A Look At Otter Tail (OTTR) Valuation After PVC Pipe Antitrust Settlement Agreements

Otter Tail OTTR | 0.00 |

Otter Tail (OTTR) is back on investor radar after the company agreed to pay a combined US$73.5 million to settle two plaintiff classes in ongoing PVC pipe antitrust litigation, subject to court approval.

The legal update lands at a time when the stock has been giving back some recent gains, with the 30-day share price return down 5.49%, even as the year-to-date share price return of 5.34% and 1-year total shareholder return of 13.53% point to solid longer term momentum.

If this legal settlement has you reassessing utilities and infrastructure style plays, it can be useful to widen your scope and review 33 power grid technology and infrastructure stocks

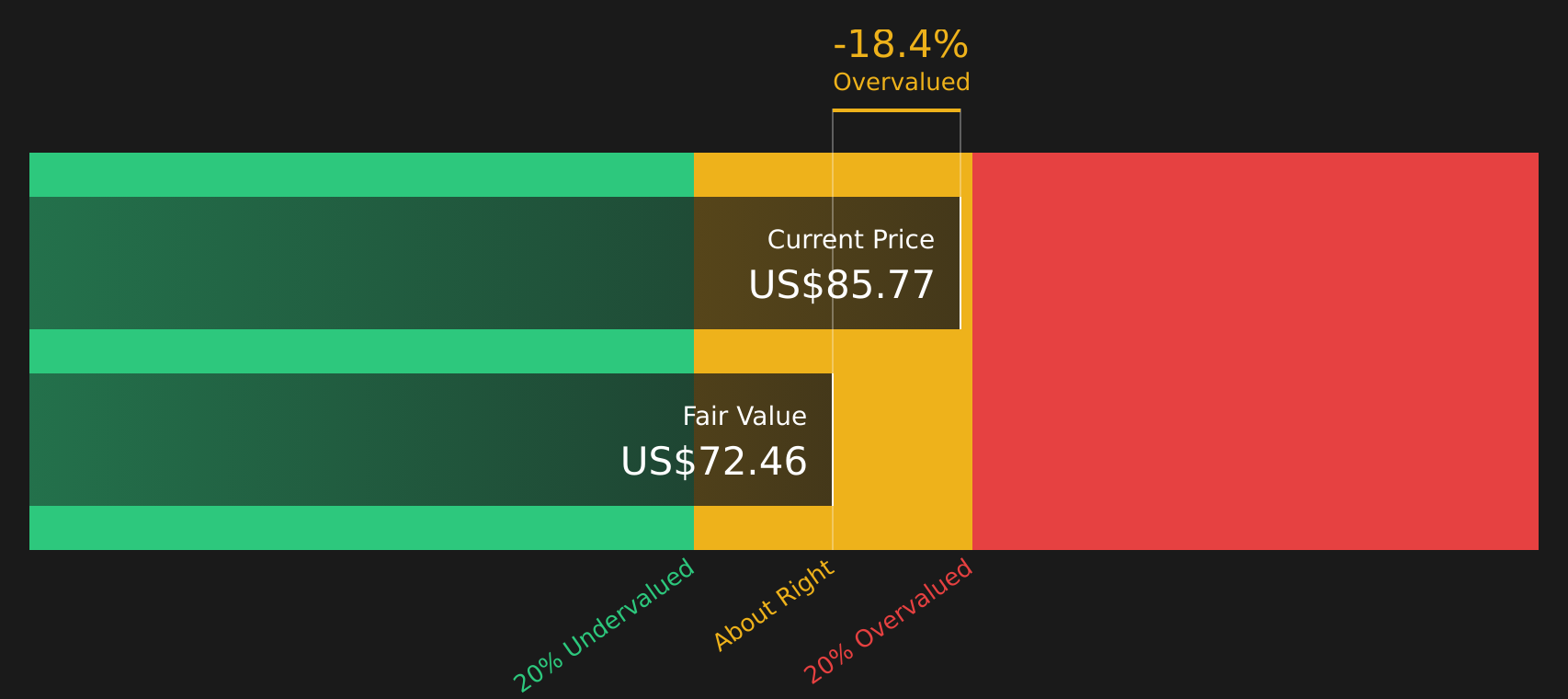

With Otter Tail trading around US$85.80, sitting roughly 5% below the average analyst target and at an estimated premium to some intrinsic value models, should you see this pullback as a buying window or accept that markets are already pricing in future growth?

Most Popular Narrative: 5.2% Undervalued

Otter Tail's most followed narrative pegs fair value at $90.50, a premium to the last close at $85.80, and builds a case around earnings visibility and capital plans.

The analysts have a consensus price target of $90.5 for Otter Tail based on their expectations of its future earnings growth, profit margins and other risk factors.

In order for you to agree with the analysts, you would need to believe that by 2029, revenues will be $1.4 billion, earnings will come to $205.5 million, and it would be trading on a PE ratio of 22.8x, assuming you use a discount rate of 7.1%.

Want to see what underpins that premium fair value? The narrative leans heavily on cash flow resilience, margin compression, and a richer future earnings multiple. Curious which assumptions really carry the model.

Result: Fair Value of $90.50 (UNDERVALUED)

However, this depends on execution, as tighter environmental rules around coal assets and higher financing costs on the US$1.4b capital plan are both capable of reshaping the story.

Another View: Cash Flows Paint a Tougher Picture

While the analyst narrative sees Otter Tail as 5.2% undervalued at a fair value of $90.50, our DCF model is more cautious. It indicates the stock at $85.80 is trading above an estimated future cash flow value of $72.46. That gap suggests less room for error if growth underwhelms.

For a closer look at how this cash flow view is built, and how sensitive it is to small shifts in earnings or discount rates, Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Otter Tail for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 47 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With both risks and rewards in play, do you feel the balance of this story fits your own expectations, or is it time to pressure test the thesis and move quickly using 2 key rewards and 3 important warning signs?

Looking for more investment ideas?

Do not stop at one stock. Broaden your watchlist with data driven ideas so you are not relying on a single narrative when the next move comes.

- Tap into potential mispricing by checking companies that screen as quality and undervalued through the 47 high quality undervalued stocks.

- Focus on dependable income by reviewing companies with stronger yields and solid payout profiles in the 11 dividend fortresses.

- Prioritize resilience by scanning companies with sturdier balance sheets and fundamentals using the solid balance sheet and fundamentals stocks screener (47 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.