A Look At Kinsale Capital Group’s Valuation After Q1 Miss And Leadership Realignment

Kinsale Capital Group, Inc. KNSL | 0.00 |

Why Kinsale Capital Group stock is back in focus

Kinsale Capital Group (KNSL) has drawn fresh attention after first quarter results came in below revenue expectations, and management reshaped its analytics and technology leadership following the retirement of its longtime CIO.

The recent leadership reshuffle in analytics and technology, combined with first quarter results that missed revenue expectations, has coincided with a sharp reset in sentiment, with a 90 day share price return of 21.25% decline and a 1 year total shareholder return of 30.41% decline. However, the 5 year total shareholder return of 86.92% shows the longer term picture has been more resilient.

If Kinsale’s recent moves have you reassessing your portfolio, it can be useful to compare it with other specialist insurers and financials or broaden out to 18 top founder-led companies

With Kinsale shares down over the past year yet still trading above one valuation model’s estimate and below analyst targets, is the recent pullback an opening for investors or a sign that markets already anticipate future growth?

Most Popular Narrative: 17.3% Undervalued

At a last close of $311.74 versus a narrative fair value of $377.11, the most followed view sees meaningful upside once slower growth and margin pressures are accounted for in the discounted cash flow model using a 6.98% discount rate.

The secular shift of risks from standard markets into the E&S channel, particularly for homeowners and catastrophe-exposed lines (for example, in California, Texas, and coastal regions), is broadening Kinsale's long-term premium base and enabling sustainable top-line growth even as competition intensifies in select lines.

Curious what sits behind that fair value gap? The narrative leans on measured revenue growth, firm margins and a future earnings multiple that assumes investors keep paying up for this profile.

Result: Fair Value of $377.11 (UNDERVALUED)

However, slower premium growth and softer margins, along with competition in large account property, could challenge the view that Kinsale is meaningfully undervalued.

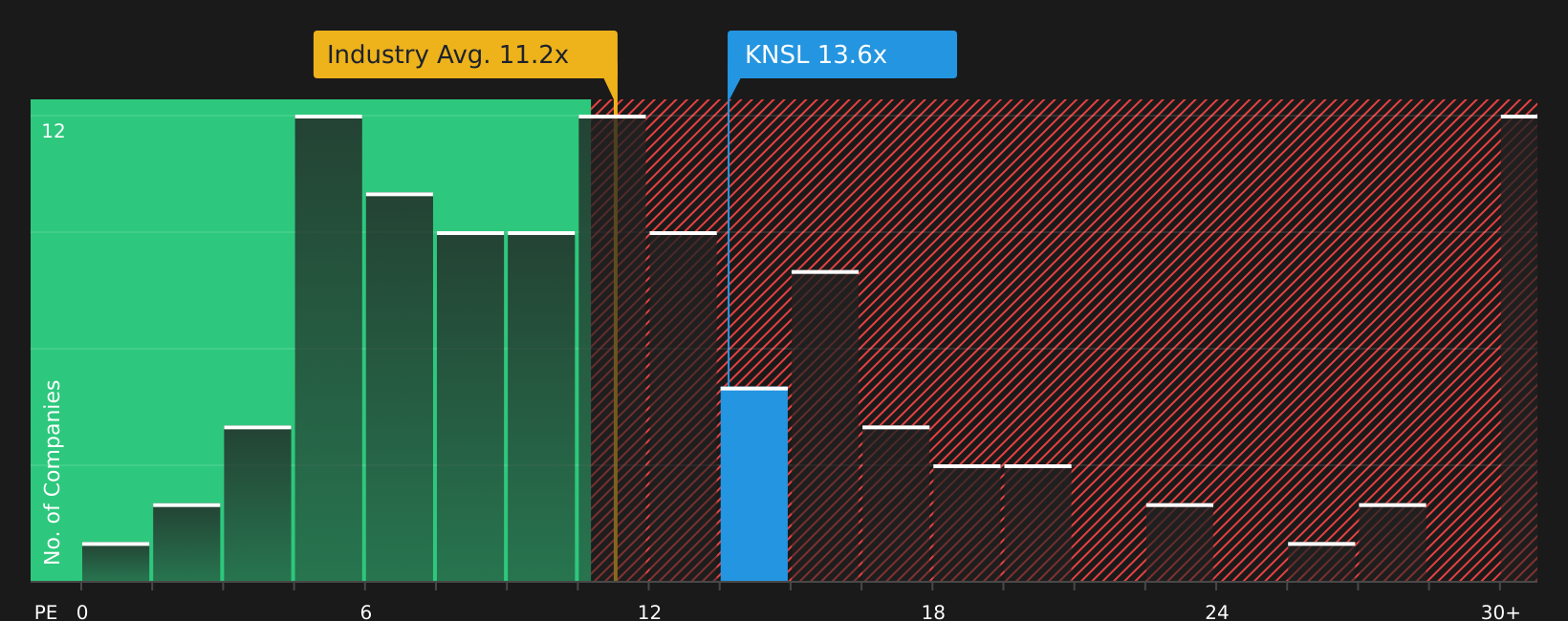

Another way to look at Kinsale’s valuation

The SWS fair ratio approach paints a very different picture to the DCF work. On this view, Kinsale trades on a P/E of 13.6x versus a fair ratio of 11.1x, above both the US Insurance average of 11.7x and peer average of 7.9x. This points to valuation risk rather than a clear bargain. Which signal do you put more weight on?

Next Steps

With mixed signals on valuation and sentiment, do you want to rely on headline views or your own judgment? Take a closer look at the 2 key rewards and 1 important warning sign

Looking for more investment ideas?

If Kinsale has sharpened your thinking, do not stop here. Use the Simply Wall Street Screener to uncover other stocks that could suit your approach.

- Target steady compounding and income potential by checking out 13 dividend fortresses that focus on meaningful yields backed by fundamentals.

- Pursue quality at a price that could make sense by scanning through 51 high quality undervalued stocks built on both cash flow strength and balance sheet support.

- Prioritise capital protection first by reviewing 67 resilient stocks with low risk scores that score well on resilience and business stability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.