A Look At Maase (MAAS) Valuation After Its Sharp Year To Date Share Price Surge

Maase Inc MAAS | 0.00 |

Maase (MAAS) has drawn fresh attention after a sharp recent move in its stock, prompting investors to look more closely at this China focused financial services and technology platform listed on the Nasdaq.

The recent surge in Maase’s share price, including a 9.22% 1 day share price return and 103.43% year to date share price return, points to strengthening momentum as investors reassess its China focused financial technology platform.

If Maase’s move has your attention, this could be a good moment to broaden your watchlist with other fast changing opportunities in financial technology and AI related platforms by checking out 63 profitable AI stocks that aren't just burning cash

With Maase posting a very large year-to-date gain and reporting revenue of CN¥3.483 and a loss of CN¥1.775, investors may now need to consider whether the stock remains mispriced or whether markets are already incorporating expectations of future growth into its valuation.

Preferred Price to Book Multiple of 18.4x: Is it justified?

On a P/B basis, Maase currently screens as expensive, with its 18.4x multiple sitting well above both the US Insurance industry average of 1.6x and a peer average of 4.8x.

P/B compares the company’s market value to its book value, which for financial and capital intensive businesses is often used as a rough gauge of how the market values their assets and equity base. When the multiple is this high, it usually signals that investors are paying a premium relative to the accounting value of net assets.

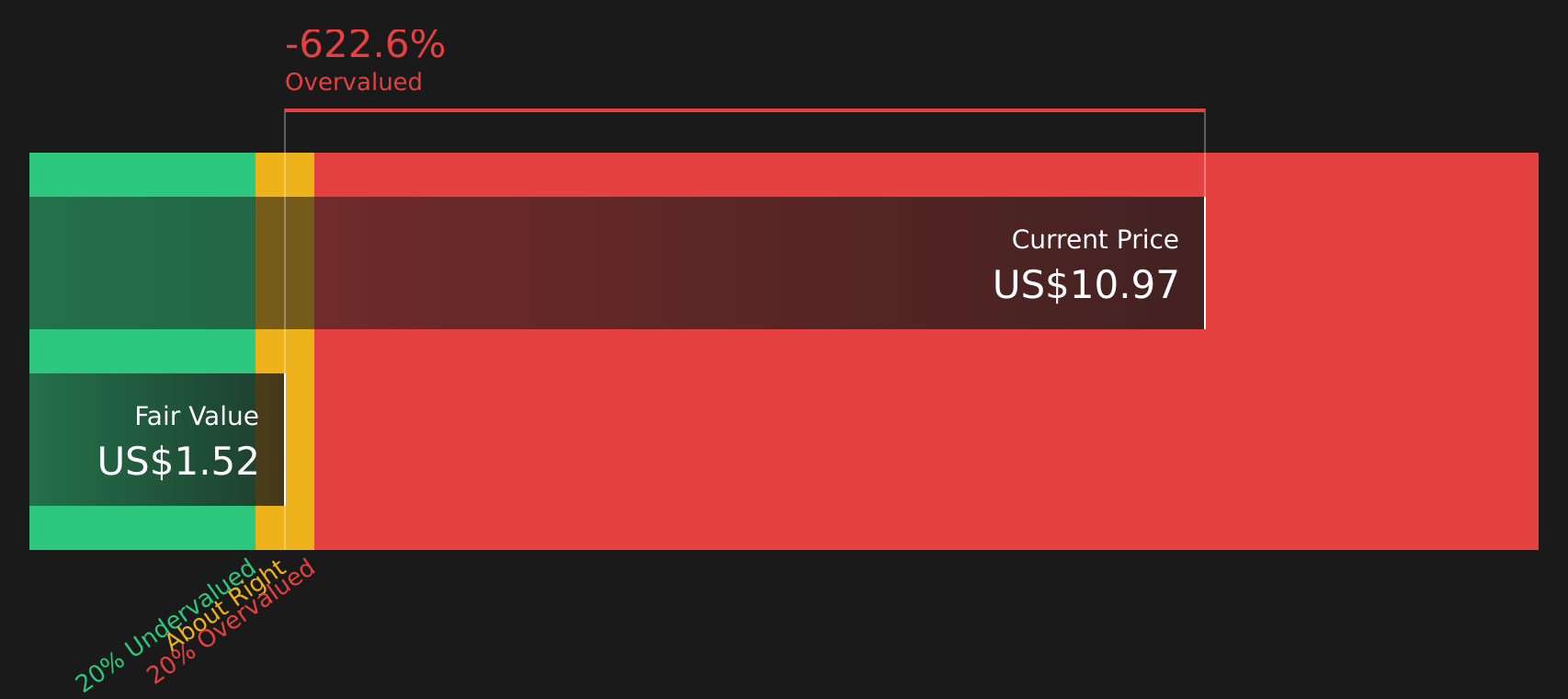

For Maase, that premium comes despite the company reporting a loss of CN¥1.775 on revenue of CN¥3.483, less than three years of public financial history, and a negative return on equity of 0.092%. The SWS DCF model also currently values the stock at $1.51 per share compared with the last close of $11.85. This comparison suggests the current price is well above that cash flow based estimate.

Against that backdrop, the 18.4x P/B multiple is not just slightly higher than benchmarks. It is far above both the 1.6x sector average and the 4.8x peer group level, which implies the market is assigning a substantial premium relative to comparable insurance and financial services stocks.

Result: Price-to-book of 18.4x (OVERVALUED)

However, the recent rally sits against limited public financial history, a reported loss of CN¥1.775, and a market cap above US$5.2b, which could challenge confidence.

Another angle on value

While the 18.4x P/B ratio suggests Maase trades at a heavy premium to both the US Insurance industry at 1.6x and peers at 4.8x, the SWS DCF model also points to a stretched picture, with an estimated value of $1.51 per share versus a market price of $11.85. That gap frames Maase as overvalued on two very different yardsticks. The real question is what exactly investors think they are paying up for.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Maase for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 49 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of rich valuation and limited history feels difficult to interpret, consider reviewing the data now and forming your own view using our breakdown of 1 key reward and 3 important warning signs

Looking for more investment ideas?

If Maase has sharpened your focus, now is the time to widen your search using structured stock lists that surface opportunities you might otherwise miss.

- Target stability first by screening for companies in the 67 resilient stocks with low risk scores that may align with a more cautious approach to equity investing.

- Hunt for overlooked potential with the screener containing 21 high quality undiscovered gems and see which lesser known stocks show strong underlying fundamentals.

- Focus on financial strength by filtering companies through the solid balance sheet and fundamentals stocks screener (46 results) to spot businesses with healthier balance sheets and cleaner financial profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.