A Look at On Running (ONON) Valuation Following Latest Financial Results

On Holding AG Class A ONON | 33.57 | -3.44% |

On Holding (NYSE:ONON) has delivered its latest financial results, drawing attention to both revenue growth and profitability. Investors will likely focus on how these numbers reflect the company's performance in comparison to market expectations and past figures.

After an impressive run since its IPO, On Holding’s 3-year total shareholder return still sits at a remarkable 160%, despite a bumpy ride lately. Momentum has clearly faded this year, with the share price down 22% year-to-date. This suggests investors are weighing both growth prospects and rising risks in the current environment.

If you’re looking for your next big opportunity, this could be the perfect moment to broaden your search and discover fast growing stocks with high insider ownership

With shares trading about 46% below the average analyst price target and fundamentals showing solid growth, investors may wonder if On Holding is undervalued at current levels or if the market has already priced in the company's forward momentum.

Most Popular Narrative: 34.9% Undervalued

Compared to its last close at $42.97, On Holding's most widely followed narrative puts fair value well above the current price, hinting at significant room for upside if expected growth is realized.

The acceleration in DTC (Direct-to-Consumer) and e-commerce channels, with DTC reaching new highs (41.1% of sales in Q2 and up 54% YoY), gives On more control over brand, pricing, and customer data. This also increases gross and EBITDA margins, serving as an operational catalyst likely to further expand profitability as DTC continues its mix shift.

Want the secret to this bullish valuation? A big part of the story relies on aggressive top-line expansion, bolder margin targets, and an ambitious profit transformation. Curious what rates and future multiples drive the narrative's price target without seeing the actual math? Click for the inside story.

Result: Fair Value of $66.04 (UNDERVALUED)

However, risks remain. As competition intensifies and On Holding's heavy reliance on premium pricing may limit its ability to maintain current growth rates.

Another View: Multiples Paint a Cautious Picture

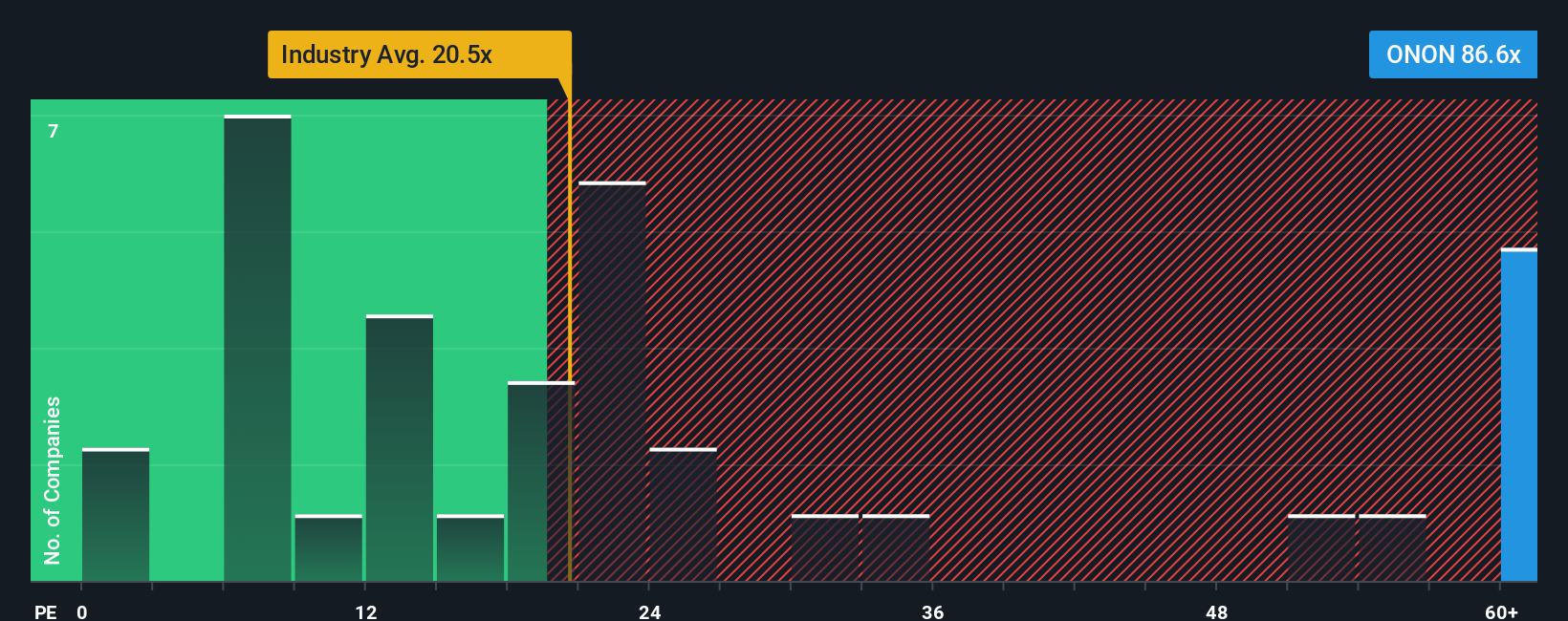

While optimistic forecasts highlight big upside, the company trades at a steep price-to-earnings ratio of 83 times, much higher than both industry peers (around 21 times) and its own fair ratio of 32.9. This premium leaves little room for disappointment or missteps, which could be a warning sign for value-focused investors.

Build Your Own On Holding Narrative

If you like to form your own views or dive deeper into the numbers, you have all the tools needed to craft a narrative in just a few minutes, so why not Do it your way

A great starting point for your On Holding research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Investment Ideas?

Don’t stop at just one stock when there’s a world of opportunity out there. Take charge and discover powerful new ways to grow your portfolio today.

- Tap into the next innovation wave by checking out these 25 AI penny stocks powering breakthroughs in artificial intelligence and automation.

- Supercharge your search for market bargains with these 891 undervalued stocks based on cash flows holding real promise based on underlying cash flows.

- Secure steady income for your future. See these 18 dividend stocks with yields > 3% that deliver attractive yields and consistent performance.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.