A Look At Newegg Commerce (NEGG) Valuation After Chairman Detention And Governance Concerns

Newegg Commerce, Inc. - Common Shares NEGG | 38.03 | -2.51% |

Newegg Commerce (NEGG) is back in focus after the company disclosed that chairman and controlling shareholder He Zhitao has been detained and placed under investigation, with multiple law firms now reviewing potential securities law issues.

The governance shock around the chairman’s detention comes after a sharp 41.6% decline in the 90 day share price return and a 10.8% fall over the last day, even though the 1 year total shareholder return remains very large and the 3 year total shareholder return sits at 26.3%. This suggests longer term momentum has cooled as investors reassess risk.

If this kind of volatility has you looking beyond a single name, it could be a good moment to broaden your watchlist with fast growing stocks with high insider ownership.

With the stock dropping 41.6% over 90 days but still showing a very large 1 year return and a 3 year total return of 26.3%, investors may ask whether Newegg is now mispriced or whether the market is already factoring in any growth that may come next.

Preferred Price to Sales Ratio of 0.8x: Is it justified?

On a P/S of 0.8x at a last close of $49.5, Newegg Commerce screens cheaper than its peer group average but more expensive than the broader US specialty retail space.

The P/S ratio compares the company’s market value to its revenue, which can be useful when earnings are negative, as they are here. For an electronics focused e retailer generating $1,313.127m of revenue but reporting a net loss of $22.555m, the market is effectively putting more weight on sales scale than on current profitability.

Against direct peers, Newegg’s 0.8x P/S is below the peer average of 1.2x. This suggests the market is assigning a lower sales multiple than companies it is often grouped with. However, compared with the wider US specialty retail industry average of 0.5x, the same 0.8x looks rich, implying investors are paying a premium to the sector while the business remains unprofitable and carries higher risk funding with 100% of liabilities from external borrowing.

Result: Price to sales ratio of 0.8x (ABOUT RIGHT)

However, the chairman’s detention and the company’s current net loss of $22.555m could still unsettle confidence and raise further questions about governance and funding.

Another View using our DCF model

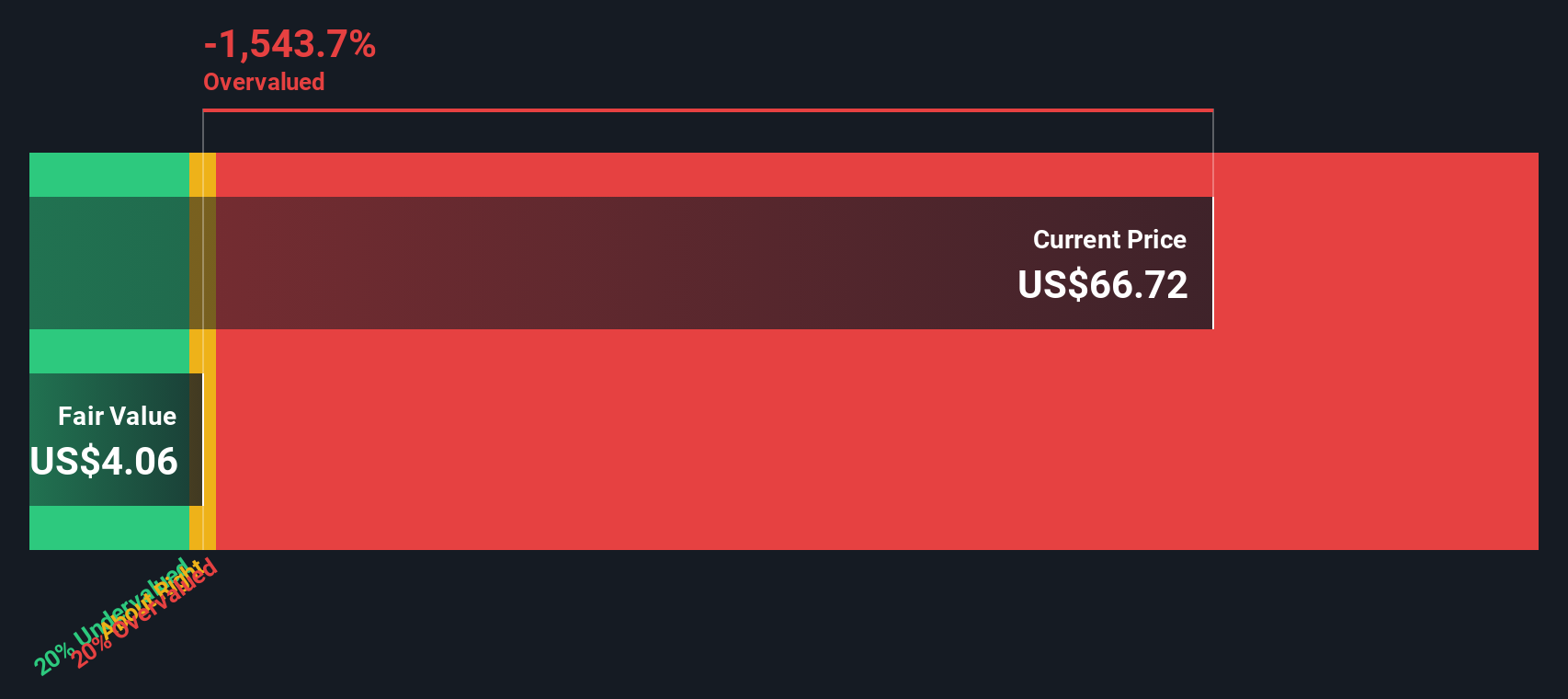

There is a twist when you look at Newegg through our DCF model. While the current P/S of 0.8x felt roughly in line with peers, the SWS DCF model estimates future cash flow value at $3.97 per share, compared to a market price of $49.5, which points to a very large premium. That kind of gap raises a simple question: which lens do you trust more when sentiment is this fragile?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Newegg Commerce for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 868 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Newegg Commerce Narrative

If you are not on board with this view or simply prefer to test your own assumptions against the numbers, you can pull the same data, pressure test the story yourself and build a version that fits your thinking in just a few minutes with Do it your way.

A great starting point for your Newegg Commerce research is our analysis highlighting 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Newegg has you rethinking concentration risk, do not stop here. Broaden your opportunity set now or you could miss out on more suitable fits.

- Scan for potential hidden value by checking out these 868 undervalued stocks based on cash flows that might align better with your return expectations and risk comfort.

- Ride major tech themes by reviewing these 25 AI penny stocks that are tied to artificial intelligence trends across different parts of the market.

- Add income focused options to your watchlist by assessing these 14 dividend stocks with yields > 3% that may offer more predictable cash payouts.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.