A Look At Lakeland Financial (LKFN) Valuation After Robust Full Year Earnings And Buyback Completion

Lakeland Financial Corporation LKFN | 59.94 | -1.35% |

Lakeland Financial (LKFN) has drawn fresh attention after reporting full year 2025 earnings, with net interest income of US$221.02 million and net income of US$103.36 million, alongside recently completed share repurchases.

The recent full year earnings and completion of the buyback program have arrived alongside a steady shift in sentiment, with a 30 day share price return of 8.2% and a year to date share price return of 10.34%. However, the 1 year total shareholder return is 6.42% lower and the 3 year total shareholder return is 1.36% lower, suggesting recent momentum is improving after a weaker stretch for long term holders.

If these results have you thinking about where else capital could work harder, it may be a good moment to widen your search with our 22 top founder-led companies.

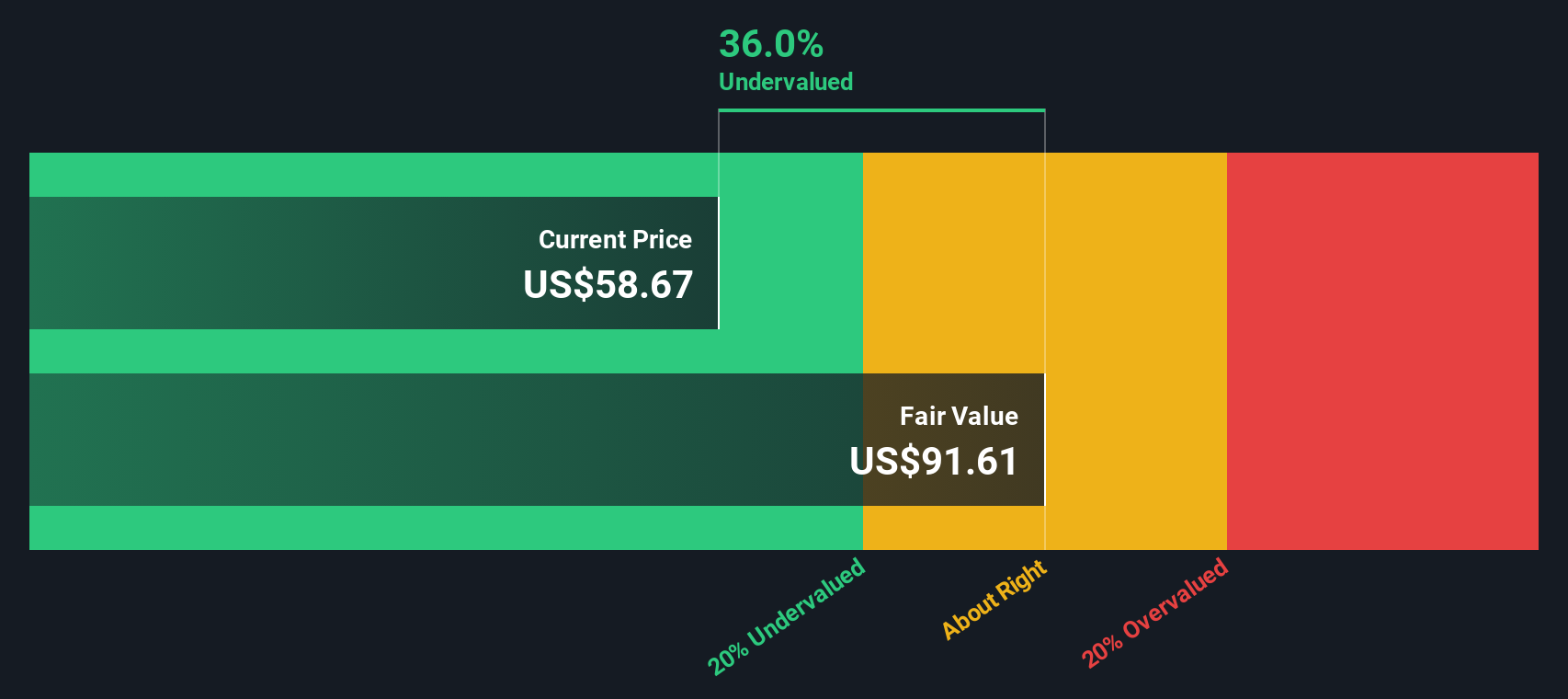

With earnings and buybacks now on the table and the share price ticking higher in recent weeks, the real question is whether Lakeland Financial is still trading below its intrinsic value or whether the market is already pricing in further growth.

Preferred P/E of 15.2x: Is it justified?

Lakeland Financial last closed at $62.30 and, on our numbers, the shares are trading above both peer and model based P/E reference points. This suggests the market is putting a relatively full price on current earnings.

The P/E ratio compares what you pay per share to the company’s earnings per share. For banks it is a quick way to see how the market is valuing their ability to generate profit from their balance sheet. In this case, the current P/E of 15.2x sits against a backdrop of high quality earnings, a net profit margin of 40.2%, and earnings growth that has recently been faster than the company’s own 5 year average.

However, that 15.2x P/E is higher than the US Banks peer average of 12x. It is also above an estimated fair P/E of 11.4x that our model suggests the market could move toward over time. Put simply, the share price currently embeds richer earnings expectations than both peers and the fair value gauge would indicate.

Result: Price-to-Earnings of 15.2x (OVERVALUED)

However, recent 1 year and 3 year total shareholder returns are in negative territory, and when combined with a premium P/E, this could leave the share price vulnerable if sentiment cools.

Another View on Value

While the current 15.2x P/E suggests Lakeland Financial trades at a premium, our DCF model points the other way. It shows an estimated future cash flow value of $98.80 per share versus the recent $62.30 price, which indicates potential undervaluation. Which signal do you put more weight on?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Lakeland Financial for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 55 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Lakeland Financial Narrative

If you see Lakeland Financial differently or want to stress test these numbers yourself, you can pull the data together and Do it your way in just a few minutes.

A great starting point for your Lakeland Financial research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Lakeland Financial has sharpened your focus, do not stop here. Use this momentum to compare other opportunities and see how they stack up against your goals.

- Pinpoint potential value opportunities by scanning our list of 55 high quality undervalued stocks, which pairs strong fundamentals with attractive pricing signals.

- Prioritise resilience by checking out 81 resilient stocks with low risk scores, built around companies that score well on our risk metrics and balance sheet checks.

- Unearth fresh names that others may be overlooking with our screener containing 25 high quality undiscovered gems, sourced from companies showing quality traits without widespread attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.