A Look At Lennar (LEN) Valuation As Analysts Turn More Bearish On Earnings Outlook

Lennar Corporation Class A LEN | 0.00 |

Analyst expectations and recent leadership changes at Lennar

Recent analyst forecasts for Lennar (LEN) point to lower earnings and revenue in the upcoming quarter, with sentiment turning bearish as the company reshapes its leadership and continues rolling out new communities.

Lennar's share price has seen a 4.7% 1 month gain after earlier weakness, yet the year to date share price return is down 11.2% and the 1 year total shareholder return is down 17.0%. This suggests that recent leadership changes and new community launches are being weighed against continued concerns around earnings pressure.

If this mix of weak sentiment and selective strength has you looking beyond housing, it could be a good moment to scan for 20 top founder-led companies

With Lennar trading at US$92.56 against an analyst target of US$90.43, but with an estimated 46.7% discount to intrinsic value, you have to ask whether there is genuine value here or whether the market is already pricing in future growth.

Most Popular Narrative: 1.2% Overvalued

Against a last close of $92.56 and a narrative fair value of $91.50, Lennar is framed as only modestly rich on valuation, with the story hinging more on earnings quality, margins, and capital allocation than on a big mispricing call.

The analysts have a consensus price target of $91.5 for Lennar based on their expectations of its future earnings growth, profit margins and other risk factors.

However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $124.0, and the most bearish reporting a price target of just $74.0.

Analysts are incorporating expectations for revenue, margins, and a future earnings multiple, all under a single discount rate. Curious which assumptions really carry this fair value and how much of Lennar's cash flow story is attributed to buybacks versus underlying profit metrics? The full narrative lays out those moving pieces in detail.

Result: Fair Value of $91.50 (OVERVALUED)

However, this fair value story can quickly look different if mortgage rates stay elevated or if Lennar's land light model pushes margins lower than analysts currently assume.

Another Take: Cash Flows Point to a Very Different Story

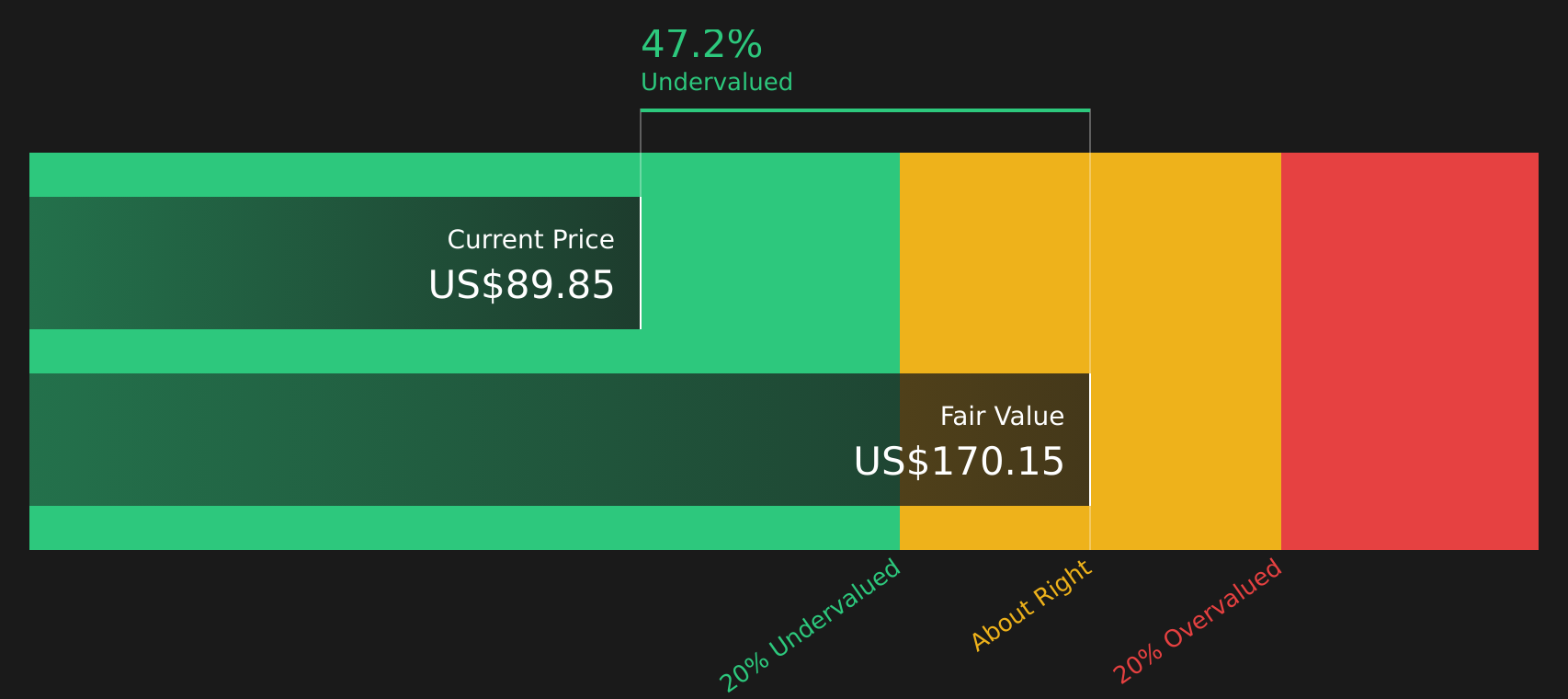

While the narrative fair value of $91.50 paints Lennar as only slightly overvalued against the $92.56 share price, the Simply Wall St DCF model suggests something far more generous, with an estimated future cash flow value of $170.42, or about a 45.7% gap. That kind of spread raises the question of which set of assumptions you trust more: the earnings based narrative or the cash flow model.

For a closer look at how those cash flows are modeled and discounted in practice, it helps to go straight to the source, Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Lennar for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 46 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment this mixed, you do not need to wait for the next headline to tell you what to think. Move quickly, review the key data for yourself, and weigh the 2 key rewards and 2 important warning signs.

Looking for more investment ideas?

If you are weighing Lennar and feel unsure about the next move, you may want to broaden your view with a few focused stock ideas that match different investing styles.

- Target potential mispricing by scanning for 46 high quality undervalued stocks that combine quality fundamentals with room for a better market view.

- Build a portfolio with income in mind by reviewing 9 dividend fortresses that aim to pair higher yields with resilience.

- Put capital to work in financially robust businesses by checking the solid balance sheet and fundamentals stocks screener (46 results) that keep risk in tighter check.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.