A Look At Kilroy Realty (KRC) Valuation As Investors Reassess Office And Life Science REIT Prospects

Kilroy Realty Corporation KRC | 28.45 | +1.32% |

Why Kilroy Realty is on investors’ radar today

Kilroy Realty (KRC) has been drawing attention after a period of mixed share performance, with the stock showing a small 1 year total return but weaker moves over the past month and past 3 months.

For a real estate investment trust focused on office and life science properties, those return figures invite a closer look at how its current valuation lines up with recent fundamentals, including revenue of about US$1.13b and net income of roughly US$322.1m.

At a share price of US$36.56, Kilroy Realty’s recent stretch of weaker share price returns, including a 90 day share price return of 9.86% and a modest 1 year total shareholder return of 1.37%, points to fading momentum as investors reassess both income potential and risks around its office and life science portfolio.

If Kilroy’s recent moves have you rethinking where you want property exposure in your portfolio, it could be a good moment to scan other healthcare stocks for fresh ideas.

With Kilroy trading around US$36.56, carrying a value score of 5 and some pressure on recent returns and net income growth, the key question is simple: is this a mispriced REIT, or is the market already baking in future growth?

Price-to-Earnings of 13.4x: Is it justified?

At a last close of US$36.56, Kilroy Realty is on a P/E of 13.4x, which screens as inexpensive compared with both peers and the wider Office REITs industry.

The P/E multiple compares the company’s share price to its earnings per share. It gives you a sense of how much investors are paying for each dollar of current earnings. For a REIT like Kilroy, where income generation is central to the story, this is one of the core yardsticks many investors watch.

Here, the current P/E of 13.4x sits well below the peer average of 32.9x and the global Office REITs industry average of 22.3x. This suggests the market is assigning Kilroy a lower earnings multiple than many similar companies. Relative to an estimated fair P/E of 17.6x, there is also a gap that could narrow if sentiment toward its earnings profile shifts, since that fair ratio represents a level the market could move toward over time.

Result: Price-to-Earnings of 13.4x (UNDERVALUED)

However, you still need to weigh risks like a nearly 49% annual net income decline and weaker recent share returns, which could signal pressure on the current thesis.

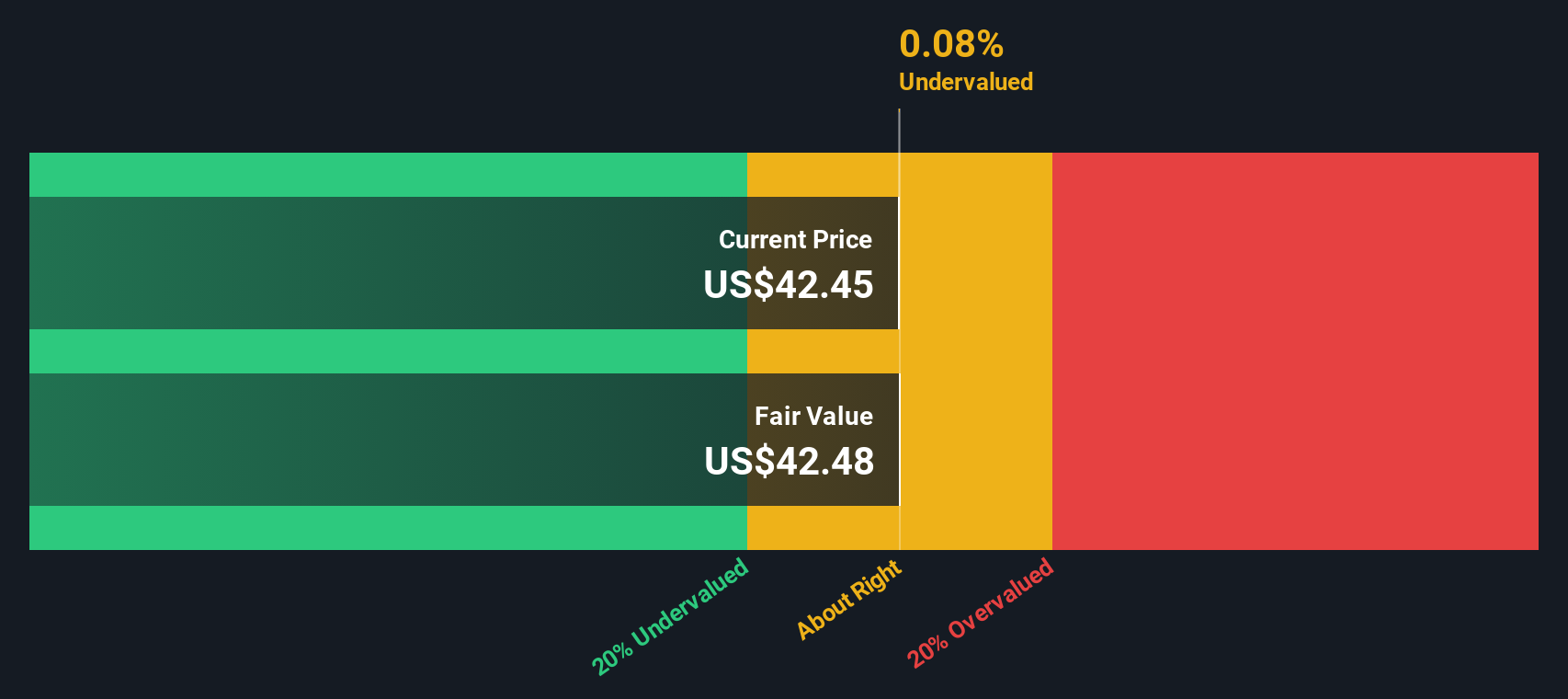

Another view: what our DCF model suggests

While the 13.4x P/E points to Kilroy trading cheaply against peers, our DCF model also suggests the shares are undervalued, with an estimate of future cash flow value around US$51.66 versus the current US$36.56. That gap could reflect opportunity or simply higher perceived risk, so which do you think it is?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Kilroy Realty for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 881 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Kilroy Realty Narrative

If you see the numbers differently or prefer to work from your own assumptions, you can build a customised view in just a few minutes with Do it your way.

A great starting point for your Kilroy Realty research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

Ready to broaden your investment watchlist?

If Kilroy has caught your attention, it is worth widening your search now so you do not miss other opportunities that could fit your goals just as well.

- Spot companies the market might be overlooking by scanning these 881 undervalued stocks based on cash flows that screen for prices that sit below their estimated cash flow value.

- Lean into growth themes by checking out these 23 AI penny stocks that focus on businesses linked to artificial intelligence trends.

- Target income ideas with these 13 dividend stocks with yields > 3% that highlight companies offering dividend yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.