A Look At McDonald's (MCD) Valuation As Q4 Earnings Expectations Build

McDonald's Corporation MCD | 306.26 | +1.00% |

Dividend declaration and what it means for McDonald's (MCD) shareholders

McDonald's (MCD) has drawn fresh attention after its board declared a quarterly cash dividend of US$1.86 per share, payable on March 17, 2026, to shareholders of record on March 3.

For current and prospective investors, this payout decision sits alongside upcoming Q4 earnings, prior quarterly performance, and ongoing expansion and leadership moves. Together, these factors provide several angles to consider when evaluating how the stock may fit into a portfolio.

At a share price of US$327.16, McDonald's has recently shown firm momentum, with a 30 day share price return of 7.56% and a 1 year total shareholder return of 13.76%, while the 5 year total shareholder return of 71.45% reflects how longer term holders have fared.

If this dividend news has you thinking about where else steady demand and brand strength might matter, it could be worth scanning our 22 top founder-led companies as another source of ideas.

With McDonald's trading at US$327.16 and sitting close to analyst price targets, plus fresh dividend income on the table, you have to ask: is there still upside here, or is the market already pricing in future growth?

Most Popular Narrative: 1.2% Undervalued

McDonald's last closed at $327.16, while the most followed narrative pegs fair value close by at $331.20, suggesting only a small valuation gap.

The company's ongoing refranchising and asset light model, paired with disciplined global cost management and G&A efficiencies enabled by new centralized platforms, reinforces stable free cash flow and structurally higher operating margins, increasing the company's ability to return capital to shareholders and boosting long term earnings growth.

Want to see what kind of revenue growth, margin profile, and earnings multiple have to line up to support that fair value? The full narrative spells out a tight set of assumptions around future cash generation and profitability that go well beyond the recent dividend headline.

Result: Fair Value of $331.20 (UNDERVALUED)

However, the story can change quickly if low-income guest traffic weakens further or if higher beef and labor costs squeeze restaurant-level profitability.

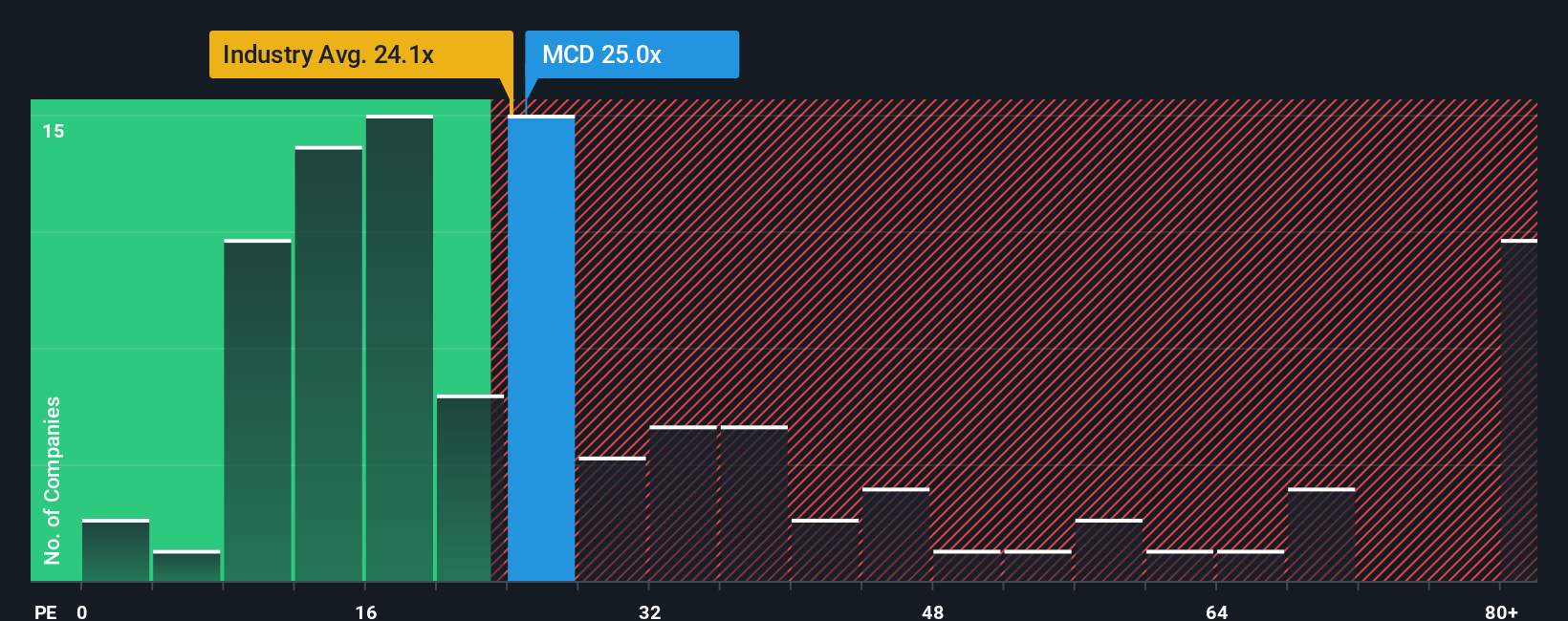

Another View: Rich P/E Leaves Less Room For Error

While the most followed narrative points to a fair value around US$331.20 and calls McDonald's slightly undervalued, the market is already assigning a P/E of 27.7x, above the US Hospitality average of 22x, even though it sits below both peers at 59.1x and a fair ratio of 32.3x.

This mix of premium versus the industry, discount versus peers, and room to move toward the fair ratio highlights a valuation that is neither clearly stretched nor obviously cheap. The key question is whether you think future execution and growth can justify staying at the high end of the range.

Build Your Own McDonald's Narrative

If you see the data differently or prefer to test your own assumptions, you can quickly build a custom McDonald's view and Do it your way in just a few minutes.

A great starting point for your McDonald's research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If McDonald's has sharpened your focus on quality, do not stop here. Use our screeners to spot other opportunities that could round out your portfolio.

- Target dependable income streams by checking out 14 dividend fortresses that may appeal if you want yields with an emphasis on resilience.

- Hunt for potential value opportunities with 53 high quality undervalued stocks that line up quality fundamentals with prices that might still look reasonable.

- Prioritize capital preservation first by scanning 86 resilient stocks with low risk scores that aim to keep risk scores in check while you search for ideas.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.