A Look At Martin Marietta Materials (MLM) Valuation After Recent Share Price Moves

Martin Marietta Materials, Inc. MLM | 597.18 | -0.29% |

Why Martin Marietta Materials is on investors’ radar today

Martin Marietta Materials (MLM) has attracted fresh attention after recent share price moves, with the stock showing mixed returns over the past week, month and past 3 months relative to its longer term record.

At a share price of $649.25, Martin Marietta Materials has seen a 5.24% 90 day share price return, while its 1 year total shareholder return of 20.44% and 3 year total shareholder return of 83.78% point to momentum that has been building over time rather than fading.

If recent moves in construction materials stocks have your attention, it could be a good moment to widen your search and check out fast growing stocks with high insider ownership.

With a recent 90 day return of 5.24% and a price of $649.25 sitting close to analyst targets, the key question is simple: is Martin Marietta still mispriced, or is the market already discounting future growth?

Most Popular Narrative: 4.6% Undervalued

With Martin Marietta Materials closing at $649.25 against a narrative fair value of $680.88, the current price sits slightly below that implied level. This puts more focus on how resilient its earnings story might be over the next few years.

The exchange of cement and ready mix assets for high quality aggregate operations in Virginia, Missouri, Kansas, and Vancouver, BC, strategically increases Martin Marietta's exposure to advantaged geographies with strong barriers to entry and pricing power, expected to enhance margins and support stable earnings growth over time.

Want to see what kind of revenue profile, margin lift, and future earnings base this narrative is baking in? The full story links those operational shifts to a valuation built on multi year growth, richer profitability, and a premium multiple that is not usually attached to a traditional building materials name.

Result: Fair Value of $680.88 (UNDERVALUED)

However, you still need to watch for weaker construction demand or tighter government infrastructure budgets, as these could challenge the earnings and valuation story investors are watching.

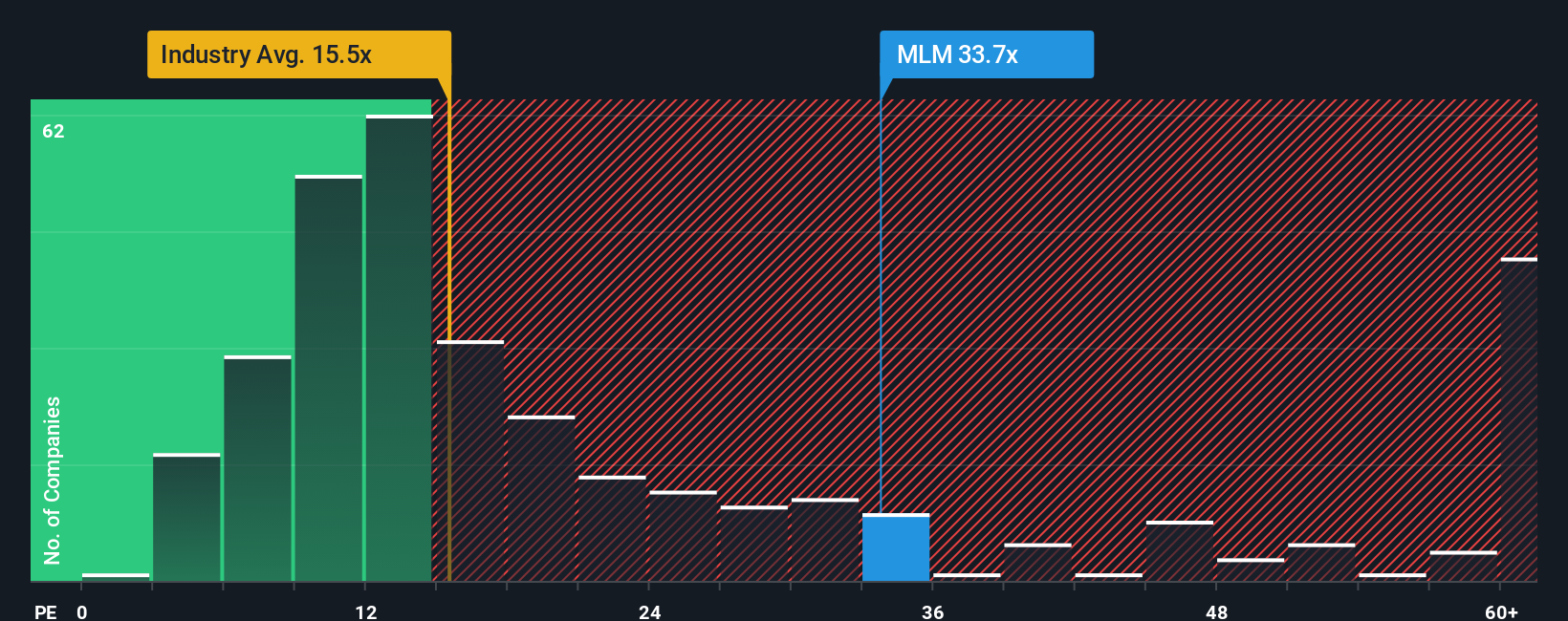

Another View: Earnings Multiple Paints A Richer Picture

The narrative fair value implies Martin Marietta Materials is modestly undervalued, but the P/E ratio of 33.1x tells a different story. It sits well above the estimated fair ratio of 23.3x, the global Basic Materials average of 15.6x, and the peer average of 25.3x. This points to meaningful valuation risk if growth or margins disappoint. Which signal do you think deserves more weight right now?

Build Your Own Martin Marietta Materials Narrative

If this take does not quite line up with your own thinking, or you prefer to lean on your own research, you can pull up the same numbers, stress test the assumptions, and shape a custom thesis around what matters most to you in just a few minutes with Do it your way.

A great starting point for your Martin Marietta Materials research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you stop with just one company, you could miss opportunities that fit your style even better. Put the Simply Wall St Screener to work for you today.

- Spot potential value plays by zeroing in on these 879 undervalued stocks based on cash flows that align with your return expectations and risk tolerance.

- Explore long term tech themes by scanning these 24 AI penny stocks that are exposed to artificial intelligence areas you want in your portfolio.

- Target income focused opportunities by filtering for these 13 dividend stocks with yields > 3% that might suit a yield driven strategy.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.