A Look At Lantheus Holdings (LNTH) Valuation As Legal Probes Follow Pylarify Revenue And Guidance Concerns

Lantheus Holdings Inc LNTH | 76.10 | +0.53% |

Investigation and legal overhang come into focus

Kahn Swick & Foti, LLC has launched an investigation into Lantheus Holdings (LNTH) after disclosures of reduced Pylarify revenue and lowered full year guidance. This development adds to an existing securities class action tied to these issues.

At a share price of $69.38, Lantheus Holdings has a 90 day share price return of 29.68% and a 1 year total shareholder return decline of 13.21%. Recent momentum therefore contrasts with weaker longer term results as investors reassess revenue risks, guidance cuts and ongoing legal scrutiny.

If the legal headlines around Lantheus have you thinking about where else to put fresh capital, now could be a good time to scan 25 healthcare AI stocks as potential new ideas to research.

With legal questions in the air, a 29.68% 90 day gain, an intrinsic discount of 53%, and a 22% gap to the average price target, you have to ask: is there real upside left here, or is the market already pricing in future growth?

Most Popular Narrative: 15.7% Undervalued

At $69.38 versus a narrative fair value of about $82.29, the widely followed view suggests Lantheus Holdings trades at a discount that hinges heavily on future execution.

Multiple new product launches within the next 18 months including the new F-18 PSMA PET, MK-6240, OCTEVY, and PNT2003 are set to diversify the revenue base, mitigate concentration risk, and open additional growth channels in oncology and neuroendocrine tumor imaging, supporting both top-line and future earnings expansion.

Curious what earnings profile needs to sit behind that valuation gap? This narrative leans on specific revenue, margin, and P/E assumptions that could surprise you.

Result: Fair Value of $82.29 (UNDERVALUED)

However, this hinges on Pylarify holding up under pricing pressure, and on acquisitions delivering more than low single digit EPS accretion instead of dragging on margins.

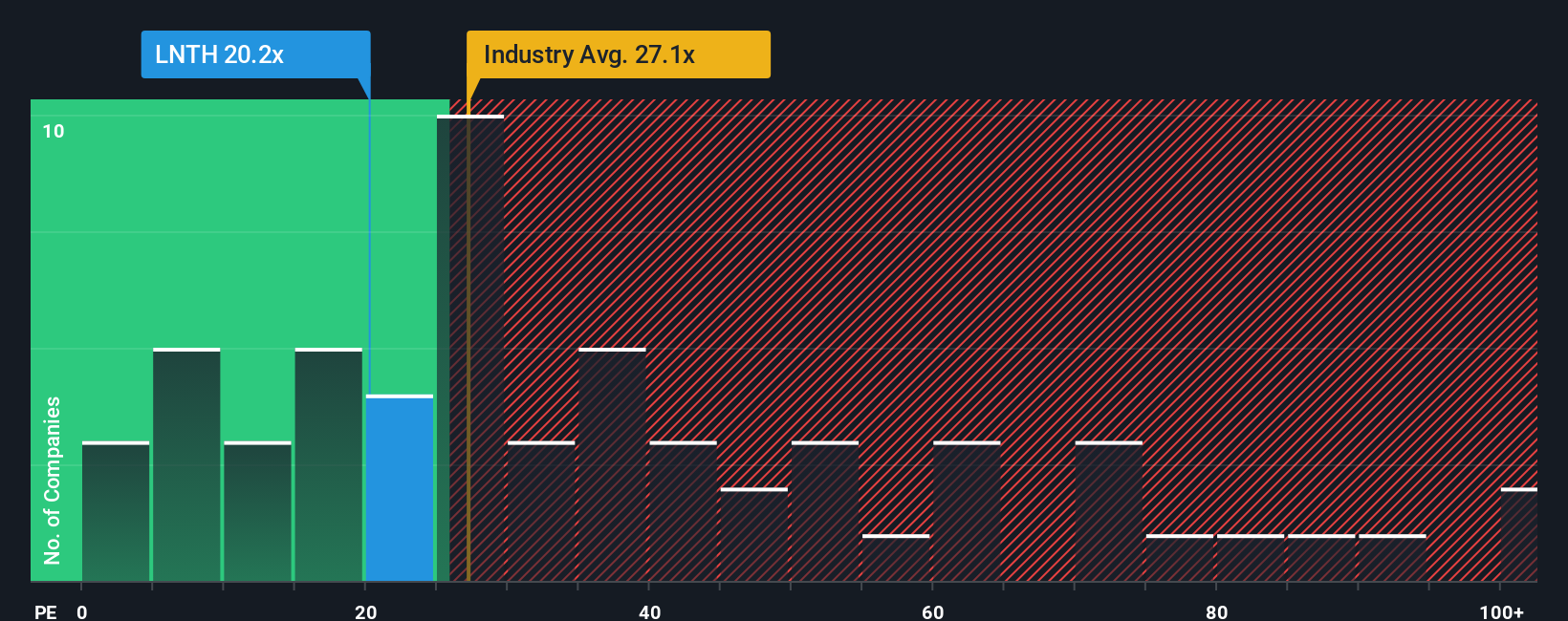

Another view on valuation: multiples send a mixed signal

Our DCF work points to a large intrinsic discount, yet the P/E story is less clear cut. At $69.38, Lantheus trades on 27.4x earnings, which is cheaper than the US Medical Equipment industry at 30.4x and its peer average of 29.3x, but above its own fair ratio of 24.6x. That gap suggests some valuation cushion versus peers, while still leaving room for the multiple to compress if growth or margins disappoint. Which signal do you treat as more important?

Build Your Own Lantheus Holdings Narrative

If this framework does not sit right with you, or you simply prefer to test your own assumptions against the numbers, you can build a personalised thesis for Lantheus in just a few minutes, Do it your way.

A great starting point for your Lantheus Holdings research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you are serious about compounding your capital, do not stop at one stock. Use the Simply Wall St screener to surface fresh, data driven ideas.

- Target dependable income and resilience by checking out a shortlist of 13 dividend fortresses that could appeal if you want cash returns plus staying power.

- Hunt for mispriced opportunities by scanning screener containing 24 high quality undiscovered gems where strong fundamentals may not yet be fully reflected in market attention.

- Prioritise sleep at night holdings by reviewing 83 resilient stocks with low risk scores that screen well on balance sheet strength and risk metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.