A Look At Packaging Corporation Of America (PKG) Valuation After Recent Share Price Strength

Packaging Corporation of America PKG | 204.46 | -3.22% |

Why Packaging Corporation of America is on investors’ radar

Packaging Corporation of America (PKG) has drawn fresh attention after recent share moves, with the stock closing at $223.72 and showing positive returns over the past month and past 3 months.

For investors tracking established US industrials, the company’s mix of containerboard and paper operations, combined with its recent performance profile, raises practical questions about valuation, earnings power and where PKG might fit in a diversified portfolio.

PKG’s recent 30-day share price return of 5.97% and 90-day share price return of 13.47%, alongside a 1-year total shareholder return of 8.56% and 5-year total shareholder return of 95.22%, indicate that momentum has been stronger over the longer term than in the very short term, as investors weigh the company’s earnings profile and containerboard demand trends against its current share price near $223.72.

If PKG’s move has you thinking about what else might be setting up for the next leg higher, this could be a good moment to scan fast growing stocks with high insider ownership.

With PKG trading near $223.72, sitting only slightly below an average analyst price target of $230.40 and alongside an estimated 50% intrinsic discount, you have to ask: is this a genuine value gap, or is future growth already baked in?

Most Popular Narrative: 2.9% Undervalued

Packaging Corporation of America’s most widely followed narrative pegs fair value at $230.40, slightly above the recent $223.72 close, so the gap is small but visible.

The reconfigured Wallula mill setup is expected to reduce annual production capacity by 250,000 tons but lower production cost at the mill by about $125 per ton from 2025 levels. The reduced capacity is planned to be offset by production enhancements at other mills starting in the fourth quarter of 2026.

Cost cuts, mill closures, capacity shifts. The fair value hinges on how these changes reshape margins and earnings power. Curious which forecasts do the heavy lifting?

Result: Fair Value of $230.40 (UNDERVALUED)

However, if containerboard volumes or pricing soften, or if cost inflation and mill downtime run hotter than expected, that 2.9% undervaluation case could quickly look fragile.

Another way to look at PKG’s price

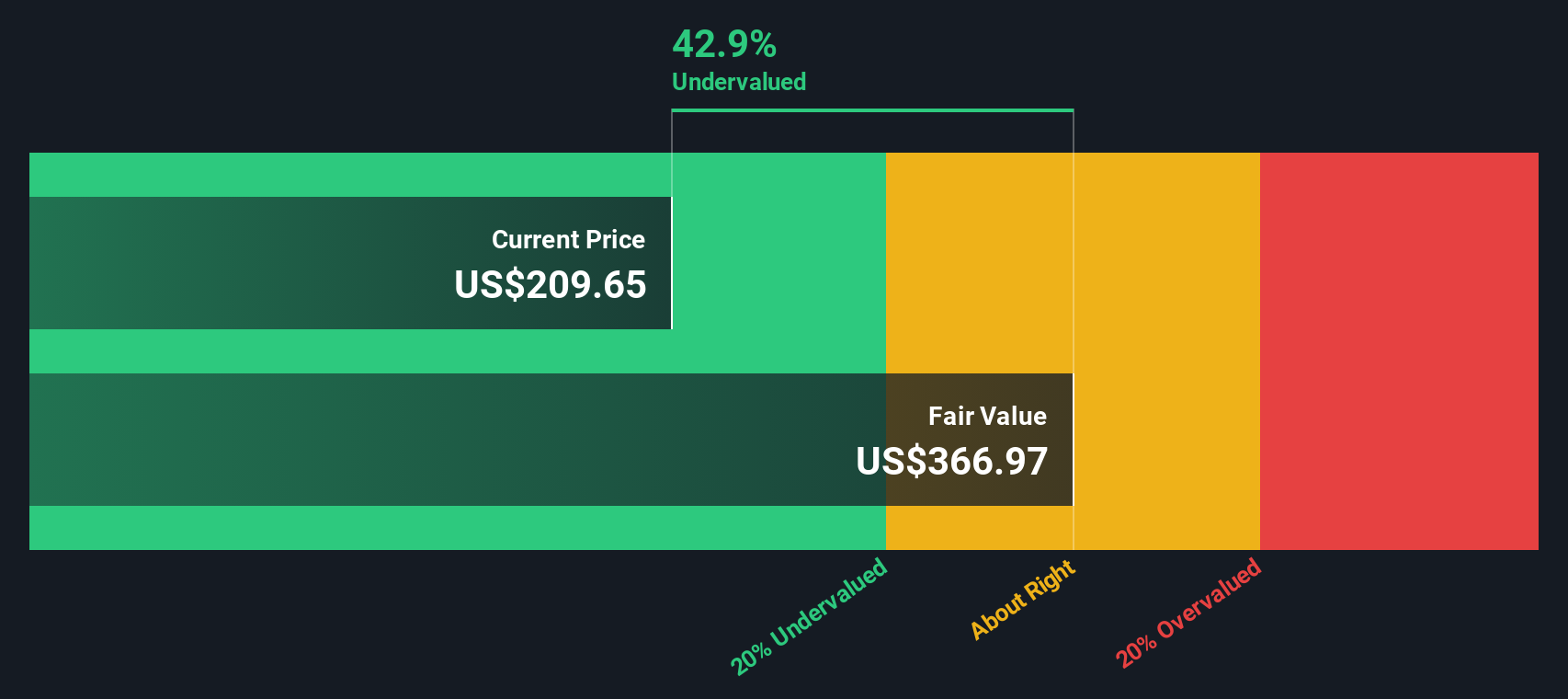

The SWS DCF model paints a very different picture, with an estimate of future cash flow value around $449.38 per share versus the current $223.72. That implies PKG is trading at roughly a 50.2% discount, which raises a simple question: is the cash flow story too generous or are expectations too low?

Build Your Own Packaging Corporation of America Narrative

If this perspective does not fully align with your own, or you would prefer to test your assumptions against the numbers directly, you can build a custom thesis in just a few minutes with Do it your way.

A great starting point for your Packaging Corporation of America research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If PKG caught your attention, do not stop here. Use the Simply Wall St Screener to quickly surface other stocks that might fit the kind of opportunities you are hunting.

- Spot potential value opportunities by scanning these 876 undervalued stocks based on cash flows that currently trade at a discount to their estimated cash flow potential.

- Tap into long term technology themes by checking out these 24 AI penny stocks tied to artificial intelligence across different parts of the market.

- Add extra yield to your watchlist by searching through these 13 dividend stocks with yields > 3% that offer dividend payouts above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.