A Look At Papa John’s (PZZA) Valuation After Its New Nationwide Pan Pizza Launch

Papa John's International, Inc. PZZA | 34.99 | +6.64% |

Papa John's International (PZZA) has rolled out a new nationwide pan pizza that is built around a six cheese blend and a texture-focused recipe, aiming to tap nostalgia and premium pizza demand.

The new pan pizza launch comes shortly after Papa John's affirmed a quarterly dividend of US$0.46 per share. The share price has a 30-day return of 13.95% and a 90-day return of 19.87%, contributing to a 1-year total shareholder return of 8.41% and a 5-year total shareholder return of 64.04%. This combination points to pressure on long term holders, even as shorter term momentum has recently been weak.

If this product refresh has you thinking about where growth stories might come from next, it could be worth scanning fast growing stocks with high insider ownership for ideas beyond the pizza sector.

With Papa John’s shares posting a 1-year total return of 8.41% and 5-year returns of 64.04%, and trading at a discount to analyst price targets, the key question is whether this pullback represents value for investors or if expectations for future growth are already reflected in the current price.

Most Popular Narrative: 28.2% Undervalued

With Papa John's International last closing at $34.31 against a narrative fair value of $47.80, the widely followed view sees considerable upside relative to current trading.

The review of the North American commissary and distribution network to improve supply chain efficiency is likely to enhance franchisee profitability and support net margins through cost savings.

Want to see what is behind that valuation gap? The narrative leans on modest revenue expectations, tighter margins and a richer future earnings multiple to bridge today’s price.

Result: Fair Value of $47.80 (UNDERVALUED)

However, recent global system wide sales softness and concerns about a possible quick service price war could both challenge the case for a higher future P/E multiple.

Another View: Earnings Multiple Flags Pricing Risk

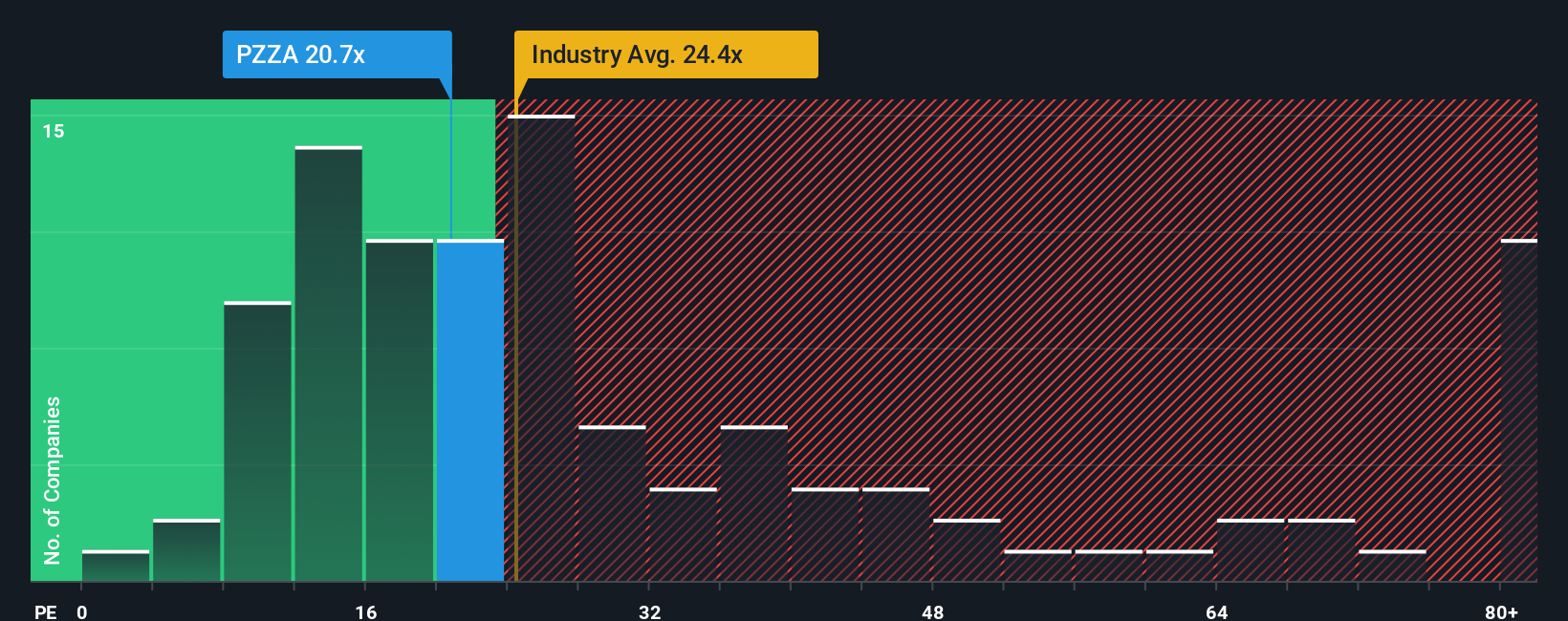

That $47.80 fair value comes from the narrative work, but the P/E picture tells a different story. Papa John’s is on 30.1x earnings, compared with 20.7x for the US Hospitality industry, 22.6x for peers, and a fair ratio of 29.3x. That richer multiple suggests less room for error if profits or sentiment slip, so which signal do you trust more?

Build Your Own Papa John's International Narrative

If you see the data differently or prefer to piece things together yourself, you can build a custom view in minutes with Do it your way.

A great starting point for your Papa John's International research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you are serious about sharpening your portfolio, do not stop at one pizza stock, use the Simply Wall St screener to uncover your next moves.

- Chase value focused opportunities by scanning these 868 undervalued stocks based on cash flows that align with your return expectations and risk comfort.

- Zero in on income potential by reviewing these 11 dividend stocks with yields > 3% that might help you build a steadier stream of payouts.

- Get ahead of the next big theme by checking these 19 cryptocurrency and blockchain stocks that tie equity markets to digital asset trends.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.