A Look At Nexa Resources (NEXA) Valuation After Temporary Atacocha Mine Disruption

Nexa Resources S.A. NEXA | 11.07 | +0.73% |

Mine disruption puts Nexa Resources (NEXA) in focus

Nexa Resources (NEXA) temporarily halted production at its Atacocha San Gerardo open pit mine after the Joraoniyoc community blocked road access. The company is concentrating operations on essential maintenance with a reduced workforce.

The production halt comes after a sharp run up, with Nexa Resources posting a 38.31% 30 day share price return and a 117.11% 90 day share price return, while its 1 year total shareholder return of 88.14% points to strong momentum that recent short term volatility has not fully reversed.

If this kind of event risk has you thinking about diversification, it could be a suitable time to broaden your watchlist and check out fast growing stocks with high insider ownership.

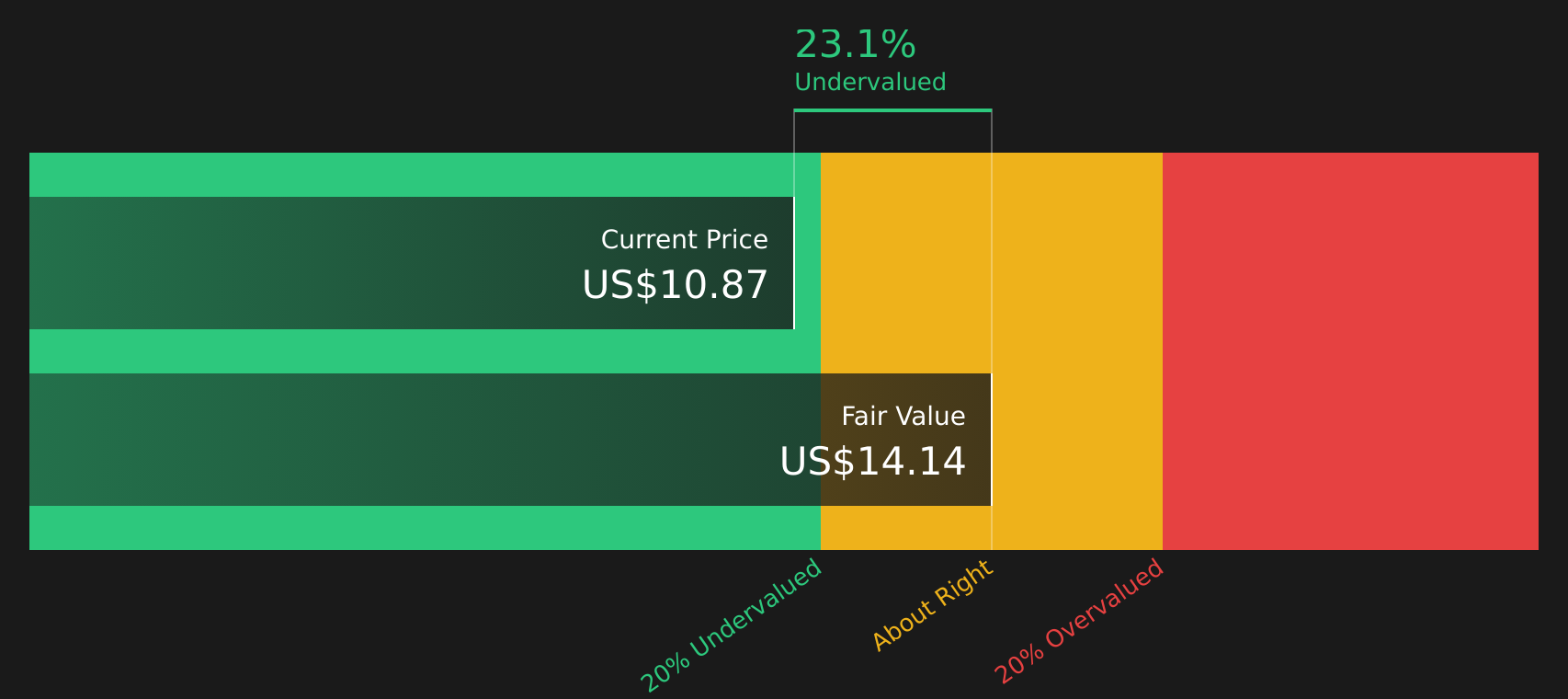

With Nexa trading at $12.31, which is above an average analyst price target of $7.40 yet still shows a 54.13% intrinsic discount, you have to ask whether the recent optimism is justified or whether the market is already pricing in future growth.

Most Popular Narrative: 75.2% Overvalued

Compared with the last close of $12.31, the most followed narrative points to a fair value of about $7.03, which is a steep gap for any investor to ignore.

The plan to reach Aripuana’s nameplate capacity only in the second half of 2026, with the fourth tailings filter still in installation and commissioning, concentrates a lot of future zinc volume and cash flow in a single asset. Any delay or underperformance could weigh on revenue growth and EBITDA.

Curious what kind of margin lift and earnings swing this story is built on, and what profit multiple is baked into that fair value? The narrative leans heavily on a turnaround from losses to consistent profits, relatively stable revenue expectations and a lower earnings multiple than many peers. If you want to see exactly how those moving parts stack up to reach $7.03, the full narrative lays out the math in detail.

Result: Fair Value of $7.03 (OVERVALUED)

However, if zinc, copper and silver prices stay constructive and Aripuana ramps as planned, stronger cash generation could quickly challenge the current overvaluation story.

Another View: Cash Flows Tell a Different Story

While the consensus narrative points to Nexa Resources looking expensive versus a fair value of about $7.03, our DCF model lands in a very different place, with an estimated future cash flow value of $26.84 per share, which is well above the current $12.31 price. When earnings based targets and cash flow based estimates are this far apart, which lens do you trust more for a long term call?

Build Your Own Nexa Resources Narrative

If you look at the numbers and reach a different conclusion, or simply prefer to test your own view against the data, you can build a personalised thesis in just a few minutes with Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Nexa Resources.

Ready to hunt for your next idea?

If Nexa has your attention, do not stop here. Put the same energy into a few fresh stock ideas that could reshape how you build your portfolio.

- Spot potential value gaps by scanning these 880 undervalued stocks based on cash flows that line up with your return and risk expectations.

- Lean into future themes by checking out these 24 AI penny stocks that are building real businesses around artificial intelligence.

- Add income angles by reviewing these 12 dividend stocks with yields > 3% that focus on established payouts above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.