A Look At Klarna Group’s Valuation As Recent Share Price Swings Split Market Opinion

Klarna Group Plc KLAR | 0.00 |

How Klarna Group (KLAR) Is Trading Today

Klarna Group (KLAR) has drawn fresh attention after a mixed run in its stock performance, with a strong gain over the past month sitting against a weaker move in the past 3 months.

The stock closed at $14.29, with a 1 day return of around 0.3% decline and a 7 day gain of about 6.2%. Over the past month it is up roughly 8.5%, while the past 3 months show a 29.8% decline and the year to date move sits near a 50% decline.

For context, Klarna Group’s share price return shows short term momentum with a 7 day gain and 1 month share price return of 8.5%. This is set against a much weaker year to date share price return near a 50% decline, suggesting sentiment has cooled after earlier enthusiasm about its digital banking and payments model.

If you are weighing Klarna against other opportunities in financial technology, it can help to broaden your view and see how other founder led growth stories are shaping up through the 19 top founder-led companies

With Klarna reporting US$3,509.0 million of revenue, a net loss of US$294.0 million and a stock price of US$14.29 versus an average analyst target of US$22.82, is there real upside here, or is the market already pricing in future growth?

Most Popular Narrative: 66.8% Undervalued

Compared to Klarna Group's last close at $14.29, the most followed narrative suggests a fair value of $43.01, implying a large valuation gap built on that author's assumptions about growth and profitability.

My fair value of $43.01 represents a significant vote of confidence in Klarna’s ability to maintain this trajectory. While the broader market often fluctuates based on interest rate fears, the "narrative of the $43" is one of undervalued efficiency.

This narrative explains the move from current losses to that higher fair value by focusing on three core ingredients: revenue expansion, margin uplift, and a future earnings multiple that assumes real traction in Klarna's digital banking and shopping assistant ambitions.

Result: Fair Value of $43.01 (UNDERVALUED)

However, this depends on Klarna reducing its US$294.0 million net loss and moving toward profitability, as well as avoiding tighter regulation of flexible payments that could restrict growth assumptions.

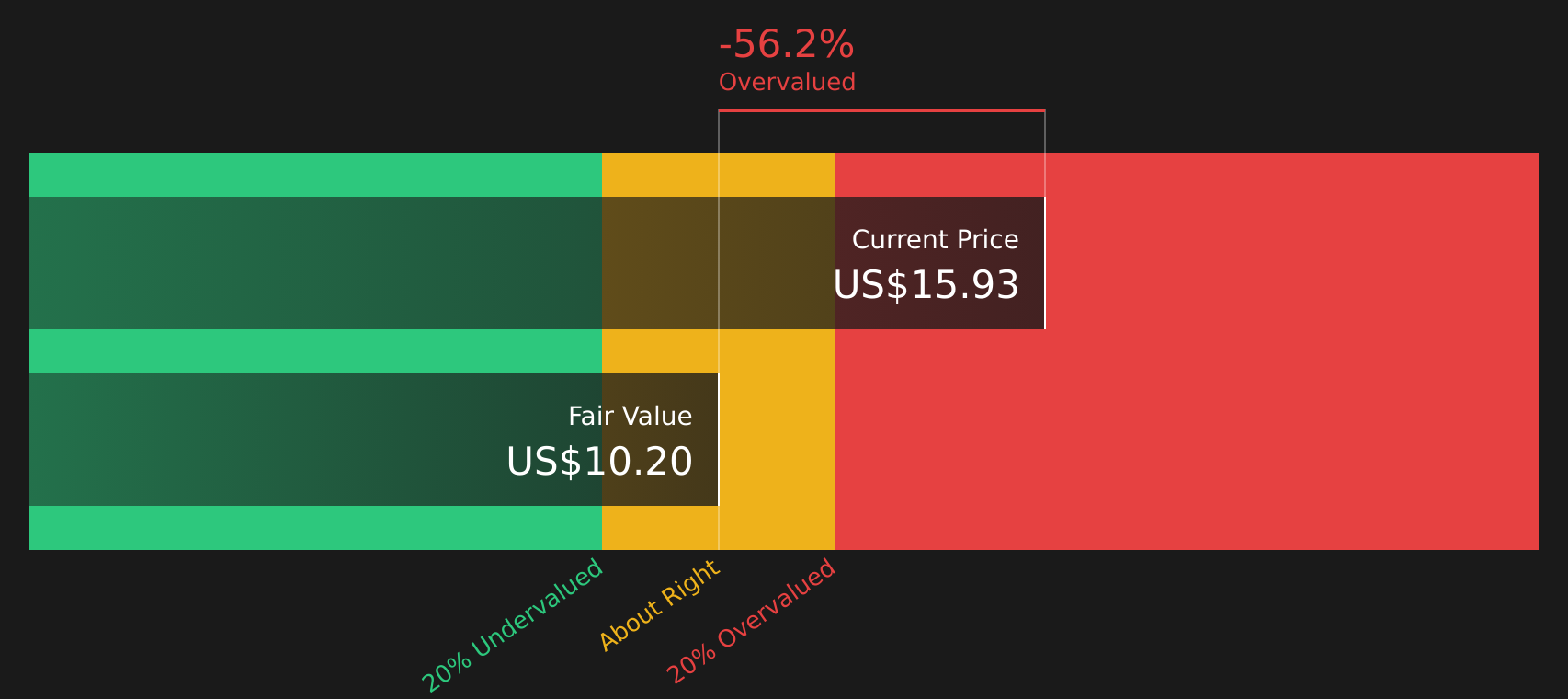

Another View: DCF Points the Other Way

While the popular narrative sees Klarna Group as heavily undervalued at a fair value of $43.01, the SWS DCF model tells a very different story. On that view, the stock at $14.29 is trading above an estimated future cash flow value of $7.34, which suggests overvaluation instead. Which story do you think fits Klarna’s risk profile better?

For a closer look at how this cash flow based estimate is built step by step, Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Klarna Group for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment clearly split between an undervalued story and a cautious DCF view, it makes sense to move fast, review the numbers yourself, and weigh both the potential upside and the issues on the table, starting with the 2 key rewards and 1 important warning sign

Looking for more investment ideas?

Do not stop with a single stock view. Use the Simply Wall St screener to spot fresh ideas that match the way you like to invest.

- Target potential upside by scanning for companies that combine quality metrics with attractive pricing through the 44 high quality undervalued stocks.

- Prioritize resilience by focusing on businesses with strong finances using the solid balance sheet and fundamentals stocks screener (45 results).

- Hunt for overlooked opportunities by searching the screener containing 23 high quality undiscovered gems before the crowd catches on.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.