A Look At NovoCure (NVCR) Valuation After Record 2025 Revenue And CEO Transition

NovoCure Ltd. NVCR | 10.55 | -2.68% |

NovoCure (NVCR) has drawn fresh attention after reporting record 2025 revenues of $655 million, appointing Frank Leonard as CEO, and advancing FDA submissions for its tumor treating fields therapies.

Those record 2025 revenues and the new CEO appointment come after a mixed year in the market, with a 30 day share price return of 6.17% and a 1 year total shareholder return decline of 47.74%. This suggests long term investors are still reassessing risk even as shorter term momentum shows signs of stabilisation.

If NovoCure’s cancer focused pipeline has your attention, it could be a good moment to scan other ideas across healthcare stocks as you compare potential opportunities.

With record 2025 revenue of $655 million, a new CEO and key FDA decisions ahead, NVCR’s share price still sits far below its 1 year level. Is the stock undervalued here, or is the market already pricing in future growth?

Most Popular Narrative: 44.8% Undervalued

Compared to NovoCure’s last close of US$13.77, the most followed narrative points to a fair value close to US$24.93, which implies a significant gap between the current share price and that estimate.

Validation of TTFields therapy in multiple new indications, such as pancreatic cancer (PANOVA-3) and brain metastases from non-small cell lung cancer (METIS), positions NovoCure for potential regulatory approvals and large market expansion beginning in 2026, likely driving topline revenue growth as global cancer incidence rises in the aging population.

Analysts are tying this valuation to a focused set of assumptions around future revenue, a shift from losses to stronger margins, and a premium P/E multiple. Curious which moving part matters most for that fair value estimate?

Result: Fair Value of $24.93 (UNDERVALUED)

However, slower than expected prescription growth and ongoing reimbursement uncertainty could limit adoption and keep losses and valuation assumptions under pressure.

Another View on Valuation

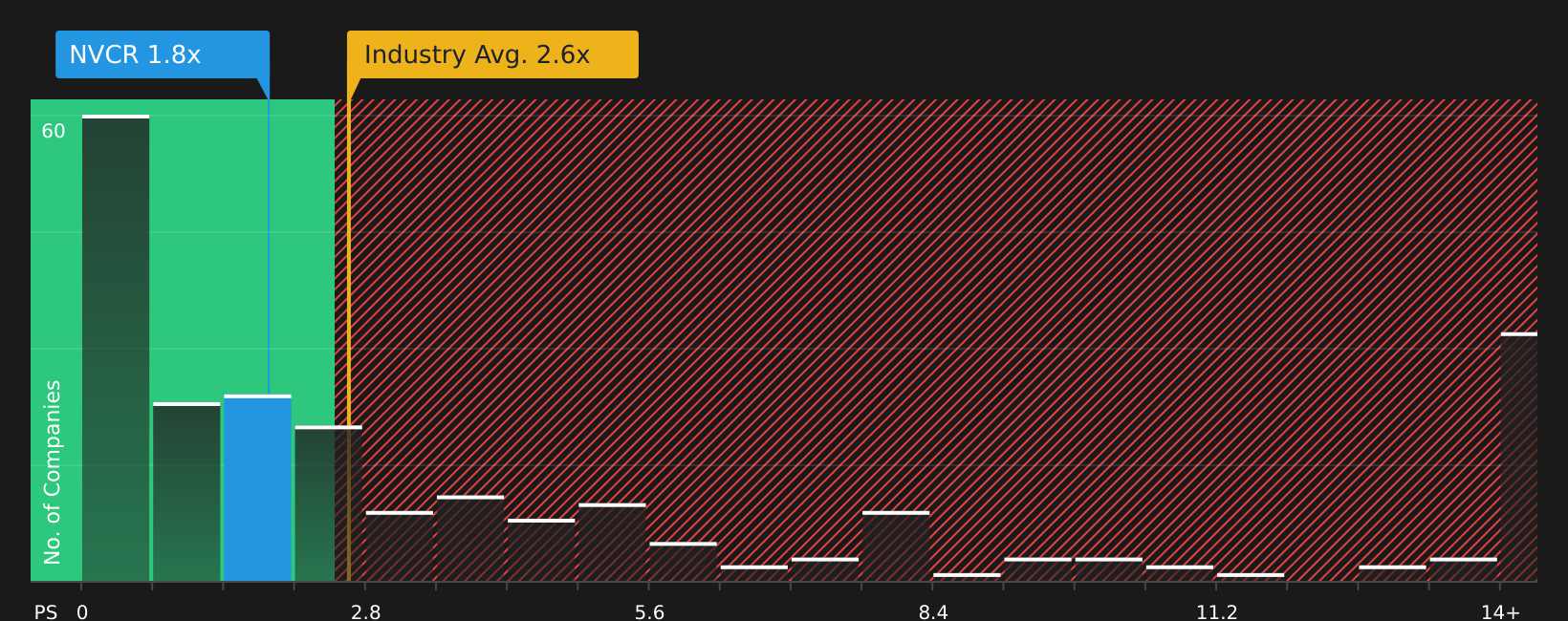

Those fair value estimates in the mid US$20s lean heavily on future earnings and margins. If you look at today’s pricing through revenue instead, NovoCure trades on a P/S ratio of 2.4x, roughly in line with peers at 2.4x and below its 4x fair ratio. The question is whether the risk is skewed toward a re-rating or further doubt.

Build Your Own NovoCure Narrative

If you see the story differently, or prefer to weigh the numbers yourself, you can build a full NovoCure view in minutes with Do it your way.

A great starting point for your NovoCure research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Ready for more investing ideas?

If NovoCure is on your radar, do not stop here. A few minutes with the right screeners can surface opportunities you might otherwise miss.

- Target higher potential upside by scanning these 3535 penny stocks with strong financials that pair smaller market caps with stronger financial profiles than you might expect.

- Get ahead of emerging trends by focusing on these 25 AI penny stocks that link artificial intelligence themes with early stage growth stories.

- Zero in on price versus fundamentals by reviewing these 886 undervalued stocks based on cash flows built around discounted cash flow assessments and cash flow strength.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.