A Look At Micron Technology (MU) Valuation As AI HBM Demand Surges And 2026 Supply Sells Out

Micron Technology, Inc. MU | 366.24 | -0.44% |

Micron Technology (MU) is back in focus after its high bandwidth memory supply for 2026 sold out, production ramped earlier than planned, and analysts highlighted tight AI driven demand and constrained industry capacity.

The latest HBM news lands on top of a strong run, with Micron’s 1 day share price return of 9.94% and 30 day return of 18.64% adding to a 73.18% 90 day move. Its 1 year total shareholder return is very large, indicating powerful momentum rather than a short lived spike.

If AI hardware is high on your watchlist, this is a good moment to see what else is moving and scan 34 AI infrastructure stocks as potential additions to your research list.

With Micron now at US$410.34 and trading at a discount to its average analyst target, yet carrying an intrinsic value premium and a long list of bullish forecasts, investors have to ask: Is there still an opportunity here, or is the market already pricing in years of AI fueled growth?

Most Popular Narrative: 36.7% Overvalued

According to the most followed Micron narrative, a fair value of $300.21 sits well below the last close at $410.34, setting up a clear valuation gap for investors to judge.

Micron Technology stands at a fascinating crossroads where the promise of a powerful, AI-driven supercycle meets the persistent risks of a volatile industry. The core investment thesis is a bet that the structural, long-term demand for high-performance memory, particularly HBM, will be strong enough to fundamentally change the company's profitability and mitigate the historical boom-and-bust cycles.

Curious what kind of revenue trajectory and profitability shift would need to support that valuation gap, and how rich a future profit multiple this narrative leans on to justify a fair value far below today’s price? The full story connects those assumptions directly to Micron’s AI centric product mix and expected earnings power.

Result: Fair Value of $300.21 (OVERVALUED)

However, this hinges on AI memory demand staying tight and on rivals like Samsung and SK Hynix avoiding aggressive capacity builds or price competition that could erode Micron’s economics.

Another View: Market-Based Valuation Looks More Generous

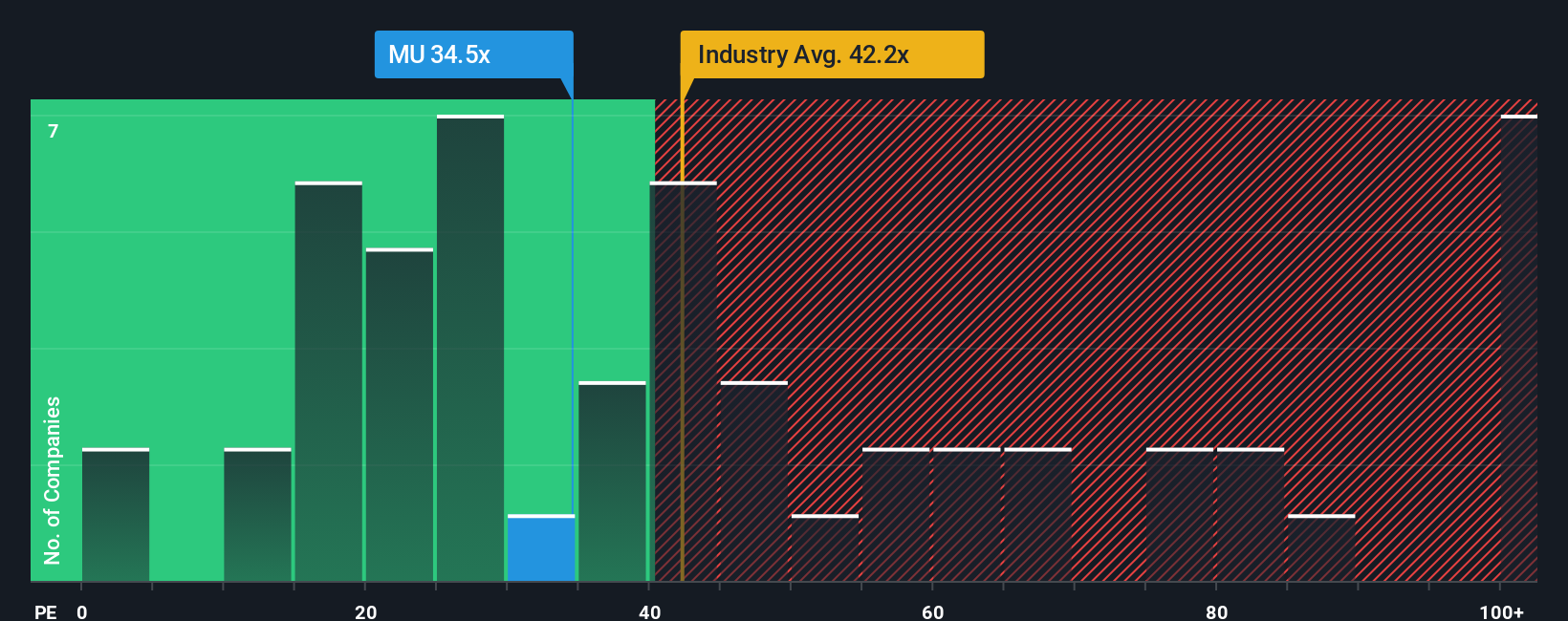

While the leading narrative suggests Micron is 36.7% overvalued versus a $300.21 fair value, the market based P/E story is quite different. At 38.8x earnings, Micron trades well below the Semiconductor industry at 46.4x and far below its own fair ratio of 62.2x. This indicates a valuation that could still shift a long way before sentiment truly looks stretched. So is the share price expensive, or is the market still leaving some headroom?

Build Your Own Micron Technology Narrative

If you are looking at the same numbers and reaching a different conclusion, that is the point. You can put your own view into a full narrative in just a few minutes and Do it your way.

A great starting point for your Micron Technology research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Ready To Find Your Next Idea?

If Micron has your attention, do not stop here. Broaden your watchlist with a few focused stock ideas that might otherwise slip past you.

- Spot potential mispricings by reviewing companies our screener flags as 51 high quality undervalued stocks that could be worth a closer look.

- Prioritize resilience by scanning 85 resilient stocks with low risk scores that score well on our risk metrics and may better fit a steadier investment style.

- Get ahead of the crowd by checking our screener containing 24 high quality undiscovered gems before they hit more mainstream watchlists.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.