A Look At Norfolk Southern (NSC) Valuation After The Gainesville Inland Port Launch

Norfolk Southern Corporation NSC | 0.00 |

The opening of the Gainesville Inland Port, with direct rail service from Norfolk Southern (NSC) five days a week, is drawing new attention to how this freight corridor could affect the stock.

The recent opening of the Gainesville Inland Port and Norfolk Southern's upcoming appearance at the Bank of America Industrials, Transportation & Airlines conference come against a backdrop of a 30 day share price return of 8.63% and a 1 year total shareholder return of 42.46%. This suggests momentum has been building after a softer 7 day share price move.

If you are looking beyond a single freight stock and want to see what else is gaining attention in critical infrastructure, it may be worth checking out 36 power grid technology and infrastructure stocks

With Norfolk Southern showing a 1 year total shareholder return of 42.46% and trading about 6.9% below the average analyst price target, it raises the question: is there still value here, or is the market already pricing in future growth?

Most Popular Narrative: 5.7% Undervalued

Norfolk Southern's most followed narrative pegs fair value at about $332 per share, a touch above the last close of $313.39, and frames that gap around long term rail efficiency and infrastructure demand.

The company's focus on increasing customer confidence through consistent service improvements is leading to meaningful market share gains, particularly in merchandise and intermodal segments, which could bolster future revenue growth.

Want to see what sits behind that confidence in higher earnings and margins? The narrative leans on a specific mix of revenue growth, profitability gains and a richer future earnings multiple that is usually reserved for faster growing sectors. Curious which financial levers matter most for that fair value gap?

Result: Fair Value of $332 (UNDERVALUED)

However, those higher earnings and margin assumptions can be tested quickly if storm related costs climb again or if weaker export coal pricing weighs on revenue and profitability.

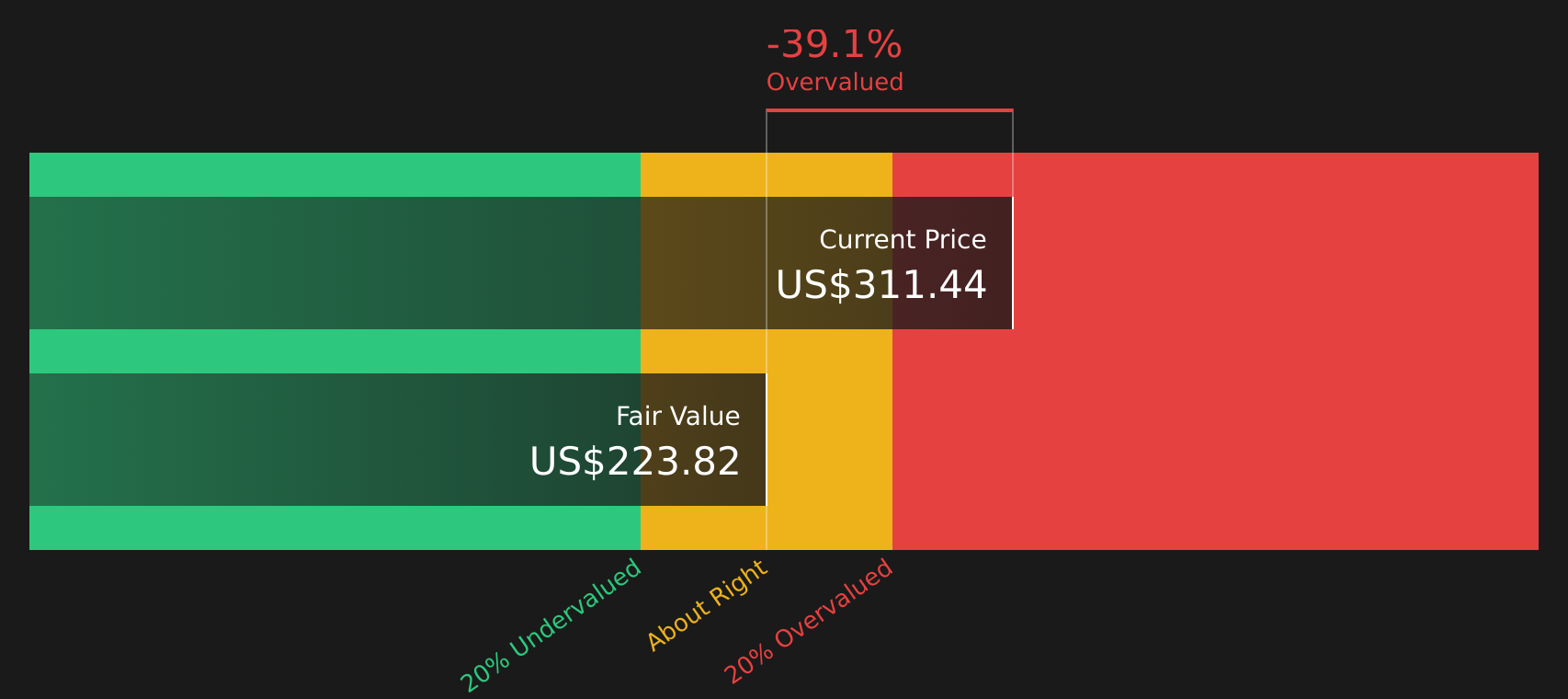

Another Angle: DCF Comes Out More Cautious

The popular narrative suggests Norfolk Southern is about 5.7% undervalued at $332 per share. However, our DCF model indicates a future cash flow value of $224.95, with the stock trading above that level. So which story do you trust more: earnings power or cash flows?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Norfolk Southern for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 51 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With mixed signals across valuation models and sentiment, this is a good time to look under the hood yourself and move quickly to firm up your own view. You might start with the 3 key rewards and 1 important warning sign.

Looking for more investment ideas?

If you stop with just one stock, you could miss opportunities sitting in plain sight, so use the screener to widen your search and stress test your thinking.

- Target quality at a discount by running your filters through 51 high quality undervalued stocks and see which stocks match your price and fundamentals criteria.

- Prioritise resilience by scanning for companies in 72 resilient stocks with low risk scores that align with your comfort level around volatility and business risk.

- Spot potential future standouts before the crowd by checking the screener containing 23 high quality undiscovered gems for lesser known stocks with solid fundamentals.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.