A Look At Kinsale Capital Group’s Valuation As Earnings Beat And Institutional Buying Renew Investor Confidence

Kinsale Capital Group, Inc. KNSL | 0.00 |

Why Kinsale’s latest dividend and earnings beat are on investors’ radar

Kinsale Capital Group (KNSL) is back in focus after better than expected first quarter earnings, renewed institutional interest and a fresh cash dividend of $0.25 per share declared by its board.

The dividend is payable on June 11, 2026 to shareholders of record on May 28, 2026, adding an income component at a time when the stock has recently faced pressure despite earlier price gains.

At a recent share price of about $311.70, Kinsale’s move higher following the results came alongside reports of buying from firms such as Isthmus Partners LLC and Stephens Investment Management Group.

At the same time, about $10.6 million of insider selling over the past 3 months gives you another factor to weigh as you consider how earnings strength and ownership trends fit together.

Recent trading reflects this tension, with the share price down about 13% over the past 30 days and 21% year to date, while the 5 year total shareholder return of 91% contrasts with a 33% decline over the past year. This suggests longer term gains but fading momentum.

If Kinsale’s recent volatility has you thinking about diversification, it could be a good moment to broaden your watchlist and check out 20 top founder-led companies

With Kinsale trading around $311.70, showing an intrinsic discount of about 43% and a value score of 2, you have to ask yourself: is this a mispriced insurer, or is the market already baking in future growth?

Most Popular Narrative: 12.7% Undervalued

Against a last close of $311.70, the most followed narrative pegs Kinsale Capital Group’s fair value at about $356.89, framing the recent pullback as a potential pricing gap rather than a verdict on the business.

The secular shift of risks from standard markets into the E&S channel, particularly for homeowners and catastrophe-exposed lines (e.g., in California, Texas, and coastal regions), is broadening Kinsale's long-term premium base and enabling sustainable top-line growth even as competition intensifies in select lines.

Want to see what sits behind that optimism on the E&S opportunity set? The narrative leans on specific revenue, margin and multiple assumptions that could change how you view today’s price.

Result: Fair Value of $356.89 (UNDERVALUED)

However, slower expected revenue growth and pressure on margins, alongside competition and catastrophe exposure, could challenge the view that Kinsale is mispriced today.

Another View: Market Multiple Sends a Different Signal

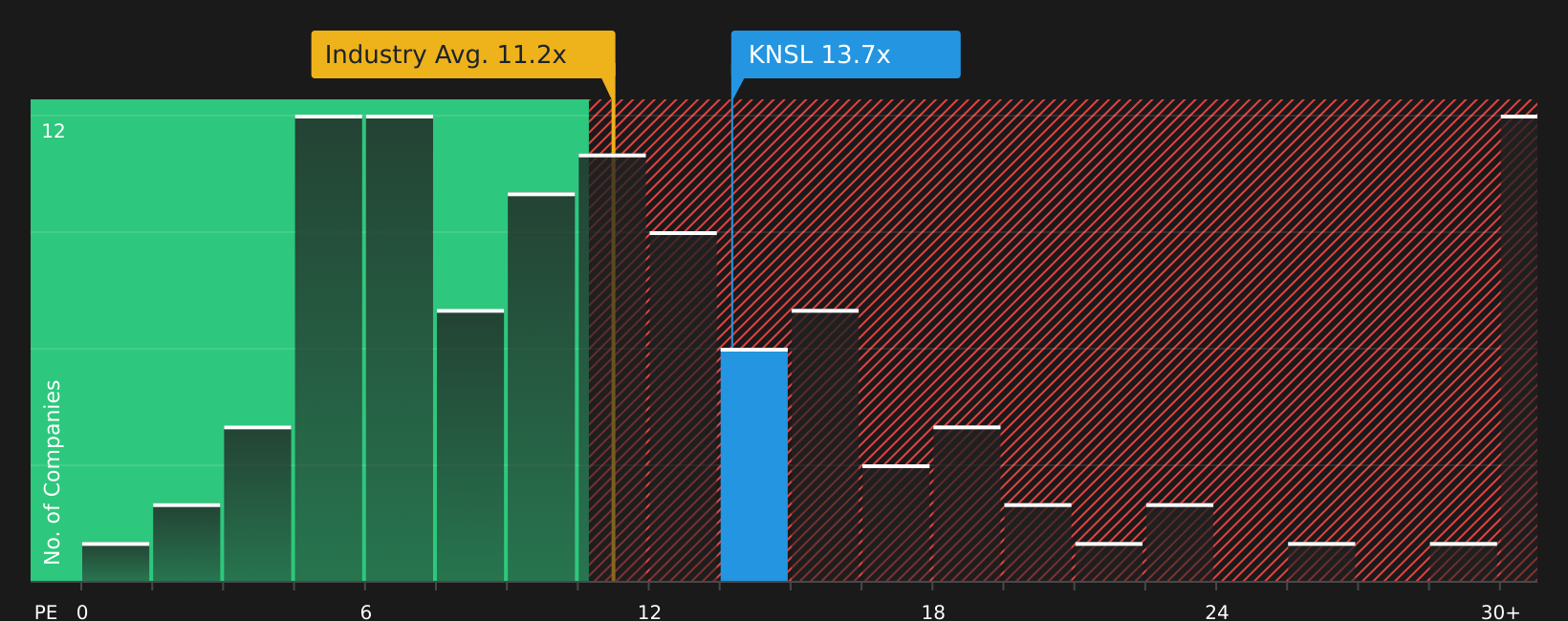

While the narrative and SWS fair value of $550.19 suggest upside, the current P/E of 13.6x tells a tougher story when set against the US Insurance industry at 11.3x, the peer average at 8x and a fair ratio of 11.1x that the market could move toward.

This gap points to valuation risk rather than a clear discount, so the key question is whether Kinsale’s quality and return profile justify staying above those benchmarks if growth expectations are now more modest.

Next Steps

With the mixed messages on value and momentum so far, it helps to move quickly, check the underlying data yourself and decide whether the risk and reward trade off still feels attractive. Then weigh up the 2 key rewards and 1 important warning sign

Looking for more investment ideas?

If you want to keep your edge, do not stop at one stock. Use the screener to quickly surface other opportunities that match your preferred style.

- Target potential upside by scanning 51 high quality undervalued stocks that combine compressed valuations with stronger fundamentals than the wider market.

- Prioritize resilience with 67 resilient stocks with low risk scores designed to spotlight companies that carry lower overall risk profiles.

- Spot less crowded opportunities through the screener containing 21 high quality undiscovered gems that highlight quality businesses many investors may be overlooking.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.