A Look at OneStream’s Valuation Following Microsoft Partnership and Expanded Enterprise AI Ambitions

OneStream OS | 0.00 |

OneStream (OS) announced a strategic alliance with Microsoft during Microsoft Ignite 2025. This partnership brings its SensibleAI Agent technology to Microsoft 365 and Azure. The collaboration is designed to accelerate AI adoption in enterprise finance.

After announcing this deepened partnership with Microsoft, OneStream’s stock has shown signs of renewed interest, notching a strong 14.6% share price return over the past month as excitement builds around its expanded role in enterprise AI. Despite this recent upside, momentum has yet to offset the longer-term dip. The one-year total shareholder return is -30.3%, reflecting a market still calibrating the company’s future potential as it forges new tech alliances.

If you’re curious about what else is happening in the world of software and AI, now’s an opportune moment to explore and discover See the full list for free.

With the recent surge in share price but lingering long-term losses, the key question for investors is whether OneStream remains undervalued given its fresh Microsoft alliance, or if the market has already accounted for its future growth prospects.

Most Popular Narrative: 26% Undervalued

With OneStream's current price significantly below the narrative’s $28.26 fair value estimate, investors are watching to see whether momentum can sustain a long-term turnaround. The narrative’s discount rate of 8.40% provides a framework for ambitious assumptions on growth and profitability.

“Ongoing large-scale digital transformation across industries, with CFOs increasingly seeking unified platforms to replace legacy financial systems, strongly positions OneStream to capture expanding market share, supporting sustained subscription revenue and new customer growth.”

Want to know what ambitious projections put this valuation within reach? The narrative relies on rapid digital adoption, recurring revenue, and a major shift in enterprise finance. But which specific assumptions drive this bullish outlook? Dive in to uncover the financial catalysts and disruptive growth bets that fuel this compelling case.

Result: Fair Value of $28.26 (UNDERVALUED)

However, ongoing public sector uncertainty and slower SaaS migration could weigh on revenue growth. This may present challenges to the optimistic outlook surrounding OneStream’s future performance.

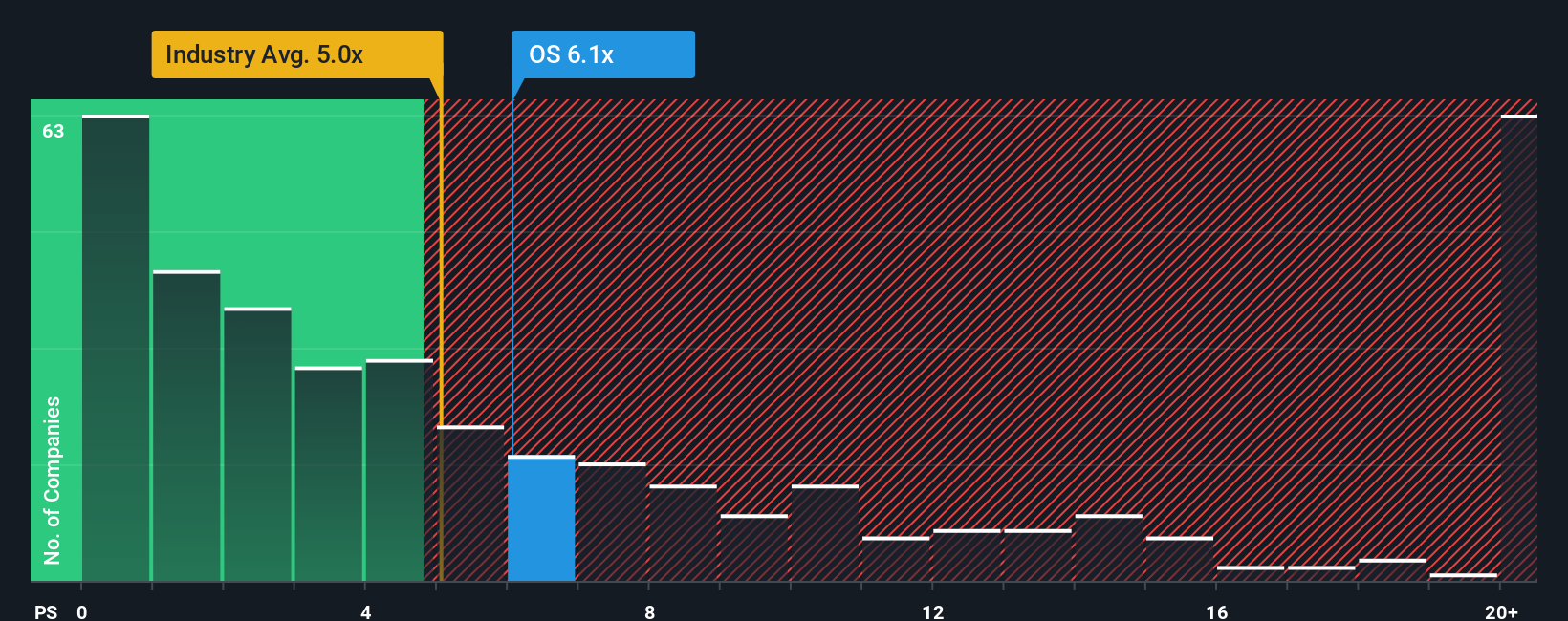

Another View: What Does the Sales Multiple Say?

Looking through another lens, OneStream is trading at a price-to-sales ratio of 6.9x. This is higher than the US Software industry average of 4.7x, but still below the peer group, which sits at 8.2x. The fair ratio, where the market might eventually settle, is 6.3x. Is this a sign of upside, or does it hint at valuation risk that could keep shares grounded?

Build Your Own OneStream Narrative

If you see things differently or want to analyze the numbers firsthand, you can shape your own take on OneStream’s outlook in just a few minutes. Do it your way

A great starting point for your OneStream research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Smart Investment Ideas?

Unlock more sharp opportunities by checking out unique screeners that highlight breakthrough companies, attractive valuations, and emerging trends before they become mainstream. Don’t let these promising ideas pass you by.

- Tap into fast-growing technology picks and see which trailblazers top the charts with these 25 AI penny stocks.

- Spot undervalued gems poised for a turnaround by using these 920 undervalued stocks based on cash flows to boost your portfolio’s upside potential.

- Start building regular income streams by investing in steady performers through these 15 dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.