A Look At Parsons (PSN) Valuation As Short Term Momentum Cools And Long Term Returns Hold Up

Parsons PSN | 56.00 | -0.23% |

Parsons (PSN) is back in focus for investors after recent share price moves, with the stock closing at $67.52 and mixed returns across the past week, month, and past 3 months attracting closer attention.

Recent trading has cooled after a strong start to the year, with a 1 day share price return of 1.44% and a 7 day share price return of 4.77% offset by a 21.42% 3 month share price decline. The 1 year total shareholder return of 12.92% contrasts with solid 3 and 5 year total shareholder returns of 51.97% and 71.11%. This suggests longer term holders have still seen meaningful gains even as shorter term momentum has faded.

If Parsons recent moves have you reassessing your watchlist, it could be a good time to broaden your search with our screener of 22 top founder-led companies.

With Parsons trading at $67.52 and sitting at an intrinsic discount of about 11% alongside a 26% gap to the average analyst target, you have to ask: is this a genuine entry point, or is the market already baking in future growth?

Most Popular Narrative: 19.7% Undervalued

Parsons most followed narrative pegs fair value at about $84.09 per share compared with the recent $67.52 close, setting up a clear valuation gap for investors to weigh.

Robust funding environment, demonstrated by a record funded backlog (up 14% YoY), strong free cash flow performance, and high win rates on large contracts, combine with secular infrastructure and security demand to underpin both near

and long-term earnings growth and margin stability, despite investor caution or perceived near-term volatility.

Curious what kind of revenue trajectory and margin uplift need to line up for that fair value to hold? The narrative leans on steady contract wins, expanding digital work, and a premium earnings multiple that is not typical for slower growing service names. Want to see how those moving parts fit together into one pricing story?

Result: Fair Value of $84.09 (UNDERVALUED)

However, this story can change quickly if U.S. government funding priorities shift, or if acquisition integration issues keep margins and earnings from matching the current assumptions.

Another Angle On Parsons Valuation

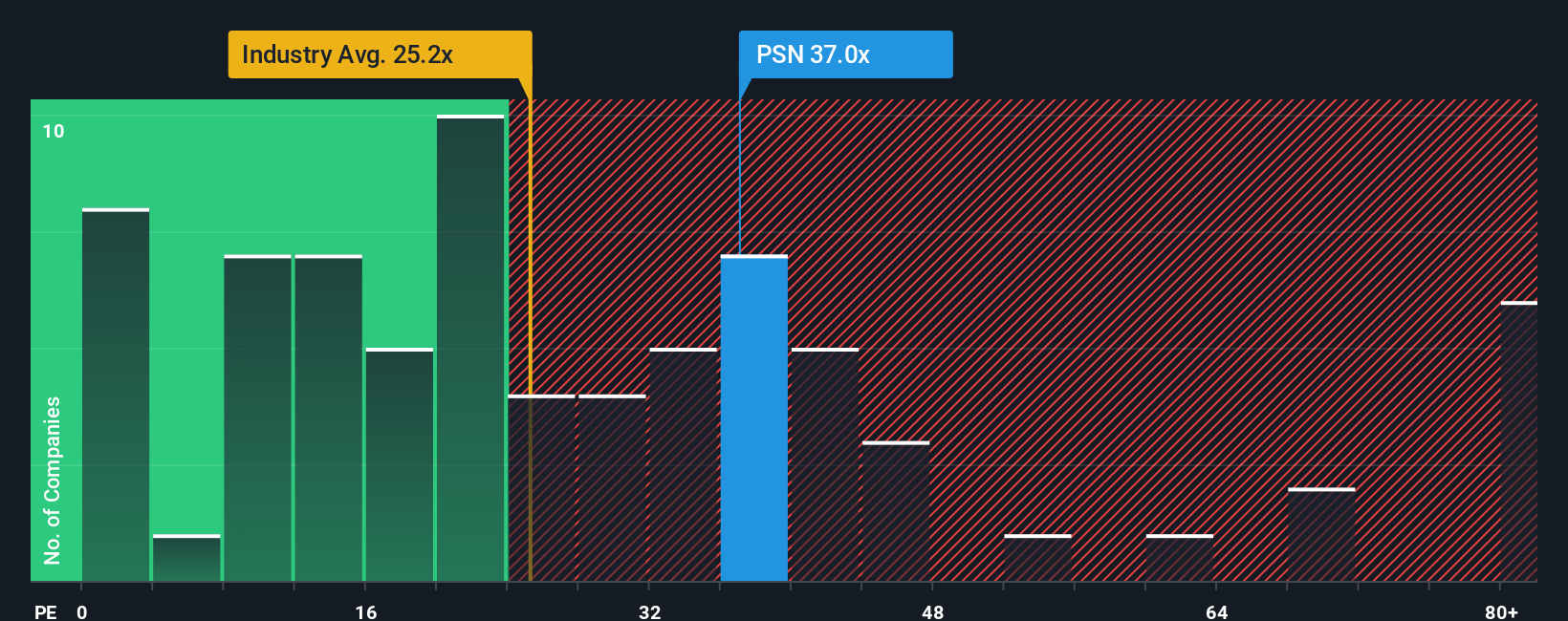

Those fair value and analyst targets point to upside, but the P/E picture tells a more cautious story. Parsons trades on about 30x earnings, above the US Professional Services industry at 21.4x and above its own fair ratio of 24.5x, even though it sits below peer average of 44.9x. That mix of signals raises a simple question: is the market paying too much for quality, or just pricing in what Parsons has already delivered?

Build Your Own Parsons Narrative

If you see the story differently or just prefer to test the numbers yourself, you can shape a complete Parsons view in minutes. To begin, start with Do it your way.

A good starting point is our analysis highlighting 4 key rewards investors are optimistic about regarding Parsons.

Looking for more investment ideas?

If Parsons is on your radar, do not stop there. Broaden your watchlist with other ideas that could suit your style and risk comfort.

- Spot potential value stories early by checking our list of 55 high quality undervalued stocks built from companies with strong fundamentals and room for investors to scrutinize.

- Prioritize resilience by reviewing our solid balance sheet and fundamentals stocks screener (46 results) so you can focus on businesses with sturdier financial footing.

- Hunt for opportunities off the beaten path through our screener containing 25 high quality undiscovered gems that might not yet be widely followed.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.