A Look At Penguin Solutions (PENG) Valuation As New CEO Kash Shaikh Takes The Helm

Penguin Solutions Incorporation PENG | 20.69 | +13.37% |

CEO transition and what it could mean for Penguin Solutions stock

Penguin Solutions (PENG) is in focus after long serving CEO Mark Adams retired from the company and its board, with technology executive Kash Shaikh stepping in as President and Chief Executive Officer.

The CEO transition comes as Penguin Solutions trades at US$19.37, with a 1 day share price return of 3.53% and a 7 day gain of 3.14%, offset by a 1 month share price decline of 4.49%. Over a longer horizon, the total shareholder return shows an 11.19% gain over three years but a 10.07% decline over the past year, suggesting recent momentum has softened even as longer term holders remain ahead.

If leadership change at Penguin has you thinking about where AI infrastructure could go next, it may be worth scanning our list of 34 AI infrastructure stocks as potential ideas to research further.

With Penguin Solutions trading at US$19.37 and flagged as having an intrinsic discount, plus a gap to the average analyst price target, the key question is whether this signals a genuine opening or whether markets are already pricing in future growth.

Most Popular Narrative: 31.4% Undervalued

With Penguin Solutions last closing at $19.37 against a narrative fair value of $28.25, the widely followed view prices in a sizeable upside gap using a 12.3% discount rate.

Expansion of recurring software and managed services (e.g., Penguin ICE ClusterWare and post deployment operations) is raising earnings stability and aggregate profitability, as services revenue is recognized steadily over time and attached to each new customer win.

Curious what earnings path and margin lift have to line up for that valuation to work? The core of this narrative leans heavily on faster profit growth than revenue, and a future earnings multiple that sits well below many peers. The exact mix of growth, profitability and discounting is where the story really gets interesting.

Result: Fair Value of $28.25 (UNDERVALUED)

However, this depends on a business that remains exposed to lumpy Advanced Computing deals and tariff pressure in Optimized LED, both of which could challenge that earnings path.

Another way to look at valuation

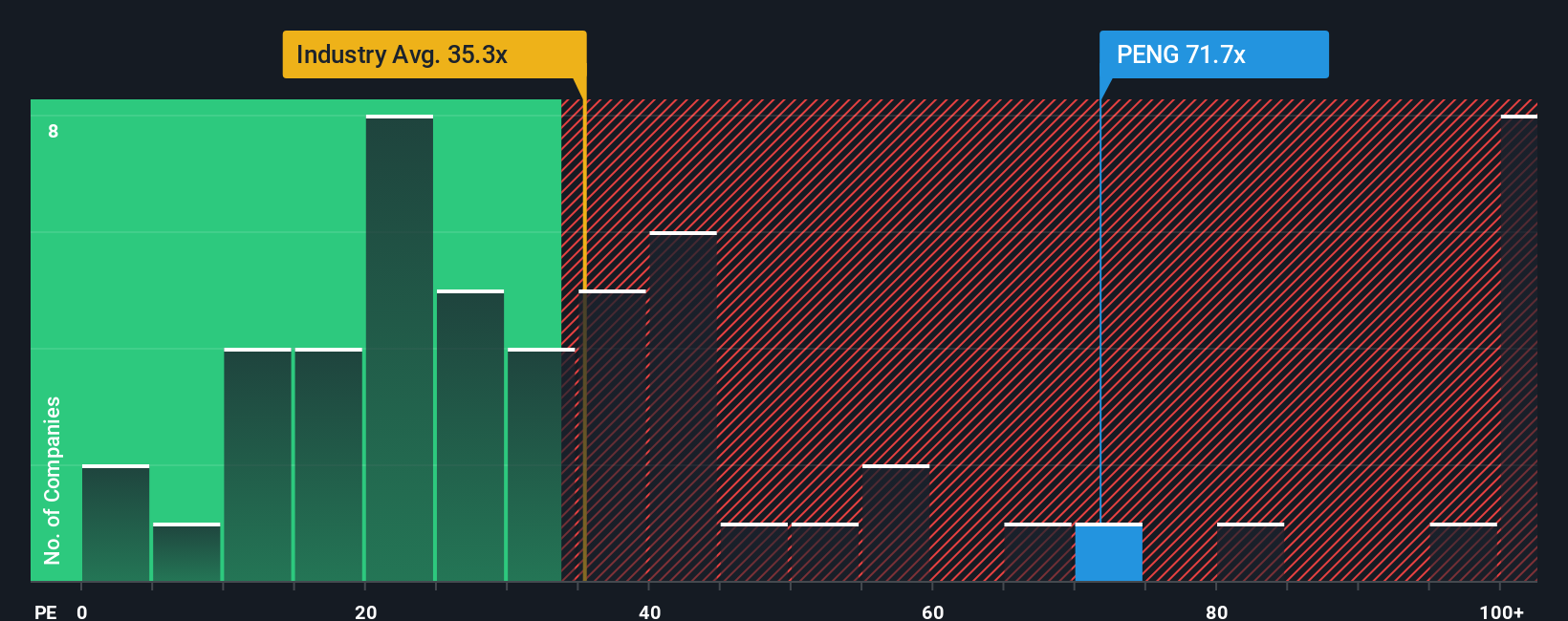

So far the story leans on discounted cash flows and analyst narratives pointing to upside. If you look at the simple P/E instead, the picture is less generous. PENG trades at about 83x earnings, compared with 43.2x for the US semiconductor group, 34.9x for peers, and a fair ratio of 80x. That premium suggests less room for error if the growth story stumbles. Which lens do you feel more comfortable relying on?

Build Your Own Penguin Solutions Narrative

If you look at this and think the assumptions do not quite fit, or you simply prefer to work from the raw numbers yourself, you can build and stress test your own view of Penguin in just a few minutes, starting with Do it your way.

A great starting point for your Penguin Solutions research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you are serious about tightening up your process, do not stop at one stock. Let the screener surface ideas you might otherwise miss.

- Target income first by scanning companies offering robust payouts through our 13 dividend fortresses and see which ones deserve a place on your watchlist.

- Hunt for quality priced below what the numbers suggest with our 53 high quality undervalued stocks and short list candidates for deeper research.

- Cut portfolio stress by focusing on resilient names using the 85 resilient stocks with low risk scores and see which businesses align with your comfort level.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.