A Look At ON Semiconductor (ON) Valuation As Analyst Optimism And Earnings Anticipation Build

ON Semiconductor Corporation ON | 0.00 |

What is driving renewed attention on ON Semiconductor?

ON Semiconductor (ON) is attracting fresh attention after recent reports highlighted analyst optimism, reflected in a favorable Zacks Rank of #2 and supported by upward revisions to earnings estimates.

Investor focus has also picked up ahead of the company’s upcoming earnings report on May 4, 2026, as many market participants watch how those updated expectations line up with ON’s actual results.

ON’s recent momentum has been strong, with a 48.59% 1 month share price return and a 56.95% year to date share price return, alongside a 143.01% 1 year total shareholder return, as investors respond to earnings optimism and the upcoming report.

If you are looking beyond ON for other chip related ideas benefiting from similar themes around data centers and electrification, now could be a good time to scan 38 AI infrastructure stocks

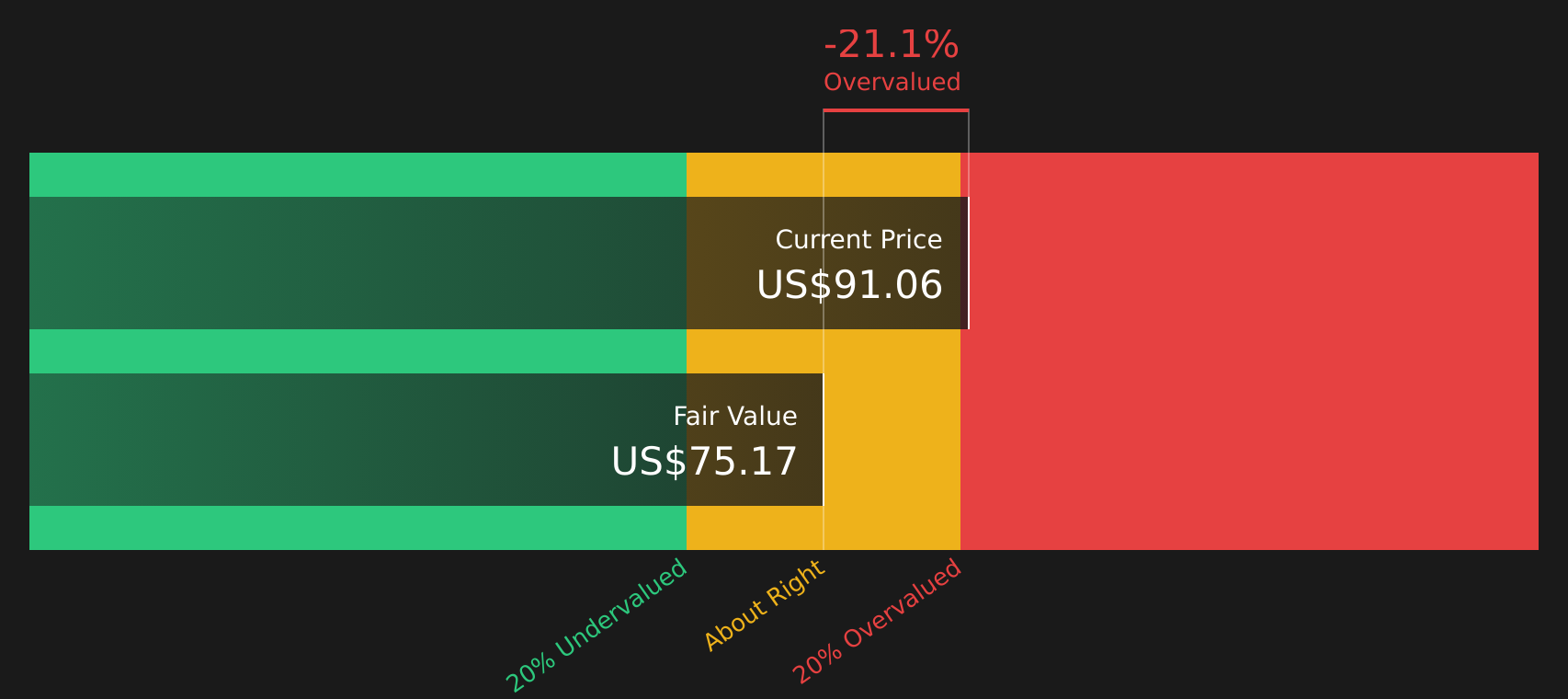

With ON now trading around $88.99, above an average analyst target of about $70.79 and with recent returns already strong, investors may need to consider whether there is real value left or whether the market is already pricing in future growth.

Most Popular Narrative: 30.3% Overvalued

ON Semiconductor’s most followed narrative sets fair value at about $68.28, well below the current $88.99 share price. This frames a clear valuation gap for investors to interrogate.

Ongoing portfolio rationalization, phasing out legacy and non-core products, and reallocating resources towards higher-margin, differentiated offerings (such as ADAS image sensing and machine vision), should improve product mix and boost average margins, positively impacting net profitability and earnings leverage.

Structural improvements in manufacturing efficiency, including the Fab Right initiative and selective capacity reduction, are lowering operational costs and setting up significant margin expansion as utilization rates recover with end-market demand. This operational leverage is likely to drive higher net margins and cash flow conversion as the cycle turns.

Curious how margin expansion, earnings forecasts and the assumed discount rate combine to support that fair value? The narrative leans heavily on future profitability, efficiency gains and capital returns. Want to see exactly which earnings profile and terminal multiple are baked into that $68 range and how much of today’s price depends on everything going right?

Result: Fair Value of $68.28 (OVERVALUED)

However, that story can change quickly if EV demand outside China stays soft, or if underused factories keep margins under pressure longer than analysts currently assume.

Another angle on ON’s price

Our DCF model points to a value of about $69.14 per share, compared with the current $88.99 price. That also suggests ON looks overvalued, even before layering in all the narrative assumptions around margins and growth. So what needs to happen for today’s price to hold up?

Next Steps

Seen enough differing views to feel a bit torn about ON’s outlook? Act now by reviewing both sides of the story through 1 key reward and 3 important warning signs

Looking for more investment ideas?

If ON has piqued your interest, do not stop here. Broaden your watchlist with other angles on quality, value and resilience that could complement your portfolio.

- Target potential mispricings by scanning 61 high quality undervalued stocks that combine solid fundamentals with room for the market to reassess their worth.

- Strengthen your income focus by reviewing 13 dividend fortresses that aim to pair higher yields with durable underlying businesses.

- Prioritise capital preservation by assessing 73 resilient stocks with low risk scores that score well on financial stability and risk controls.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.