A Look At MercadoLibre (NasdaqGS:MELI) Valuation As Strong Fundamentals Draw Fresh Investor Interest

MercadoLibre, Inc. MELI | 1715.52 | -0.20% |

Recent commentary on MercadoLibre (MELI) has focused on its business fundamentals, including rising buyer engagement, higher spending per user and a free cash flow margin of 32.7%, prompting fresh attention on the stock.

At a share price of $1,970.15, MercadoLibre has recently seen a 1 month share price return of 9.56% and a 7 day share price return of 8.27% decline, which contrasts with a relatively flat year to date share price return and a stronger 3 year total shareholder return of 78.30%. This suggests that long term holders have seen meaningful gains even as near term momentum has cooled.

If MercadoLibre’s mix of e commerce and digital payments has caught your eye, you might also want to scan our screener of 22 top founder-led companies for other compelling business models run by founders.

So with MercadoLibre combining rising user engagement, a 32.7% free cash flow margin, and recent short-term share price declines, is the current valuation an opening for patient investors, or is the market already pricing in future growth?

Most Popular Narrative: 29.8% Undervalued

Against MercadoLibre’s last close of $1,970.15, the most widely followed narrative points to a fair value of about $2,805, framing a sizeable valuation gap that rests on how its ecosystem scales over time.

Cross platform integration of commerce, fintech, and advertising demonstrated by accelerated ad revenue growth and enhanced tools for sellers deepens ecosystem stickiness, reinforcing customer lifetime value and delivering operating leverage that can support above consensus net income and earnings growth.

Curious what kind of growth, margin lift, and earnings power this narrative is baking in over the next few years, and how that ties back to that higher fair value label, without assuming everything goes perfectly.

Result: Fair Value of $2,805.46 (UNDERVALUED)

However, the picture is not one sided. Rapid growth in the credit portfolio and heavier shipping and marketing spend could pressure margins if revenue or asset quality underwhelm.

Another View On MercadoLibre’s Valuation

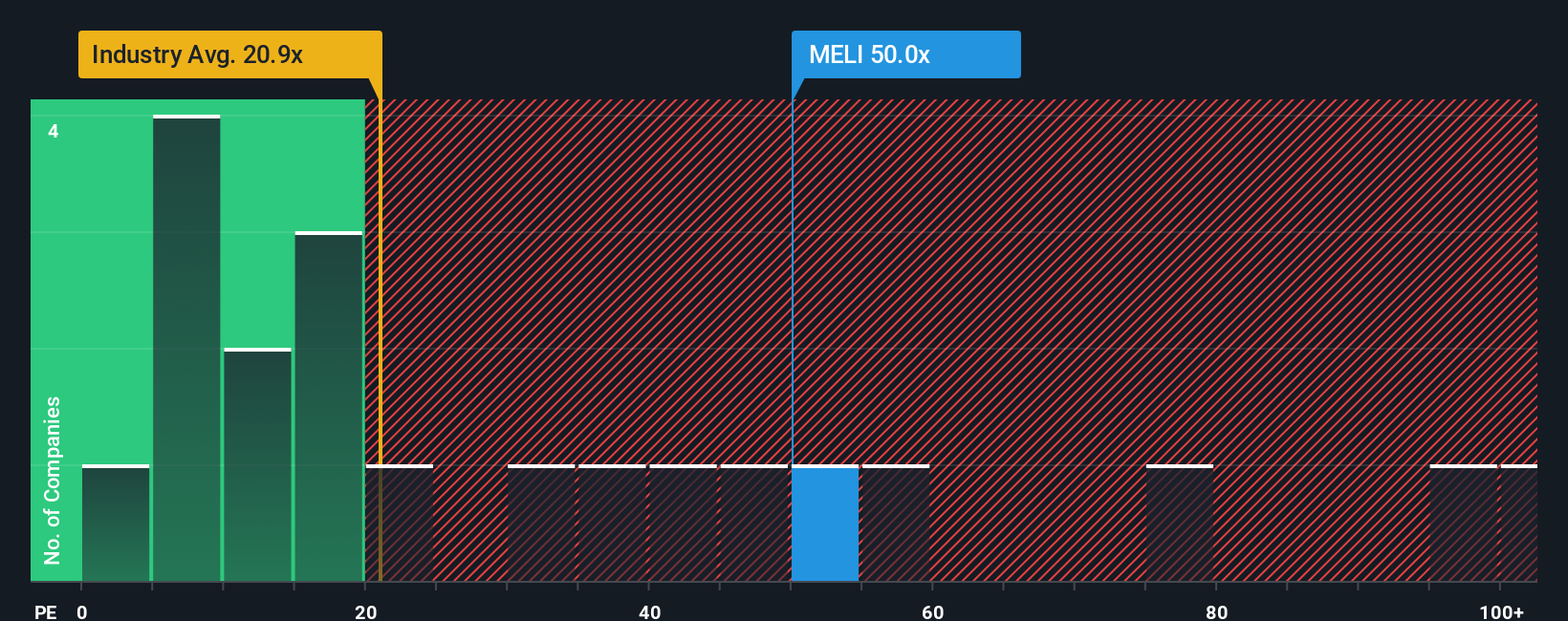

That 29.8% gap to fair value is one story. The P/E ratio tells a very different one, with MercadoLibre trading at 48.1x earnings versus 18.4x for the North American Multiline Retail industry, 36.8x for peers, and a fair ratio of 33.8x. Is the market generously paying up for quality, or just stretching the risk?

Build Your Own MercadoLibre Narrative

If you see the numbers differently or prefer to put your own spin on the story, you can build a personalized view in just a few minutes: Do it your way

A great starting point for your MercadoLibre research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If MercadoLibre has sharpened your thinking, do not stop here. Use the Simply Wall St screener to spot other opportunities that fit your style before they move.

- Target potential value opportunities by scanning our list of 52 high quality undervalued stocks that combine quality fundamentals with appealing pricing.

- Prioritise resilience first by reviewing 82 resilient stocks with low risk scores that score well on our risk checks and may suit a more cautious approach.

- Spot potential future leaders early by checking our screener containing 24 high quality undiscovered gems with strong fundamentals that the market may not be focusing on yet.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.