A Look At KLA (KLAC) Valuation As Earnings Growth Expectations And Analyst Revisions Draw Focus

KLA Corporation KLAC | 1516.84 | -0.20% |

KLA (KLAC) heads into its January 29 earnings release with expectations for year over year growth in earnings and revenue, as recent analyst estimate revisions and rating changes put guidance in sharp focus for investors.

At a share price of US$1,512.78, KLA has seen a 30 day share price return of 18.22% and a 90 day share price return of 25.43%. Its 1 year total shareholder return of 117.12% and 5 year total shareholder return of more than 4x highlight strong longer term momentum, even after recent short term pullbacks ahead of earnings and mixed analyst commentary.

If KLA’s move has you watching semiconductor equipment more closely, it could be a useful moment to size up other high growth tech and AI stocks that are catching market attention.

With KLA trading slightly above the average analyst price target after a sharp 30 day run, the key question now is whether the stock still holds upside potential or if the market is already pricing in future growth.

Most Popular Narrative: 16.6% Overvalued

Against KLA's last close of $1,512.78, the most followed narrative points to a fair value of about $1,296.89, implying a valuation premium that hinges heavily on long term AI and wafer fab spending assumptions.

The advanced packaging market is experiencing early-stage, secular growth fueled by adoption of 2.5D/3D architectures and HBM, driving KLA's advanced packaging revenue target for 2025 up nearly 80% year-over-year with expectations that this trend is "closer to the beginning than the end"; this directly expands KLA's addressable market and should provide multi-year upside to revenue.

Curious how that growth story translates into the fair value math? The narrative leans on multi year revenue compounding, firm margins and a premium earnings multiple tied to AI heavy fabs. The full breakdown shows exactly how those ingredients stack up to support that price.

Result: Fair Value of $1,296.89 (OVERVALUED)

However, that story could easily wobble if demand from China weakens further or if tariffs and other policy shifts squeeze margins more than analysts currently expect.

Another Angle On Valuation

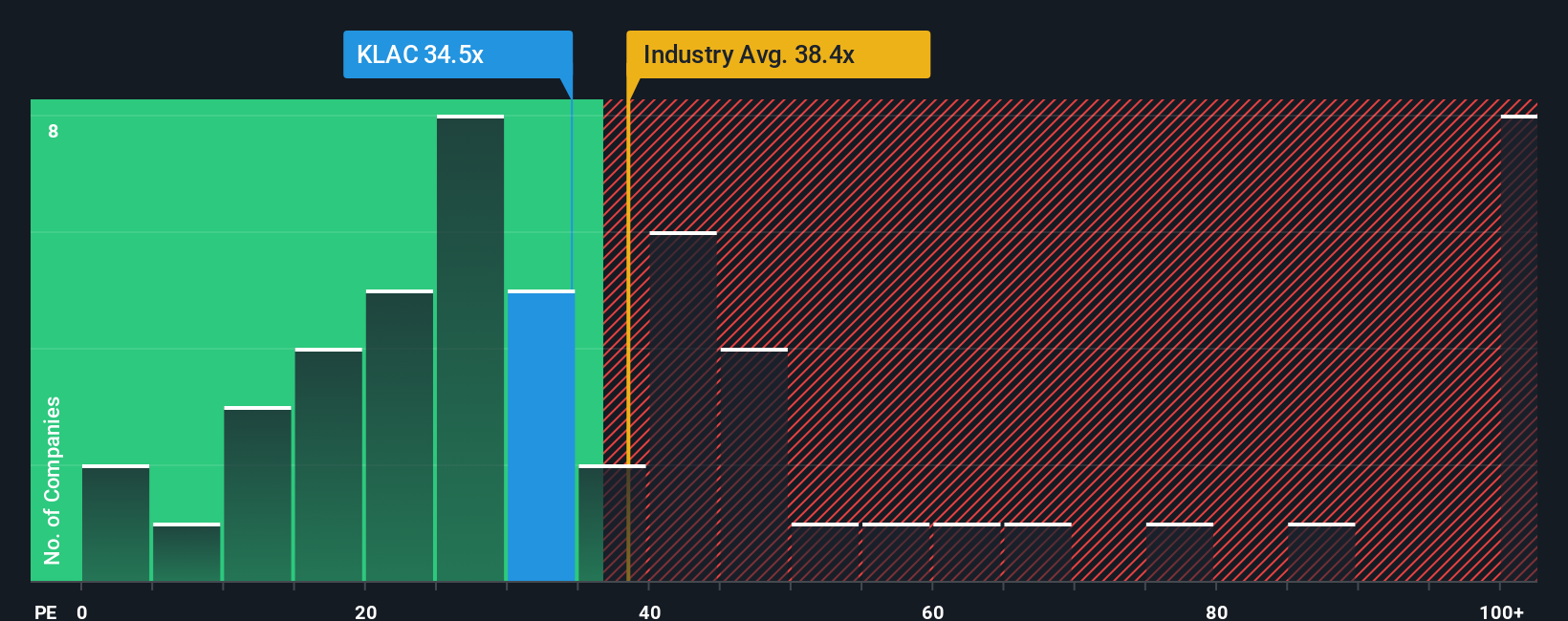

That 16.6% premium to fair value is one story. The P/E ratio tells another. At 46.9x earnings, KLA trades above the US Semiconductor average of 40.8x and above its own fair ratio of 31.3x, which points to valuation risk if sentiment or growth assumptions cool.

Build Your Own KLA Narrative

If you see the numbers differently or prefer to stress test your own assumptions, you can build a complete KLA story yourself in just a few minutes: Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding KLA.

Looking for more investment ideas?

If KLA has sharpened your interest, now is the moment to broaden your watchlist with other focused stock ideas that could round out your research.

- Spot potential bargains by scanning these 874 undervalued stocks based on cash flows that may offer more compelling prices based on their cash flow profiles.

- Ride the AI wave early by checking out these 23 AI penny stocks that are attracting attention for their exposure to artificial intelligence themes.

- Boost your income focus by running through these 13 dividend stocks with yields > 3% that currently offer yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.