overvalued

The most followed narrative puts Kaiser Aluminum's fair value at $106.50, which is well below the last close of $163.03, setting up a clear valuation gap for investors to assess.

Analysts are assuming Kaiser Aluminum's revenue will grow by 9.4% annually over the next 3 years. Analysts assume that profit margins will increase from 2.7% today to 4.1% in 3 years time.

Want to see what is driving that revenue and margin lift, and how those assumptions roll into earnings and the required P/E reset? The full narrative lays out the growth profile, the profitability shift and the market multiple the story needs to work.

Result: Fair Value of $106.50 (OVERVALUED)

However, if aerospace demand or coated packaging volumes outpace current expectations, higher utilization and margins could challenge the argument that the shares are 53.1% overvalued.

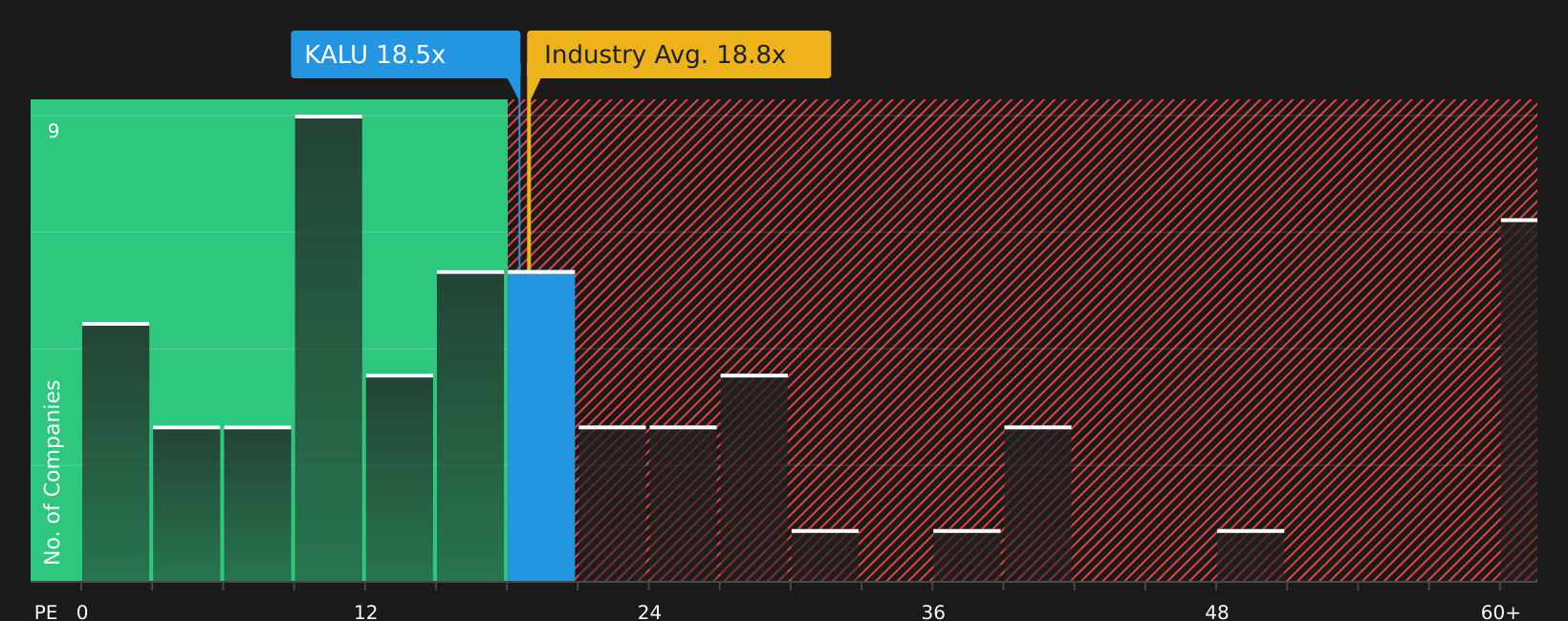

Another Way To Look At Value

While the narrative fair value of $106.50 points to Kaiser Aluminum looking 53.1% overvalued at $163.03, the P/E story is less clear cut. The current 23.3x P/E is only slightly above the US Metals and Mining average of 22.8x and not far from the 19.6x fair ratio that our model suggests the market could move toward. This raises the question of whether the valuation risk is as sharp as that headline gap implies.

Next Steps

With sentiment clearly split between risks and rewards, it makes sense to move quickly, review the data for yourself, and weigh the 3 key rewards and 3 important warning signs.

Looking for more investment ideas?

If Kaiser Aluminum has caught your attention, do not stop here; broaden your watchlist now so you are not looking back at missed opportunities later.

- Spot potential bargains early by checking a screener packed with screener containing 23 high quality undiscovered gems that meet strict quality and fundamentals criteria.

- Focus on resilient balance sheets by reviewing the solid balance sheet and fundamentals stocks screener (42 results) to see companies that prioritize financial strength.

- Prioritize stability with a screener built around 73 resilient stocks with low risk scores so you can quickly narrow in on businesses with lower risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.