A Look At Lumentum (LITE) Valuation After Earnings Beat And Strong Growth Guidance

Lumentum Holdings, Inc. LITE | 826.88 | +8.14% |

Why Lumentum’s latest earnings are drawing fresh attention

Lumentum Holdings (LITE) is back in focus after reporting second quarter results that exceeded expectations and issuing third quarter guidance that points to sharply higher revenue and profitability.

The company now expects third quarter fiscal 2026 net revenue between US$780 million and US$830 million, alongside a projected adjusted operating margin of 30% to 31% and earnings per share of US$2.15 to US$2.35.

The latest earnings beat and upbeat guidance have coincided with a sharp re-rating, with a 90 day share price return of 121.08% and a very large 1 year total shareholder return. The recent 1 day decline of 2.78% comes after a 59.67% 30 day share price gain.

If Lumentum’s move has you thinking about other AI infrastructure names, this could be a useful moment to scan 33 AI infrastructure stocks as potential candidates for further research.

With Lumentum trading near its recent highs, a roughly 34% intrinsic discount estimate and a price target now slightly below the current US$561.13 raise a key question for investors: is there still a buying opportunity here, or has the market already priced in future growth?

Most Popular Narrative: 61.1% Overvalued

At $561.13, Lumentum trades well above the most followed fair value estimate of roughly $348, which frames the current rally in a very different light.

Recent research on Lumentum presents a mix of optimism around long term growth drivers and caution on near term execution and valuation. Here is how the Street is framing the story right now.

Want to see what underpins that gap between fair value and price? The narrative leans on rapid revenue expansion, richer margins, and a premium future earnings multiple. Curious how those pieces fit together and what assumptions really drive that $348 figure? Read the full story behind the model.

Result: Fair Value of $348.38 (OVERVALUED)

However, this hinges on concentrated hyperscaler demand and tight production capacity. As a result, any order pullback or execution stumble could quickly challenge that fair value story.

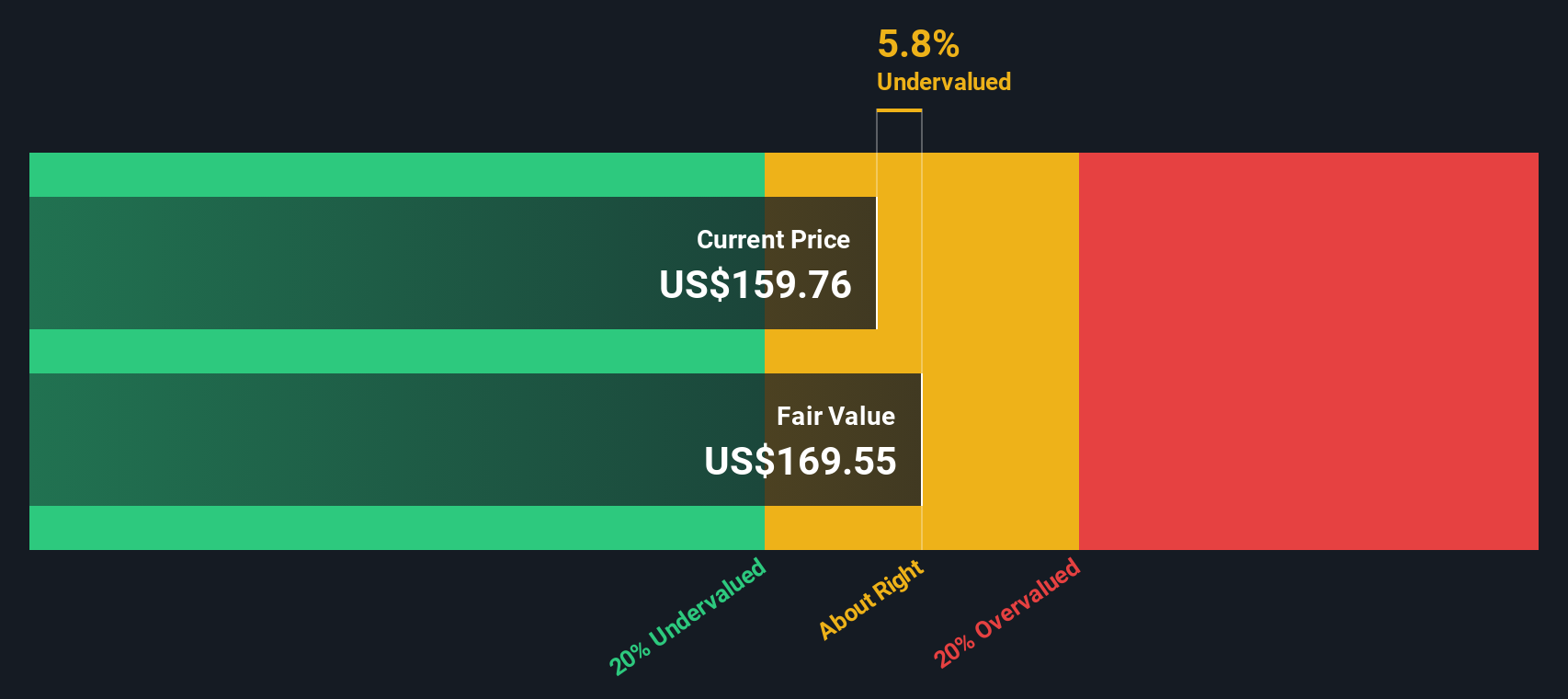

Another View: Cash Flows Tell a Very Different Story

The narrative-based fair value of about $348.38 paints Lumentum as 61.1% overvalued, yet our DCF model points the other way. On that cash flow view, Lumentum at $561.13 sits roughly 34% below an estimated value of $852.24, which flags a wide gap for investors to think through. Which lens do you trust more, the story-driven multiple or the cash flow math?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Lumentum Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Lumentum Holdings Narrative

If you see the story differently or prefer to weigh the numbers yourself, you can build a custom view in just a few minutes: Do it your way.

A great starting point for your Lumentum Holdings research is our analysis highlighting 3 key rewards and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Lumentum has sharpened your thinking, this is a good moment to widen your net and pressure test your next moves with a few targeted screeners.

- Spot potential bargains early by scanning screener containing 24 high quality undiscovered gems that pair solid fundamentals with relatively low market attention.

- Lock in potential income streams by reviewing 14 dividend fortresses that focus on higher yielding companies with resilient payouts.

- Sleep easier by checking 83 resilient stocks with low risk scores that are designed to surface companies with lower overall risk scores for a steadier ride.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.