A Look At NCR Atleos (NATL) Valuation After Recent Share Price Momentum

NCR Atleos Corporation NATL | 0.00 |

Why NCR Atleos (NATL) is on investors’ radar today

NCR Atleos (NATL) has attracted fresh attention after recent trading left the stock at a last close of $44.52, with returns of 0.3% over the past day and about 19% over the past 3 months.

For readers tracking company level fundamentals, NCR Atleos reports annual revenue of $4.354b and net income of $162.0m, alongside a reported value score of 1 that may prompt closer comparison with other financial technology names.

Those short term moves sit alongside a 30 day share price return of 1.69% and a 90 day share price return of 19.36%, while the 1 year total shareholder return of 54.21% points to strong momentum building around the story.

If NCR Atleos’s recent run has you thinking about where else capital could work hard, this is a good moment to scan 37 AI infrastructure stocks for other potential opportunities.

With a value score of 1, US$4.354b in revenue and annual net income of US$162m, the key question now is simple: is NCR Atleos still underappreciated, or are markets already pricing in future growth?

Most Popular Narrative: 11.4% Undervalued

Analysts see NCR Atleos’s fair value at $50.27, above the last close of $44.52. This puts the focus firmly on what is driving that gap.

High recurring revenue mix (over 70% in Q2), significant productivity gains through AI-driven service optimization, and a rapidly scaling backlog are driving strong margin expansion and robust free cash flow, underpinning announced share buybacks and sustained EPS growth, suggesting current valuation does not reflect enhanced long-term earnings power.

It is worth examining what kind of revenue runway, margin profile, and profit multiple are incorporated into that fair value. The narrative leans on specific projections, not vague optimism.

Result: Fair Value of $50.27 (UNDERVALUED)

However, there are clear watchpoints too, including faster adoption of fully digital banking and more intense fintech competition that could challenge NCR Atleos’s ATM focused model.

Another Way to Look at Value

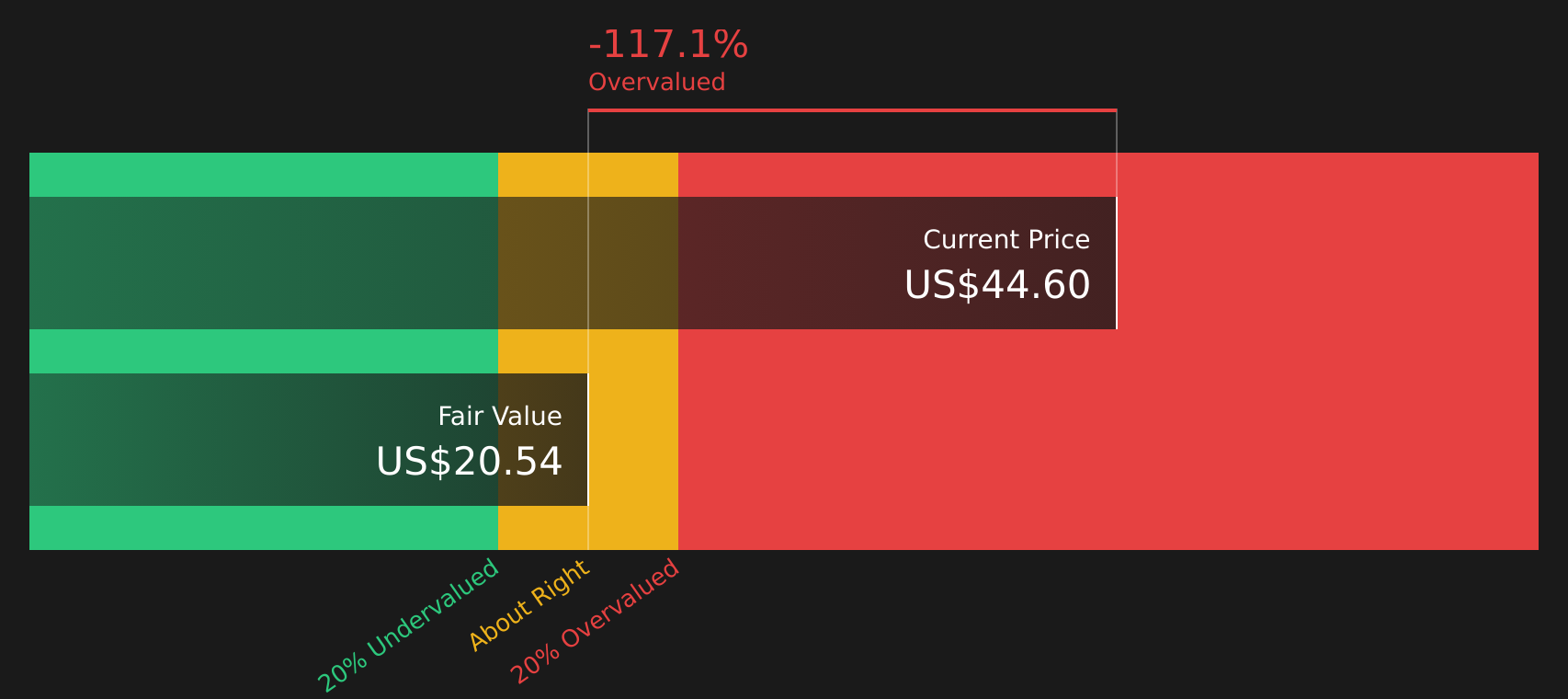

Analysts see NCR Atleos as 11.4% undervalued at $50.27, yet our DCF model points the other way, with an estimate of future cash flow value at $20.68. That is a big gap, so which story do you think better fits how this business actually generates cash?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out NCR Atleos for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals around value and expectations, this is a good time to check the numbers yourself and weigh both sides of the story using 2 key rewards and 2 important warning signs

Ready to hunt for your next idea?

If NCR Atleos has you thinking more broadly, treat this as your cue to scan other well researched ideas before the next move leaves you on the sidelines.

- Target potential mispricings by checking companies that screen as 51 high quality undervalued stocks based on their cash flows and balance sheets.

- Prioritize resilience by focusing on businesses in the 67 resilient stocks with low risk scores that show steadier fundamentals and fewer red flags.

- Spot under followed opportunities by reviewing the screener containing 25 high quality undiscovered gems where quality metrics look strong but attention is still limited.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.