A Look At New Oriental Education NYSE EDU Valuation After Tiger Pacific Exit And Recent Earnings Growth

New Oriental Education & Technology Group, Inc. Sponsored ADR EDU | 0.00 |

Tiger Pacific Capital’s decision to fully exit New Oriental Education & Technology Group (EDU) in the first quarter, as disclosed in an SEC filing, has refocused attention on the stock’s recent financial and operational updates.

At a share price of US$47.08, New Oriental’s 1-day share price return of 2.82% and 7-day gain of 1.40% sit against a 30-day decline of 12.52% and year to date drop of 18.59%. The 1-year total shareholder return of 5.49% and 3-year total shareholder return of 17.01% point to a mixed picture where recent momentum has faded despite earlier gains, with Tiger Pacific’s exit and recent revenue and income growth updates likely shaping how investors view both the company’s growth potential and risk profile.

If you are reassessing education and tech exposure after these moves, it could be a good moment to broaden your search with 20 top founder-led companies

With the stock down 18.59% year to date despite annual revenue growth of 8.53% and net income growth of 17.31%, you have to ask: Is New Oriental undervalued, or is the market already pricing in its future growth?

Most Popular Narrative: 13.7% Undervalued

With New Oriental trading at $47.08 against a narrative fair value of $54.54, the current gap puts the company’s earnings outlook under the microscope.

The bearish analysts expect earnings to reach $683.9 million (and earnings per share of $4.89) by about April 2029, up from $380.5 million today. However, there is some disagreement amongst the analysts with the more bullish ones expecting earnings as high as $1.0 billion.

Curious how this earnings path is built? Revenue, margins and the future P/E all pull in different directions. The key assumptions might surprise you.

Result: Fair Value of $54.54 (UNDERVALUED)

However, that 13.7% discount relies on bearish assumptions, and stronger segment revenue growth, along with higher profit margins, could challenge the idea that the stock is mispriced.

Another Angle on Value: Earnings Multiple Sends a Different Signal

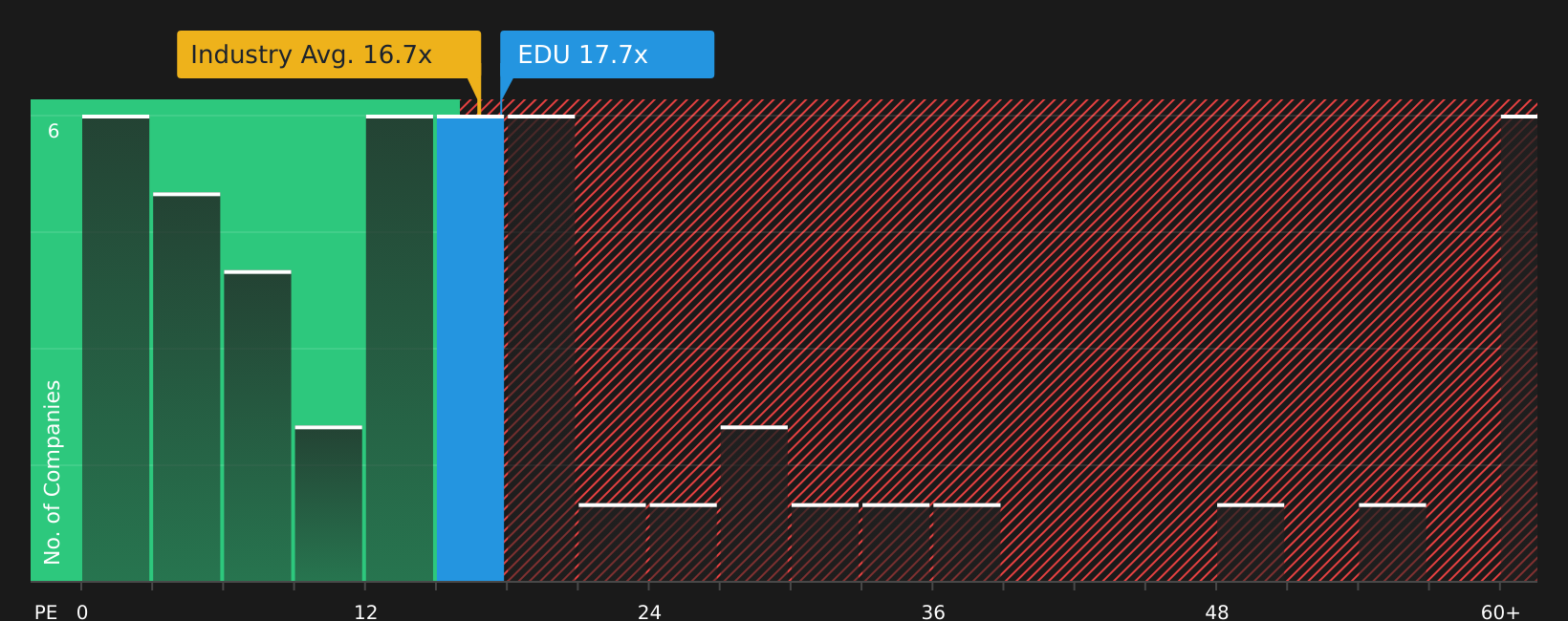

While the narrative fair value of US$54.54 suggests the stock is 13.7% undervalued, the earnings multiple tells a more cautious story. At a P/E of 17.8x versus 14.3x for peers and 16x for the wider US Consumer Services industry, EDU trades on a richer earnings tag than both.

Set against a fair ratio of 25x, the current P/E still sits well below where the market could move toward if sentiment and assumptions shift. That gap can look like either valuation headroom or a warning that expectations are already high, depending on how you see future execution.

For a closer look at how this pricing stacks up against fundamentals and peers, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Reading mixed signals from the share price and valuation gap is only the start. Now is the time to look through the details yourself. To understand what investors are optimistic about, take a closer look at the 4 key rewards

Looking for more investment ideas?

If you are serious about sharpening your portfolio after reviewing EDU, now is the moment to scan for fresh ideas before the market moves without you.

- Target value opportunities that combine quality and pricing by checking out 47 high quality undervalued stocks.

- Strengthen your portfolio core with companies that show robust finances through the solid balance sheet and fundamentals stocks screener (45 results).

- Spot early-stage potential that many investors miss by reviewing the screener containing 22 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.