A Look At Klarna Group (KLAR) Valuation As Investor Views Diverge On Future Growth

Klarna Group Plc KLAR | 0.00 |

Klarna Group stock: recent performance snapshot

Klarna Group (KLAR) has drawn investor attention after a period of mixed share performance, with a 2.7% gain over the past day, an 8.6% rise over the past month, and a 49.2% decline over the past 3 months.

Despite the latest 2.7% 1 day share price return and a 30 day share price return of 8.6%, the year to date share price return of a 50.8% decline signals fading momentum from earlier levels.

If Klarna’s swings have you thinking more broadly about opportunities in financial technology and payments, it could be a good moment to widen your radar with 19 top founder-led companies

With revenue growth running at 16.4% and net income improving from a loss position, yet the share price sitting well below the average analyst target, you have to ask: is this a mispriced fintech bank, or is the market already factoring in future growth?

Most Popular Narrative: 67.3% Undervalued

Compared with Klarna Group's last close at $14.07, the most followed narrative pegs fair value at $43.01, suggesting a wide gap investors are debating.

The heart of Klarna’s mission addresses a fundamental human constant: People want things. Whether it’s a necessary home repair (actual construction) or the latest tech to stay competitive, there is often a temporal disconnect between a consumer's desire and their payday.

Small, Purposeful Loans: Instead of the "revolving door" of high-interest credit card debt, Klarna offers surgical, small-scale loans.

Curious how that mission translates into a $43.01 fair value? The narrative focuses on ramping revenue, improving margins, and a future earnings multiple that assumes real staying power.

Result: Fair Value of $43.01 (UNDERVALUED)

However, stubborn losses of $294 million and any slowdown from 16.4% revenue growth could challenge the $43.01 narrative and keep pressure on sentiment.

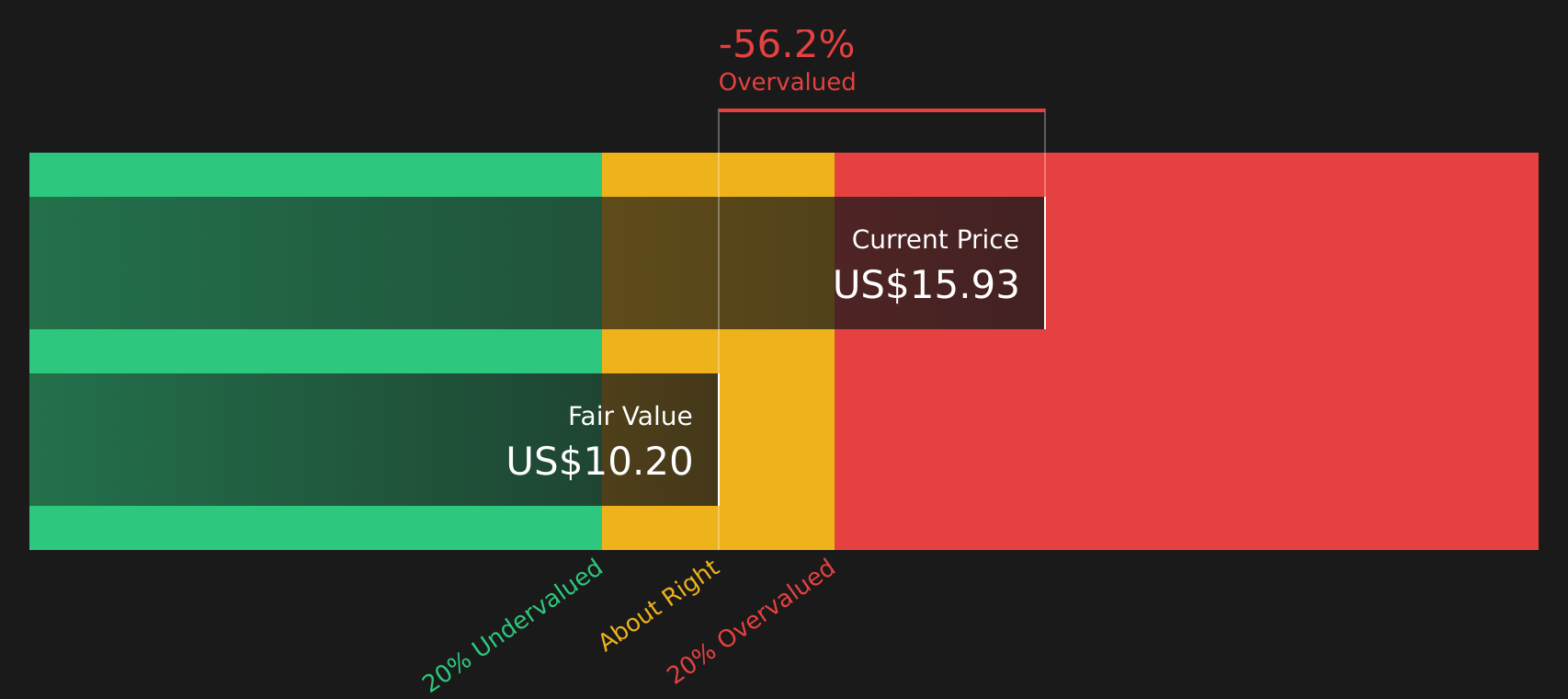

Another view on Klarna’s value

While the community’s $43.01 fair value leans on growth and future earnings, the SWS DCF model points in a different direction. On that view, Klarna’s current $14.07 share price sits above an estimated future cash flow value of $7.29, which implies overvaluation instead of a bargain.

When one approach says undervalued and another suggests the opposite, the real question for you is which assumptions around growth, margins, and risk feel more realistic.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Klarna Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 56 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With such a split view on Klarna, now is the time to look through the numbers yourself, weigh the trade off between risk and reward, and check the 2 key rewards and 1 important warning sign

Looking for more investment ideas?

If Klarna has sharpened your focus, do not stop here. Spread your attention across other opportunities that might better fit your goals and risk comfort.

- Target potential upside in quality names by scanning the 56 high quality undervalued stocks that combine solid business traits with prices below many investors' expectations.

- Strengthen your income stream by reviewing the 13 dividend fortresses that offer yields above 5% while aiming to maintain payout resilience.

- Reduce sleepless nights by checking the 72 resilient stocks with low risk scores designed for investors who want steadier businesses with lower overall risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.