A Look At Kosmos Energy (KOS) Valuation After Its Recent Share Price Surge

Kosmos Energy Ltd. KOS | 0.00 |

Why Kosmos Energy is on investors’ radar today

Kosmos Energy (KOS) has drawn attention after a period of mixed share performance, with a flat move over the past day, pressure over the past month, and a sharp gain over the past 3 months.

At a share price of $2.89, Kosmos Energy’s recent pullback over the past week and month comes after a strong 90 day share price return of 95.27%. However, the 3 year total shareholder return decline of 51.99% and the 5 year total shareholder return of 6.64% highlight how recent momentum contrasts with a mixed longer term record.

If you are looking beyond Kosmos Energy for other opportunities in the energy space, this could be a good moment to review producers screened for 31 elite gold producer stocks

With Kosmos Energy trading close to analyst targets yet screened with an intrinsic discount and a mid range value score, the key question is whether the recent surge leaves upside on the table or if markets already price in future growth.

Most Popular Narrative: 15.3% Overvalued

The most followed narrative pegs Kosmos Energy’s fair value at $2.51, compared with a last close of $2.89. This puts the current price above that anchor while still leaning on a detailed set of long term assumptions.

The analysts have a consensus price target of $3.9 for Kosmos Energy based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $7.0, and the most bearish reporting a price target of just $2.0.

Curious what justifies a fair value below the consensus target, yet still above earlier estimates? The narrative leans on moderate revenue growth, slimmer margins, and a far richer future earnings multiple than before. These are all filtered through a specific discount rate and timeframe that sharply changes the outcome.

Result: Fair Value of $2.51 (OVERVALUED)

However, this hinges on execution in politically sensitive regions and on the company’s ability to manage its substantial debt load without eroding future flexibility.

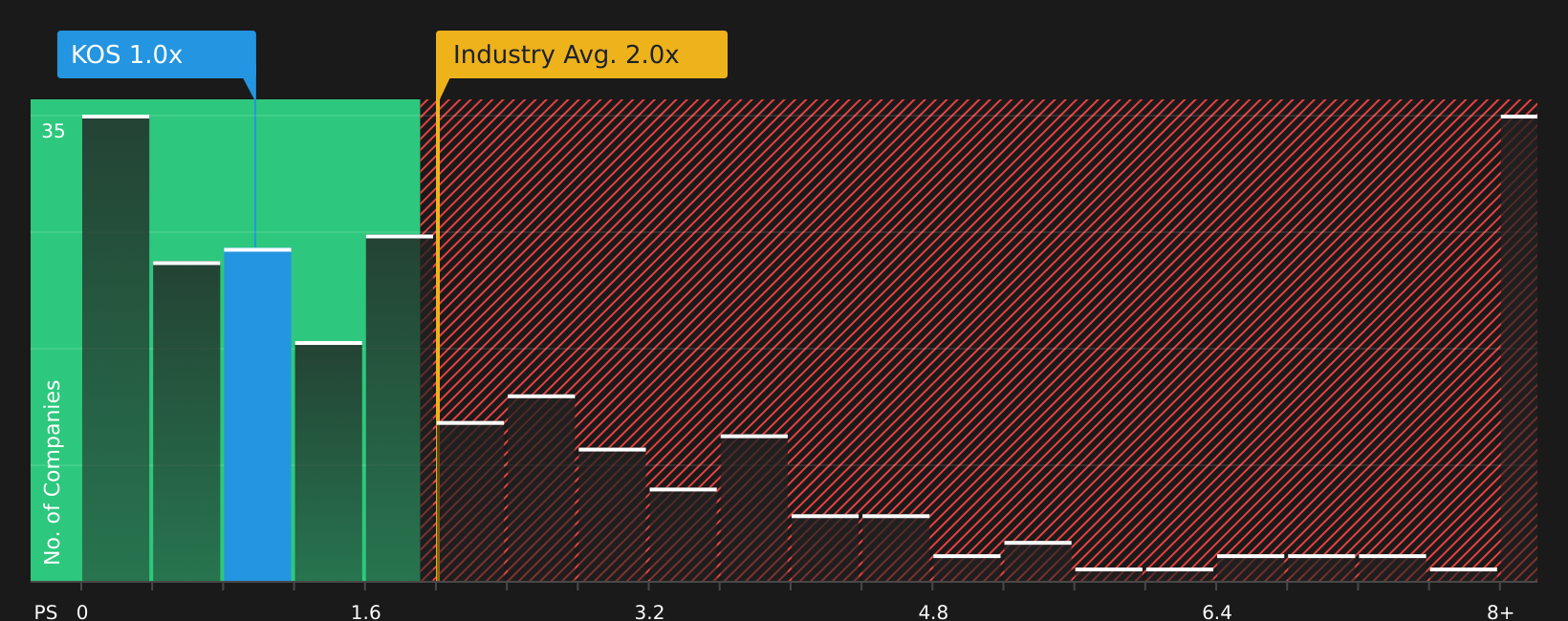

Another View: Multiples Point to Good Value

While the narrative model suggests Kosmos Energy is 15.3% overvalued against a $2.51 fair value anchor, simple P/S arithmetic paints a different picture. At 1.3x sales, the stock sits below the US Oil and Gas industry at 2.1x, the peer average at 6.7x, and even a 1.5x fair ratio the market could gravitate toward. Is this a signal of valuation risk in the narrative, or an opportunity in the current price?

For a closer look at how these sales based metrics stack up against the market, and what that gap could mean for future repricing, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment clearly split between opportunity and caution, it makes sense to check the underlying data yourself, weigh both sides, and see the 3 key rewards and 2 important warning signs

Looking for more investment ideas?

If Kosmos Energy has you thinking about where to go next, this is a strong moment to scan for other stocks that match your risk and return preferences.

- Target potential mispricing by checking out 51 high quality undervalued stocks that combine quality fundamentals with compressed valuations.

- Prioritise resilience by reviewing 72 resilient stocks with low risk scores that score well on stability and downside protection.

- Seek quality that flies under the radar by exploring the screener containing 23 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.