A Look At Kosmos Energy’s (KOS) Valuation After Director Adebayo Ogunlesi’s Major Share Purchase

Kosmos Energy Ltd. KOS | 2.92 | +8.55% |

Director Adebayo Ogunlesi’s recent open market purchase of over 3.1 million Kosmos Energy (KOS) shares, his first in years, puts insider activity in focus alongside the company’s asset reshaping and production plans.

The latest US$2.87 share price comes after a 1 month share price return of 28.7% and a very large 90 day gain. However, the 3 year total shareholder return of a 60.95% loss shows how recent momentum contrasts with a tougher longer term record.

If this kind of move in Kosmos has you thinking about what else might be setting up for big shifts in energy and infrastructure, it is worth scanning 26 power grid technology and infrastructure stocks

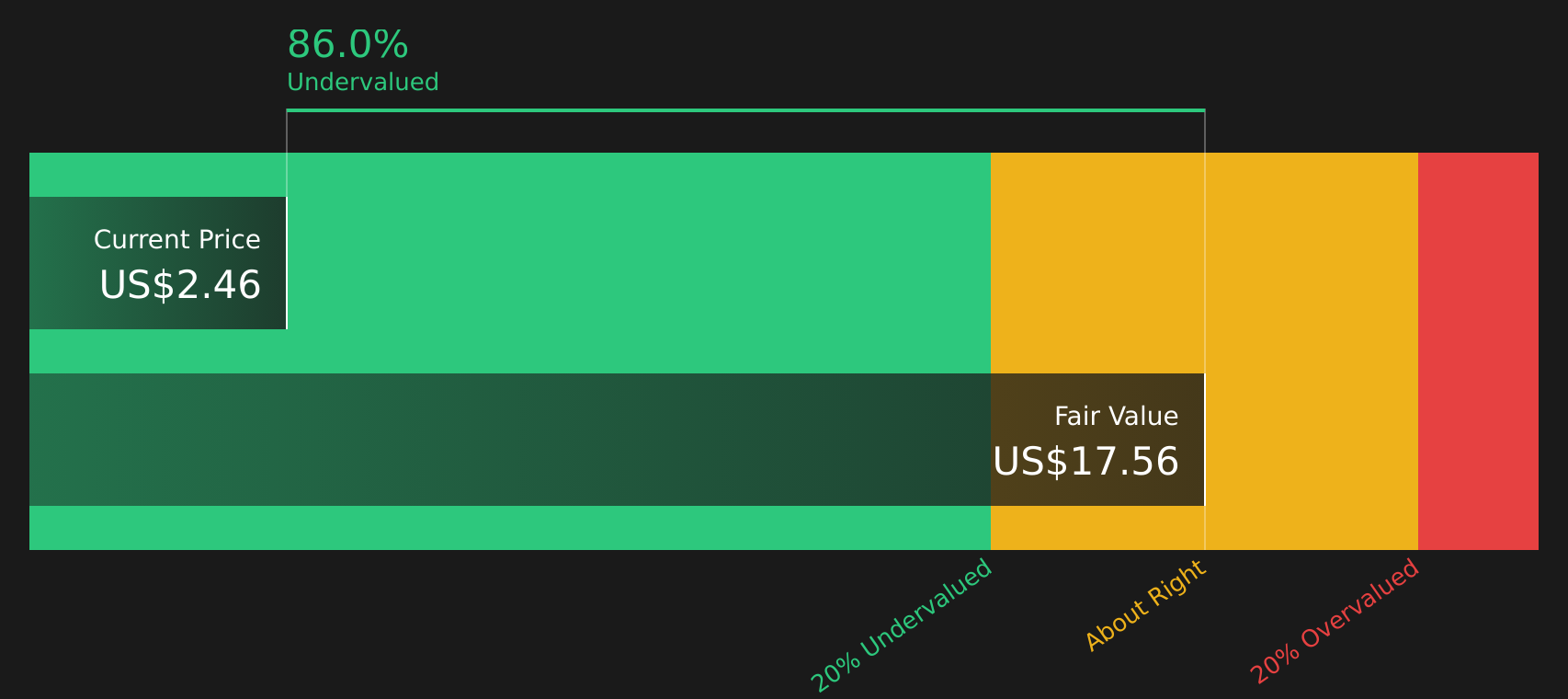

With the shares up sharply in recent months, a director buying heavily, and the price sitting near US$2.87 against an implied intrinsic discount of about 75%, you have to ask: is this a genuine opportunity, or is the market already pricing in future growth?

Most Popular Narrative: 14.5% Overvalued

With Kosmos Energy last closing at $2.87 against a widely followed fair value estimate of $2.51, the current price sits above that narrative anchor and raises questions about how much future progress is already reflected.

Fair Value: Updated estimate increased from $2.24 to $2.51 per share, representing a moderate upward move in the implied valuation anchor. Discount Rate: Adjusted from 9.70% to about 9.26%, a small reduction that generally makes future cash flows slightly more valuable in the model.

Want to understand why a modest fair value and small tweak in the discount rate still point to a rich future earnings multiple and slim margins? The core of this narrative is how revenue, profitability and valuation are expected to evolve together over several years, even as recent equity raises and impairments reshape the balance sheet.

Result: Fair Value of $2.51 (OVERVALUED)

However, there is still meaningful execution risk, with heavy reliance on politically sensitive West African assets and a sizeable debt load that could pressure cash flows if conditions tighten.

Another Way to Look at Valuation

The narrative driven fair value of $2.51 paints Kosmos as 14.5% overvalued, yet the SWS DCF model points the other way, with an estimated future cash flow value of $11.43 and the shares trading at a roughly 75% discount. Which view do you think better reflects the risks and potential cash generation?

Next Steps

With sentiment clearly mixed, this is a good moment to look at the numbers yourself and decide where you stand, starting with the 2 key rewards and 2 important warning signs

Looking for more investment ideas?

If Kosmos has sharpened your focus, do not stop here. Use the screener to quickly surface other opportunities that might suit your style and risk tolerance.

- Spot potential value opportunities early by scanning 61 high quality undervalued stocks before other investors start paying attention.

- Prioritize resilience and sleep easier at night by focusing on 69 resilient stocks with low risk scores that aim to keep downside in check.

- Aim for quality with staying power by using the solid balance sheet and fundamentals stocks screener (39 results) to highlight companies built on stronger financial footing.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.