A Look At Lumen Technologies (LUMN) Valuation After CEO Share Buy, Earnings Beat And AT&T Asset Sale

Lumen LUMN | 7.80 7.81 | +0.13% +0.13% Post |

Lumen Technologies (LUMN) is back in focus after CEO Kate Johnson bought roughly US$500,000 of stock following a post earnings sell off, alongside an earnings beat and a major asset sale to AT&T.

At a share price of US$8.06, Lumen’s 29.4% 1 day share price return stands out against a weaker 90 day share price return of 23.2%. The 1 year total shareholder return of 61.5% and 3 year total shareholder return of just over 2x suggest longer term holders have seen very different outcomes over time, as investors react to the earnings beat, the AT&T asset sale and fresh leadership moves including the appointment of a new Chief Revenue Officer.

If this kind of turnaround story has your attention, it might be a good moment to see what else is out there via our screener of 22 top founder-led companies.

The question now is whether Lumen’s sharper focus, cost cuts and debt reduction are already reflected in a US$8.06 share price, or if the recent surge still leaves room in the event that markets are underestimating future growth.

Most Popular Narrative: 11.4% Overvalued

Compared with the most followed fair value estimate of $7.23, Lumen’s $8.06 close prices in above that narrative, which leans on a higher discount rate and cautious revenue assumptions.

Lumen's large pipeline of AI-driven network infrastructure and Platform Connectivity Fiber (PCF) contracts, particularly with hyperscalers and data center providers, positions the company to capture long-duration, higher-margin recurring revenues from explosive data growth, benefiting long-term revenue and margin expansion.

Want to see what kind of revenue path and margin profile this narrative is baking in? The fair value hinges on shrinking top line, higher profitability and a compact earnings multiple that sits well below many telecom peers. The full story shows how those moving parts fit together.

Result: Fair Value of $7.23 (OVERVALUED)

However, there are still clear watchpoints, including ongoing revenue contraction and legacy product declines, that could outweigh modernization efforts and pressure the turnaround story.

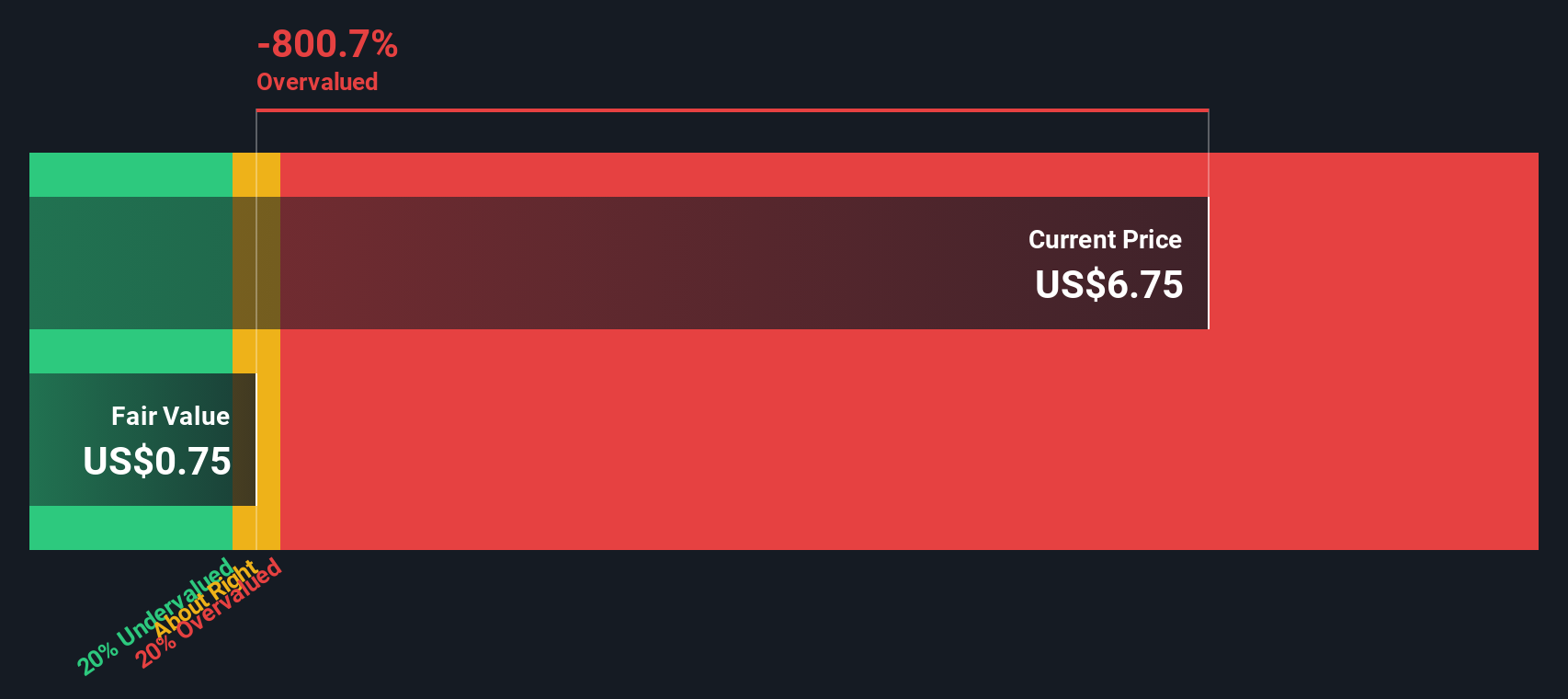

Another Take: Market Price Versus Our Cash Flow View

Here is where things get interesting. While the popular fair value narrative sits at $7.23 and describes Lumen as overvalued at $8.06, our DCF model is far more cautious, indicating a future cash flow value of just $1.15 per share. This points to meaningful downside if that view proves closer to reality. As an investor, which story feels more realistic to you, and what would need to change in the business for your view to shift?

Build Your Own Lumen Technologies Narrative

If you look at the numbers and reach a different conclusion, or simply prefer to piece things together yourself, you can build a custom view of Lumen’s story in just a few minutes, starting with Do it your way

A great starting point for your Lumen Technologies research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

Ready For More Investment Ideas?

If you are weighing up Lumen, it can be helpful to compare it with other types of opportunities so you can see where it really stands in your portfolio.

- Target potential mispricings by checking companies our screener flags as 52 high quality undervalued stocks with solid fundamentals backing up their current prices.

- Strengthen your income stream by reviewing our hand picked list of 14 dividend fortresses that focus on yield and resilience.

- Prioritize resilience by scanning 82 resilient stocks with low risk scores that our models score well on balance sheet strength and risk indicators.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.