A Look At Lowe’s Companies (LOW) Valuation As It Launches MyLowe’s Rewards Kids Club

Lowe's Companies, Inc. LOW | 231.03 | -2.10% |

Lowe's Companies (LOW) is drawing fresh investor interest after launching the MyLowe's Rewards Kids Club, a new family focused program that builds on its long running in store Kids Workshops.

The MyLowe's Rewards Kids Club launch comes as momentum in the shares has been picking up, with a 30 day share price return of 12.65% and a 90 day return of 19.39%, while the 1 year total shareholder return of 12.72% and 5 year total shareholder return of 72.45% point to solid compounding over time.

If this family focused news has you thinking about where else growth stories might emerge, it could be a good moment to scan our screener of 22 top founder-led companies for broader ideas.

With Lowe’s trading near its analyst price target and only a small implied intrinsic discount, the key question for investors is whether recent gains leave limited upside or the market is still underestimating its future growth potential.

Most Popular Narrative: 0% Overvalued

The most followed narrative puts Lowe's fair value at $278.13, almost exactly in line with the last close at $278.38. This frames the Kids Club launch against a tightly priced stock.

Ongoing pent-up demand from delayed home improvement projects, combined with record-high aging U.S. housing stock and an estimated 18 million new homes needed by 2033, points to a significant runway for future growth in renovation, repair, and new construction. This will positively affect revenue and support sustained top-line expansion as the housing cycle recovers.

Curious how that housing backlog, modest revenue growth assumptions and a richer future earnings multiple all fit together? The full narrative joins those pieces into one valuation blueprint.

Result: Fair Value of $278.13 (ABOUT RIGHT)

However, that blueprint depends on smooth integration of the FBM and ADG deals and manageable debt levels, with any stumble in execution or financing pressure becoming a potential spoiler.

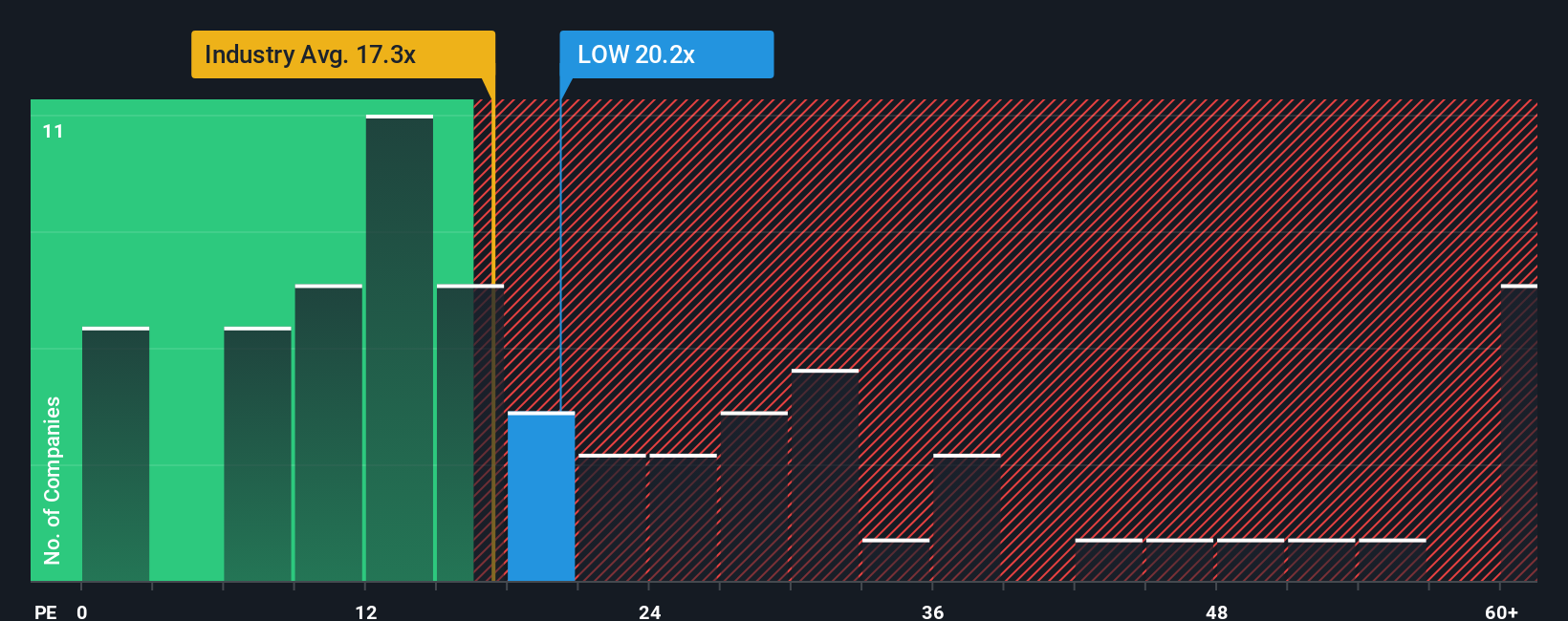

Another Take: Earnings Multiple Sends Mixed Signals

While the consensus narrative pegs Lowe's fair value close to the current $278.38 share price, the earnings multiple picture is less tidy. The current P/E of 22.8x sits above the US Specialty Retail industry average of 20.8x and slightly above the SWS fair ratio of 22.1x.

That gap is not huge, but it suggests the market is paying a bit more for Lowe's earnings than both peers and the level our fair ratio points to, which could matter if growth or margins fall short of expectations.

Build Your Own Lowe's Companies Narrative

If you look at these numbers and reach a different conclusion, or simply prefer to test your own assumptions, you can build a custom Lowe's view in just a few minutes, starting with Do it your way.

A great starting point for your Lowe's Companies research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Lowe's has your attention, do not stop here. A wider set of ideas can help you spot opportunities you might otherwise miss.

- Spot potential value opportunities early by scanning our list of 52 high quality undervalued stocks that combine quality fundamentals with what our models flag as appealing prices.

- Prioritize resilience by checking companies in our 85 resilient stocks with low risk scores where business stability and risk metrics are front and center.

- Hunt for fresher ideas by reviewing the screener containing 25 high quality undiscovered gems that screens for quality names the market may not be fully focused on yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.