A Look At Klarna Group’s Valuation As First Net Profit And Revenue Beat Draw Investor Attention

Klarna Group Plc KLAR | 0.00 |

Klarna Group (NYSE:KLAR) is back in focus after first quarter 2026 results beat expectations. The company posted its first net profit and issued new second quarter revenue guidance of US$960 million to US$1,000 million.

The stock has been volatile around the news, with a 1-day share price return of down 7.89% after earnings, a 7-day share price return of up 4.62%, and a year-to-date share price return of down 46.9%. This suggests that recent momentum is improving but still weak compared with earlier in 2026.

If Klarna’s earnings story has your attention, it can be useful to see how other fintech and AI related plays are shaping up, starting with 62 profitable AI stocks that aren't just burning cash

With Klarna now profitable and trading about 50% below the average analyst price target, investors are asking a key question: is the stock undervalued after the recent pullback, or is the market already pricing in future growth?

Most Popular Narrative: 64.7% Undervalued

Compared with Klarna Group's last close at $15.17, the most followed narrative pegs fair value at $43.01, implying a large valuation gap.

My fair value of $43.01 represents a significant vote of confidence in Klarna’s ability to maintain this trajectory. While the broader market often fluctuates based on interest rate fears, the "narrative of the $43" is one of undervalued efficiency.

Curious what kind of revenue curve, profit margin profile, and future earnings multiple are baked into that $43.01 figure? The narrative leans on a tight set of growth and profitability assumptions that could materially change how you see Klarna's long term earnings power.

Result: Fair Value of $43.01 (UNDERVALUED)

However, this hinges on Klarna turning its current US$294 million net loss into durable profitability and managing credit risk as it expands flexible lending products.

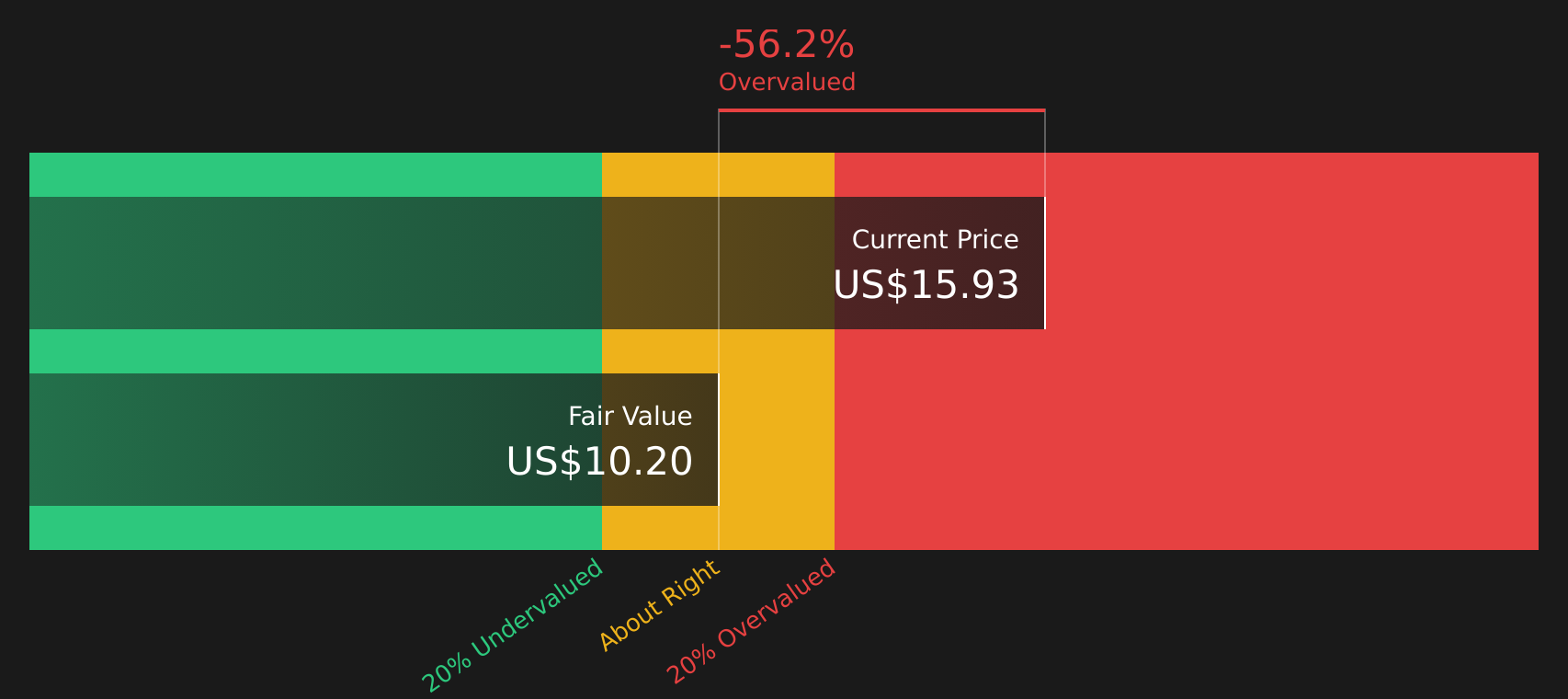

Another View: Our DCF Says Klarna Is Expensive

While the user narrative points to a fair value of $43.01, our DCF model presents a different picture. At $15.17, Klarna trades above an estimated future cash flow value of $11.51, which signals potential overvaluation if those cash flow forecasts prove accurate.

For investors, that contrast raises a useful question: do you lean more on long term growth narratives or on what the cash flow math is indicating right now?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Klarna Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 50 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With such mixed signals on value and future prospects, it makes sense to move quickly and review the key data yourself. To see a concise summary of the main concern and the upside case in one place, start with 2 key rewards and 1 important warning sign

Looking for more investment ideas?

If Klarna is on your radar, do not stop there. This can be a good time to widen your watchlist and explore other opportunities before the crowd catches on.

- Zero in on value by scanning 50 high quality undervalued stocks that combine quality fundamentals with prices that may not fully reflect their strengths.

- Strengthen your income stream by reviewing 12 dividend fortresses built around companies offering higher yields with a focus on resilience.

- Prioritize stability by checking 66 resilient stocks with low risk scores featuring companies with lower risk scores that may better suit a steadier portfolio approach.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.