A Look At LSB Industries (LXU) Valuation As Models Clash On Fair Value Estimates

LSB Industries, Inc. LXU | 0.00 |

LSB Industries (LXU) is drawing attention after recent share price swings, with a 0.7% gain over the past week contrasting with a decline over the past month and a strong performance over the past three months.

At a share price of $14.56, LSB Industries has seen the 90 day share price return of 52.94% and the year to date share price return of 69.89%, while the 1 year total shareholder return of 147.20% points to strong longer term momentum.

If you are looking for other ideas in this part of the market, it could be a good time to scan 8 top copper producer stocks.

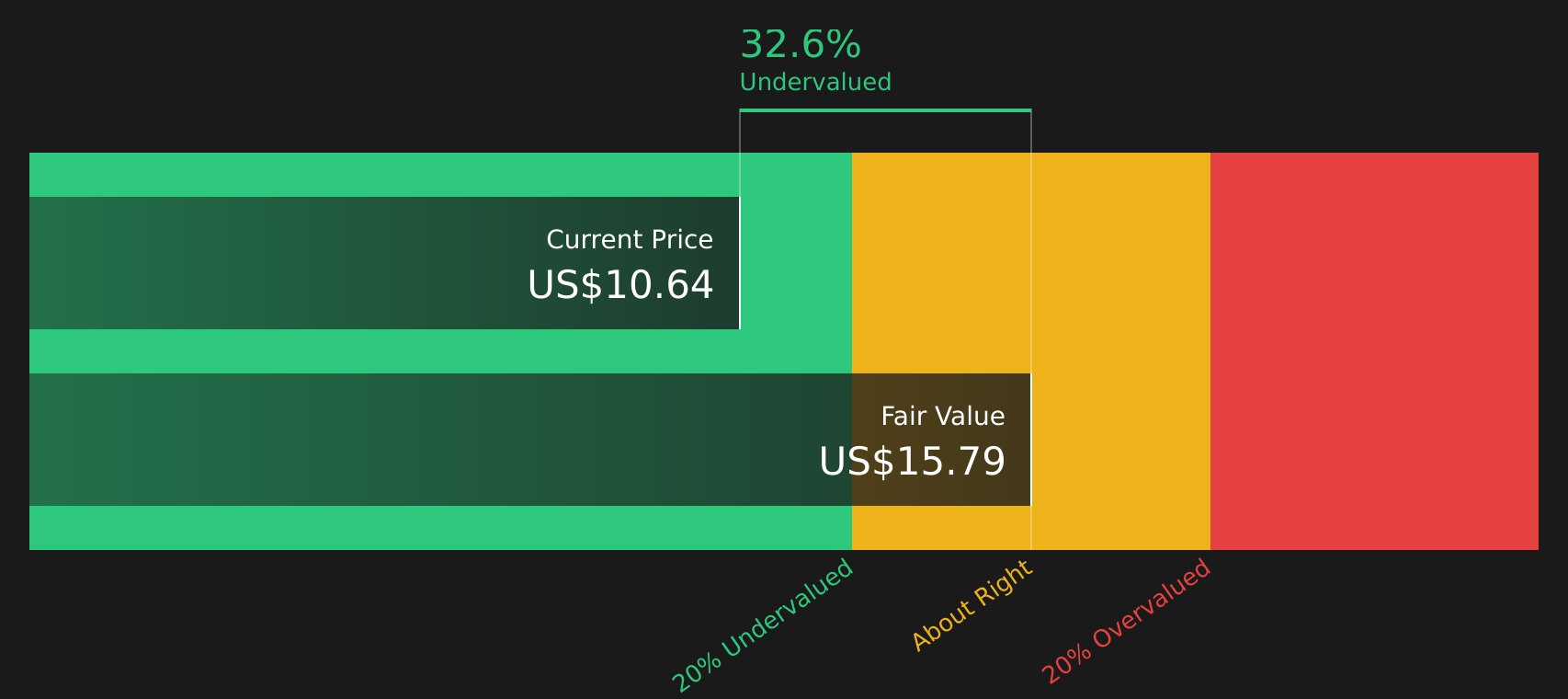

With LSB Industries trading at $14.56 and sitting about 4% below the analyst price target and around 13% below an estimated intrinsic value, the key question is whether this gap signals a buying opportunity or simply reflects markets already pricing in future growth.

Most Popular Narrative: 31% Overvalued

LSB Industries last closed at $14.56, compared to a widely followed fair value estimate of $11.15 that is based on detailed earnings and valuation assumptions.

Bullish analysts are lifting price targets, which signals growing comfort with their updated assumptions on discount rate, revenue, margins, and future P/E levels.

The internal fair value increase to US$11.15 implies that, based on their models, there is room between current market pricing and what they view as justified by fundamentals.

Want to understand why a higher future P/E and modest margin improvement are so central here? The entire narrative hinges on a tight blend of revenue forecasts, profitability shifts, and valuation multiples that are usually reserved for stronger growth profiles. Curious which specific earnings path and discount rate have been baked into that $11.15 figure and how they stack up against current pricing tension?

Result: Fair Value of $11.15 (OVERVALUED)

However, this depends on effective execution. Volatile natural gas prices and substantial ongoing plant investment could both pressure margins and challenge the fair value argument.

Another View Using The SWS DCF Model

The earlier fair value of $11.15 suggests LSB Industries is 31% overvalued, yet the SWS DCF model points the other way, with an estimated future cash flow value of $16.81, or about 13% above the current $14.56 price. Two methods, two very different stories. Which one lines up better with your expectations for cash generation and risk?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out LSB Industries for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 53 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

Consider whether to remain cautious or to challenge the mixed signals on value, growth, risks, and rewards. Either way, act quickly and thoroughly stress test the full 2 key rewards and 2 important warning signs.

Looking for more investment ideas?

If you stop with just one stock, you could miss opportunities that suit your goals even better, so take a few minutes to scan a wider set of ideas.

- Target steadier potential returns by checking companies that show up in the 73 resilient stocks with low risk scores.

- Hunt for stronger value by reviewing companies flagged in the 53 high quality undervalued stocks.

- Spot resilient balance sheets by scanning the solid balance sheet and fundamentals stocks screener (43 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.