A Look At Life Time Group Holdings (LTH) Valuation After Upbeat Preliminary Results And 2026 Guidance

Life Time Group Holdings, Inc. LTH | 26.99 | +3.37% |

Life Time Group Holdings (LTH) shares moved after the company issued preliminary fourth quarter and fiscal 2025 results, along with new 2026 guidance that provides investors with updated revenue, earnings, and expansion targets to evaluate.

At a share price of $29.70, Life Time Group Holdings has seen a 1-day share price return of 2.98% and a 7-day share price return of 9.43%, with the recent guidance and partnerships, such as the Life Time x EVEREVE capsule collection and its high profile Miami marathon events, helping to keep attention on the stock. Over a longer horizon, the 3-year total shareholder return of 59.42% compared with a 1-year total shareholder return of 2.88% suggests earlier gains have moderated and recent momentum is now rebuilding.

If this kind of story has you looking beyond a single wellness brand, it could be a good moment to scan fast growing stocks with high insider ownership as a way to spot other companies attracting committed insider backing.

With Life Time now trading at $29.70 after upbeat guidance and analyst optimism, the key question is whether today’s price still leaves room for upside or if the market is already pricing in future growth.

Most Popular Narrative: 26.4% Undervalued

With Life Time Group Holdings last closing at $29.70 against a narrative fair value of $40.36, the current setup centers on whether the earnings path and margin profile can justify that gap over time.

The expanding pipeline of new and larger club openings in affluent and high-density markets positions Life Time for sustained membership and top-line revenue growth, benefiting from the growing consumer demand for premium health, wellness, and lifestyle experiences.

Accelerating growth in ancillary, higher-margin services including personal training, Life Time Digital offerings, nutritional supplements, and health and wellness programs supports increased average revenue per member and improved net margins as consumer expectations shift toward holistic wellness.

Want to see what has to happen on revenue, margins, and future earnings to reach that valuation? The narrative focuses on steady club rollout, richer ancillary spend, and a premium earnings multiple. Curious how those pieces fit together over the next few years? The full story lays out the numbers behind that fair value step by step.

Result: Fair Value of $40.36 (UNDERVALUED)

However, this story can change quickly if heavy capital needs for new clubs strain free cash flow or if premium pricing meets weaker demand for in-person visits.

Another Angle On Value

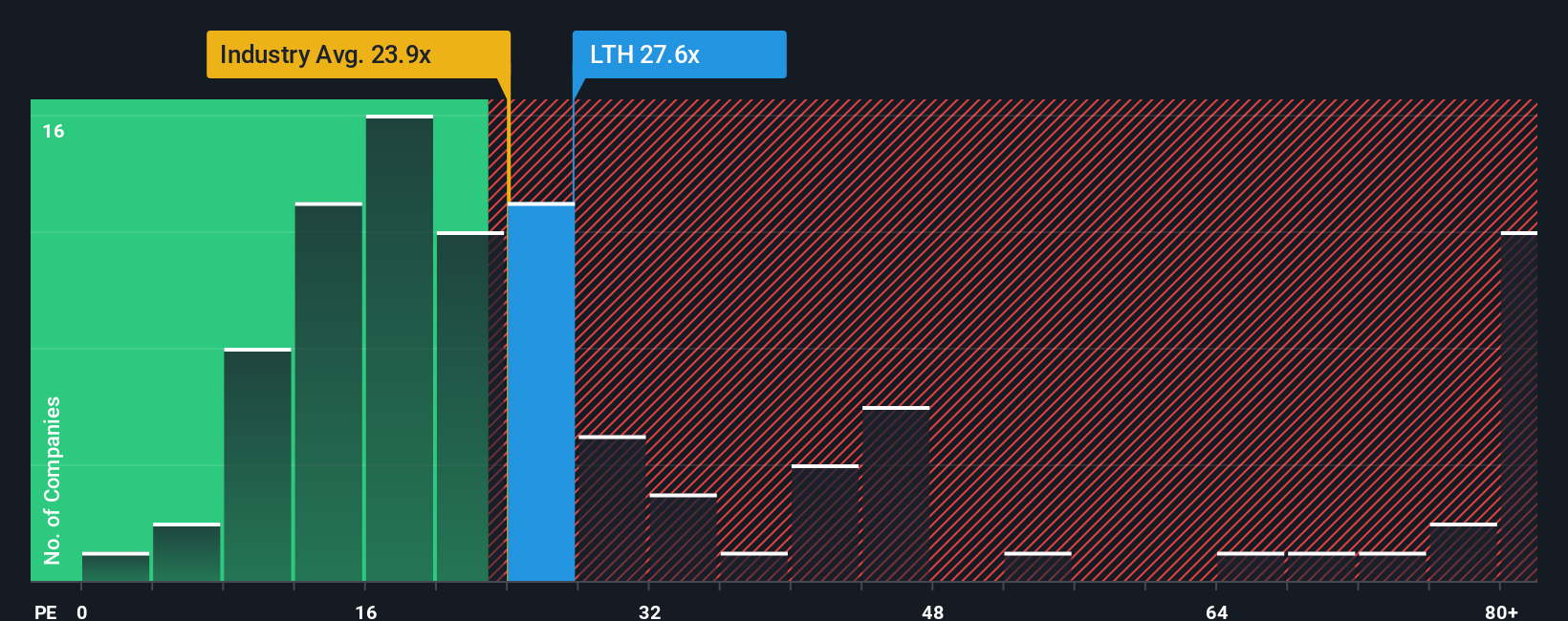

That 26.4% undervaluation story sits awkwardly next to Life Time Group Holdings trading on a P/E of 22.8x. This is higher than the US Hospitality average of 21.5x and above its fair ratio of 20.8x. If the market drifts back toward that fair ratio, how much of the upside case really survives?

Build Your Own Life Time Group Holdings Narrative

If you see the numbers differently or want to stress test your own assumptions, it only takes a few minutes to build a custom view using Do it your way.

A great starting point for your Life Time Group Holdings research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If Life Time has you thinking bigger, do not stop here. The screener is built to surface fresh ideas you might wish you had found earlier.

- Catch potential early movers by scanning these 3521 penny stocks with strong financials that combine smaller market sizes with stronger balance sheets and real operating businesses.

- Target future focused themes by checking out these 23 AI penny stocks that link artificial intelligence exposure with liquidity and core financial filters.

- Zero in on pricing gaps by reviewing these 867 undervalued stocks based on cash flows that flag companies trading below what their cash flows may justify.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.