A Look At Norfolk Southern (NSC) Valuation After The Jaguar Freight Partnership Announcement

Norfolk Southern Corporation NSC | 296.29 296.29 | +0.34% 0.00% Pre |

Why the Jaguar partnership matters for Norfolk Southern stock

Norfolk Southern (NSC) is back in focus after announcing a partnership with Jaguar Transport Holdings to handle local switching, run its Doraville transload terminal, and invest in added freight capacity in northeast Atlanta.

The agreement centers on first and final mile service, with Jaguar expected to upgrade infrastructure at Doraville to support new freight volumes, increased transloading capacity, and smoother connections for both rail-served and truck-to-rail customers.

The Jaguar announcement comes after a period where NSC’s share price return has been mixed in the short term, with a 7 day share price return of 2.53% and a 1 year total shareholder return of 39.85%, suggesting momentum has been building over a longer horizon.

If this kind of rail partnership has caught your attention, it could be a good moment to see what other infrastructure linked names are doing and check out 30 power grid technology and infrastructure stocks

With Norfolk Southern trading at $295.30, annual revenue of about $12.18b, net income of roughly $2.87b, and mixed short term returns, is the current price a fair reflection of the company’s prospects or is the market offering an opportunity?

Most Popular Narrative: 5.5% Undervalued

Against the last close of $295.30, the most followed narrative places Norfolk Southern’s fair value at about $312.63, framing the Jaguar deal within a broader efficiency and earnings story.

The commitment to $150 million in productivity and cost reduction initiatives over three years is being propelled by better labor productivity and fuel efficiency, which are anticipated to sustain EPS growth even if revenue growth slows.

The company's focus on increasing customer confidence through consistent service improvements is leading to meaningful market share gains, particularly in merchandise and intermodal segments, which could support future revenue growth.

Want to see what sits behind that fair value gap? The narrative leans on measured revenue growth, firmer margins, and a future earnings profile that assumes investors keep paying up for this network.

Result: Fair Value of $312.63 (UNDERVALUED)

However, you still need to weigh risks such as higher storm restoration costs and softer coal or intermodal pricing, which could pressure revenue, expenses and margins.

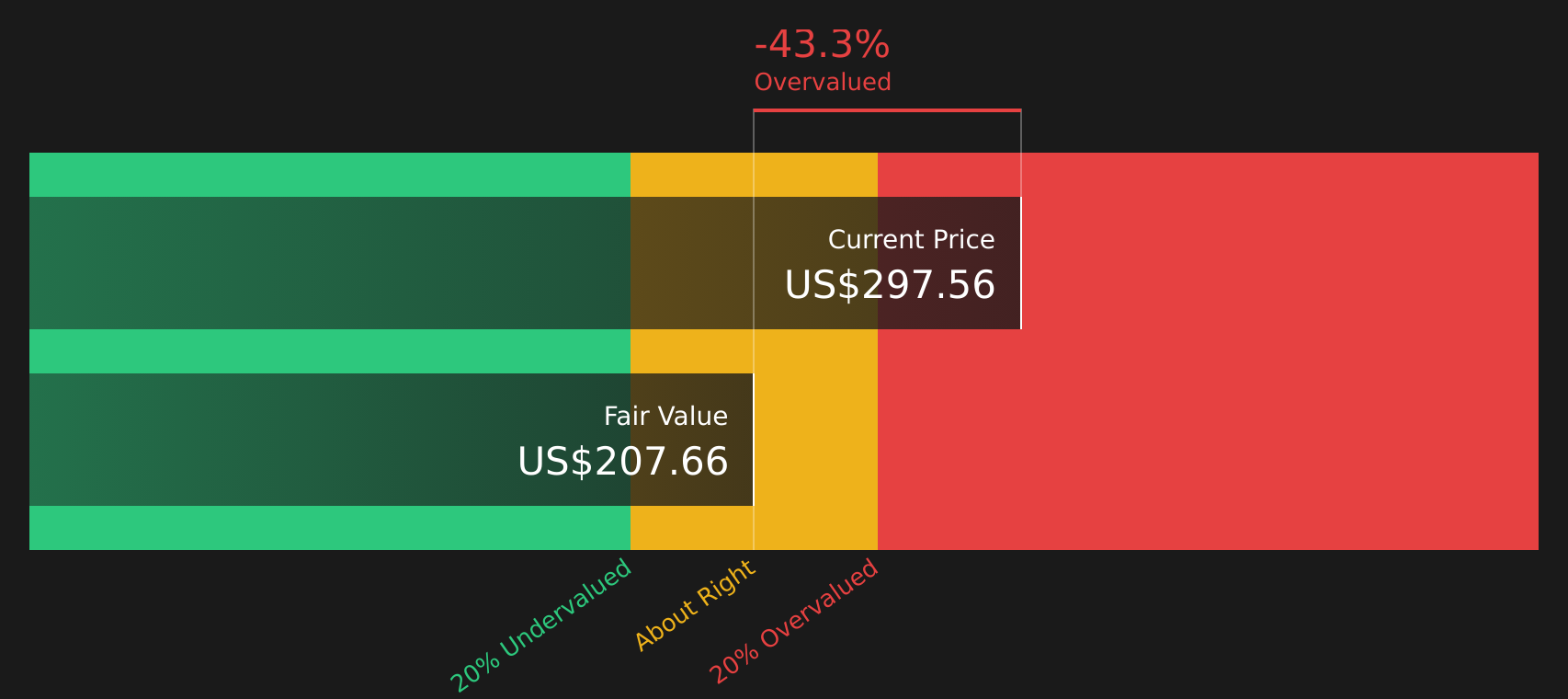

Another Angle on Value: Cash Flows vs Narratives

Analysts see a fair value near $312.63, yet the Simply Wall St DCF model points to a future cash flow value of about $207.32, with NSC trading at $295.30. One approach frames NSC as 5.5% undervalued, while the other suggests it is clearly overvalued. Consider which perspective better fits how you think about risk.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Norfolk Southern for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 62 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If the mix of optimism and concern in this story feels familiar, consider this a prompt to review the numbers directly and pressure test the assumptions using 4 key rewards and 1 important warning sign

Ready for more investment ideas?

Do not stop with a single stock story. Broaden your watchlist with a few focused sets of ideas that align with how you like to invest.

- Target dependable cash generators by scanning solid balance sheet and fundamentals stocks screener (40 results) that can better handle shocks and still fund growth.

- Hunt for mispriced opportunities and compare Norfolk Southern with 62 high quality undervalued stocks that pair strong fundamentals with attractive valuations.

- Spot under the radar opportunities before they hit the mainstream by checking the screener containing 24 high quality undiscovered gems and see which names deserve a closer look.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.