A Look At NovoCure (NVCR) Valuation As Shares Show Mixed Recent Performance

NovoCure Ltd. NVCR | 0.00 |

Event context and recent price performance

NovoCure (NVCR) stock has drawn investor attention after recent trading left the shares at a last close of US$16.56, with the move coming alongside mixed short term and longer term return patterns.

The stock declined 2.8% over the past day and 7.8% over the past week, was broadly flat over the past month, and is up about 24.5% over the past 3 months and 26.2% year to date.

Looking beyond the latest pullback, NovoCure’s recent 3 month share price return in the mid 20% range contrasts with a 1 year total shareholder return that is slightly negative. This points to recovering momentum after a much weaker multi year period.

If you are watching how sentiment shifts around healthcare and cancer treatment companies, this could be a good moment to broaden your watchlist and scan 40 healthcare AI stocks

With NovoCure generating US$674.4 million in revenue but still reporting a US$173.0 million loss, and trading well below some analyst price targets, investors may need to consider whether this is a mispriced recovery story or whether markets have already factored in the expected future growth.

Most Popular Narrative: 36.5% Undervalued

At a last close of $16.56 versus a narrative fair value of $26.07, NovoCure is framed as materially undervalued, with that gap tied to specific growth and margin assumptions.

Validation of TTFields therapy in multiple new indications, such as pancreatic cancer (PANOVA-3) and brain metastases from non-small cell lung cancer (METIS), positions NovoCure for potential regulatory approvals and large market expansion beginning in 2026, with the possibility of topline revenue growth as global cancer incidence rises in the aging population.

Increasing real-world adoption of TTFields in both academic and community settings, supported by positive retrospective studies (e.g., Mayo Clinic data in GBM), indicates building physician confidence and integration into standard care, which may translate into higher device utilization rates and more stable recurring revenues over time.

Want to see what sits behind that fair value gap? The narrative leans on steady revenue compounding, margin repair, and a higher future earnings multiple that has to hold.

Result: Fair Value of $26.07 (UNDERVALUED)

However, the story can change quickly if TTFields adoption stalls or reimbursement progress slows, which could pressure growth expectations and keep losses elevated.

Another angle on valuation

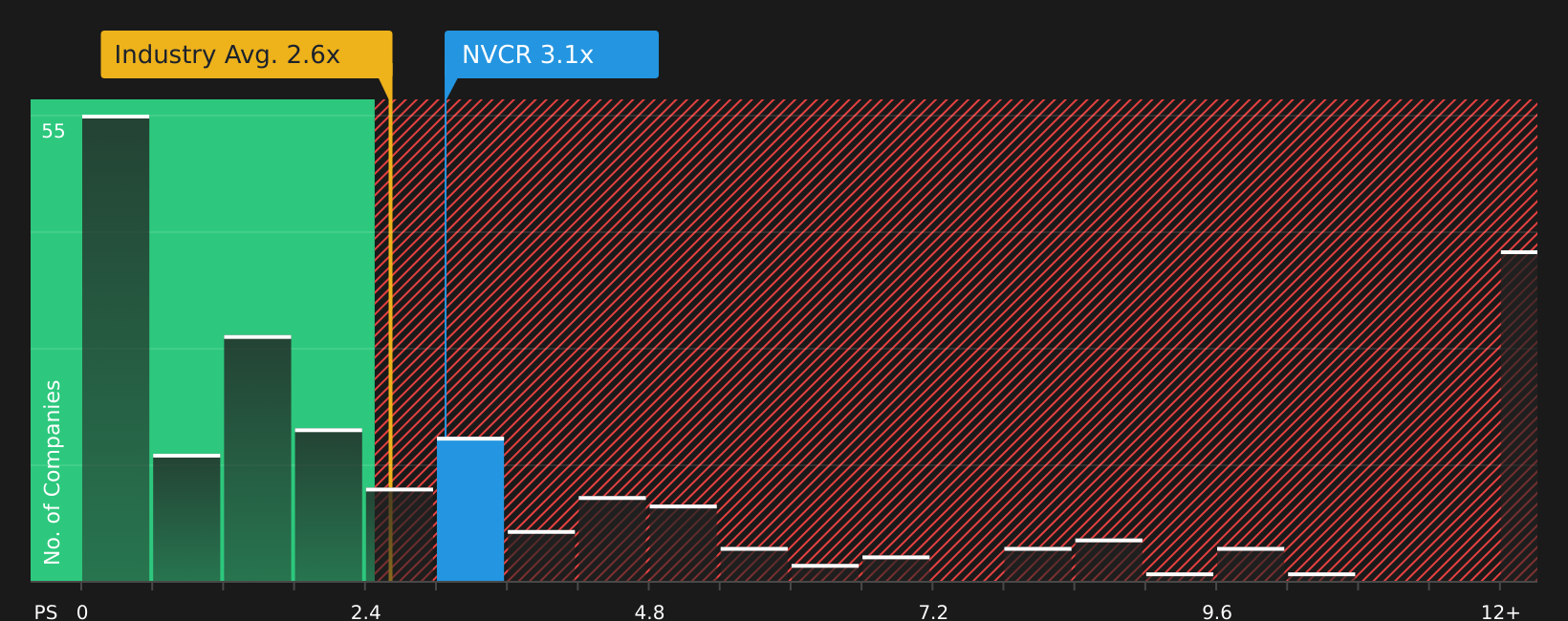

While the narrative fair value of $26.07 frames NovoCure as undervalued, the price to sales picture is more cautious. At 2.8x P/S, the stock sits in line with the US Medical Equipment average of 2.8x, but below a fair ratio estimate of 4.8x and a peer average of 5.2x. That mix of apparent upside and sector level parity leaves an open question: is this a margin of safety or a value trap waiting for better execution?

Next Steps

With mixed signals on valuation, risk, and potential rewards, do not wait for consensus. Check the data yourself and weigh the 2 key rewards and 1 important warning sign

Looking for more investment ideas?

If you stop with just one stock, you could miss out on opportunities that fit your goals even better, so use the tools available and keep your options open.

- Target higher potential with quality at the core by scanning screener containing 22 high quality undiscovered gems that combine solid fundamentals with room to grow.

- Strengthen your income stream by reviewing 10 dividend fortresses that focus on companies offering substantial yields with an eye on stability.

- Dial down portfolio stress by filtering for 62 resilient stocks with low risk scores that prioritize resilience and more measured risk profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.