A Look At Kratos Defense & Security Solutions (KTOS) Valuation After Drone Dominance Program Selection

Kratos Defense & Security Solutions, Inc. KTOS | 0.00 |

Kratos Defense & Security Solutions (KTOS) is back in focus after being selected for Phase 1 of the Office of the Secretary of War’s Drone Dominance Program, alongside fresh progress in its dual use autonomy deployments.

Those defense and dual use autonomy announcements have come alongside a choppy tape, with the 1 day share price return of 2.31% following a 30 day share price decline of 31.87%, yet sitting on a very large 1 year total shareholder return of about 3.3x and an even higher 3 year total shareholder return of about 7x. This points to strong long term momentum despite recent volatility.

If these moves in defense and autonomy are on your radar, it could be worth seeing what else is setting up in this space with our screener of 32 robotics and automation stocks.

With Kratos now trading at $89.06 after a sharp 30 day pullback but still sitting on multi year returns of about 7x, the key question is whether recent contract wins are already fully priced in or if there is still an opportunity the market is not yet reflecting.

Most Popular Narrative: 24.3% Undervalued

With Kratos Defense & Security Solutions closing at $89.06 against a widely followed fair value estimate of $117.63, the current pricing sits well below what that narrative implies, putting the focus squarely on how aggressive those future growth and earnings assumptions really are.

Kratos' early investments in serial production of tactical drones (e.g., Valkyrie) and rapid scaling in missile propulsion and microelectronics put it ahead of competitors as demand for unmanned and autonomous solutions escalates globally. With sole-source and first-to-market positions, Kratos is poised for significant incremental revenue and higher-margin growth as large contracts come online, particularly as international orders (with premium margins) ramp up.

Want to see what is baked into that kind of upside gap? The narrative leans on rapid revenue expansion, fatter margins, and a future earnings multiple usually reserved for high growth franchises. Curious which specific growth path and profitability mix have to land for that fair value to hold up? The full story lays out the numbers behind that $117.63 figure.

Result: Fair Value of $117.63 (UNDERVALUED)

However, that upside story still leans heavily on timely contract awards and facility ramps, as well as consistent government spending that may not follow analysts' central assumptions.

Another View: What The Market Multiple Is Saying

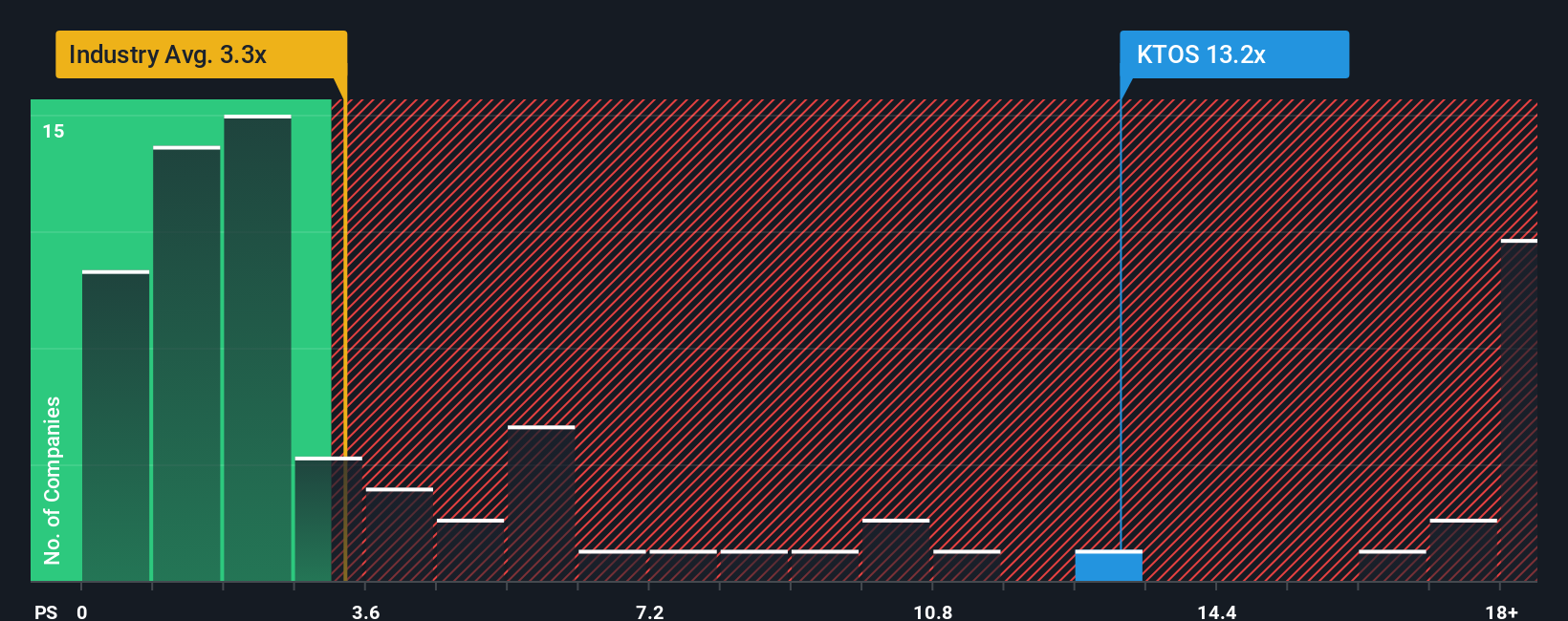

The fair value story leans heavily on growth and margin expansion, but the current P/S of 11.8x is far higher than the US Aerospace & Defense industry at 3.9x, peers at 3.7x, and a fair ratio of 3.3x. If sentiment cools, how much compression could you tolerate?

Build Your Own Kratos Defense & Security Solutions Narrative

If you see the story differently, or prefer to test your own assumptions, you can build a full Kratos view in just a few minutes starting with Do it your way.

A great starting point for your Kratos Defense & Security Solutions research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you like what you see with Kratos, do not stop here, there are other opportunities you could be missing that might fit your style even better.

- Target stability first and use our screener of 84 resilient stocks with low risk scores to see companies where risk scores are already working in your favour.

- Hunt for value and let our list of 53 high quality undervalued stocks show you where quality fundamentals and pricing are out of sync.

- Build a watchlist of future contenders by checking the screener containing 23 high quality undiscovered gems, where strong financials have not yet attracted broad attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.