A Look At Ligand Pharmaceuticals (LGND) Valuation As Royalty Growth And Investment Plans Take Focus

Ligand Pharmaceuticals Incorporated LGND | 199.59 | -0.02% |

Royalty growth outlook and capital deployment signal focus areas for investors

Ligand Pharmaceuticals (LGND) recently highlighted an expected 40% royalty revenue increase in 2026 and a 23% compound annual growth rate projection through 2030, alongside more than US$1b in deployable capital for new investments.

Those royalty growth projections and the large capital pool are arriving after a sharp move in the stock, with a 1 year total shareholder return of 73.91% and a 3 year total shareholder return of 166.07%. However, the 1 day share price return of an 8.72% decline and softer recent trading suggest momentum has cooled after a strong run.

If Ligand’s royalty model has caught your attention, this can be a good moment to scan other healthcare stocks that might fit a similar long term thesis.

With Ligand trading at US$188.78 and screening as intrinsically discounted by 37%, yet already up 166.07% over three years, should you view this as a potential mispricing, or assume the market is already factoring in those royalty growth targets?

Most Popular Narrative: 22.5% Undervalued

Against a last close of US$188.78, the most followed narrative points to a fair value of US$243.44, anchored in detailed revenue and margin assumptions.

Strong revenue and earnings growth are expected as Ligand broadens its high-margin royalty portfolio, with multiple partnered drugs (such as O2vir, Filspari, Qarziba, and Zelsuvmi) in various stages of commercialization or late-stage development. This expanding royalty base enhances recurring revenue, earnings visibility, and long-term cash flow predictability.

Curious what kind of revenue ramp and margin reset sit behind that fair value jump? The narrative leans heavily on richer royalties, rising profitability, and a future earnings multiple that is far from conservative.

Result: Fair Value of $243.44 (UNDERVALUED)

However, this hinges on key assumptions, and pressure on royalty pricing or a setback in one of the larger partnered drugs could quickly challenge that “undervalued” story.

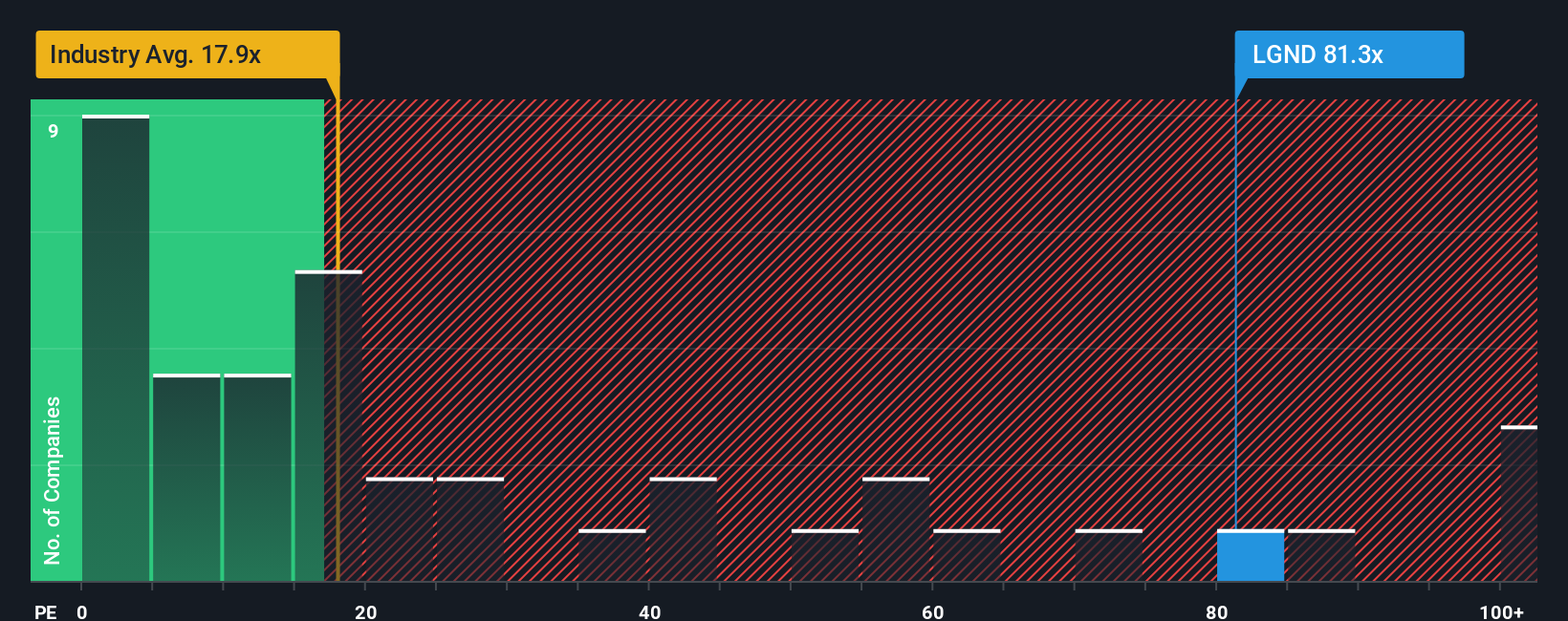

Another Angle: Earnings Multiple Sends A Very Different Signal

Our DCF model sees Ligand as trading about 37.3% below its estimated fair value of US$301.09, which points to an undervalued setup. Yet the current P/E of 76.5x is far above the US Pharmaceuticals industry at 20.1x and peer average at 23.5x, and also well ahead of the 21.2x fair ratio the market could move toward. Is this a genuine opportunity, or is the price already stretching future expectations?

Build Your Own Ligand Pharmaceuticals Narrative

If you are not on board with this view, or prefer to test your own assumptions against the numbers, you can build a full narrative yourself in just a few minutes with Do it your way.

A great starting point for your Ligand Pharmaceuticals research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Ligand has sharpened your thinking, do not stop here. Widening your watchlist with fresh angles can surface opportunities you would not otherwise consider.

- Target potential turnaround stories by scanning these 884 undervalued stocks based on cash flows that currently trade below what their cash flows may justify.

- Ride powerful tech trends by focusing on these 25 AI penny stocks that link artificial intelligence to real business models and financials.

- Position for income-focused returns by filtering for these 13 dividend stocks with yields > 3% that may complement growth oriented holdings.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.