A Look At Pool Corporation’s (POOL) Valuation After Expanded Buybacks And Higher Dividend

Pool Corporation POOL | 0.00 |

Pool (POOL) has drawn fresh attention after its board expanded the share repurchase program to US$600.0m and lifted the quarterly dividend by 4% to US$1.30 per share, signaling shareholder friendly capital returns.

Even with the enlarged buyback and higher dividend, Pool’s recent price action has been weak, with a 10.52% 7 day share price return decline and a 30.87% 1 year total shareholder return decline. This points to fading momentum despite steady recent earnings and confirmed 2026 guidance.

If Pool’s latest move has you reassessing your watchlist, this is a good moment to widen the search and look at 18 top founder-led companies

With Pool trading at US$208.09 and sitting at a 24.30% intrinsic discount and 26.26% below the current analyst price target of US$262.73, you have to ask: is this a genuine entry point, or is the market already factoring in its future growth?

Most Popular Narrative: 21.9% Undervalued

With Pool’s fair value estimate at about $266 against a last close of $208.09, the leading narrative frames today’s price as a material discount to its long term earnings potential.

Growing consumer emphasis on home based leisure and wellness is maintaining structurally elevated demand for pools and related services, driving resilient recurring revenue for maintenance and enhancements, which should support top line stability and growth even during new construction lulls.

Curious what earnings path and margin profile underpin that higher fair value? The narrative describes expectations of steady growth, richer profitability, and a premium future earnings multiple. The details may surprise you.

Result: Fair Value of $266 (UNDERVALUED)

However, you also need to weigh housing and construction headwinds, along with Pool’s heavy tilt to mature North American markets, which could cap the long term growth story.

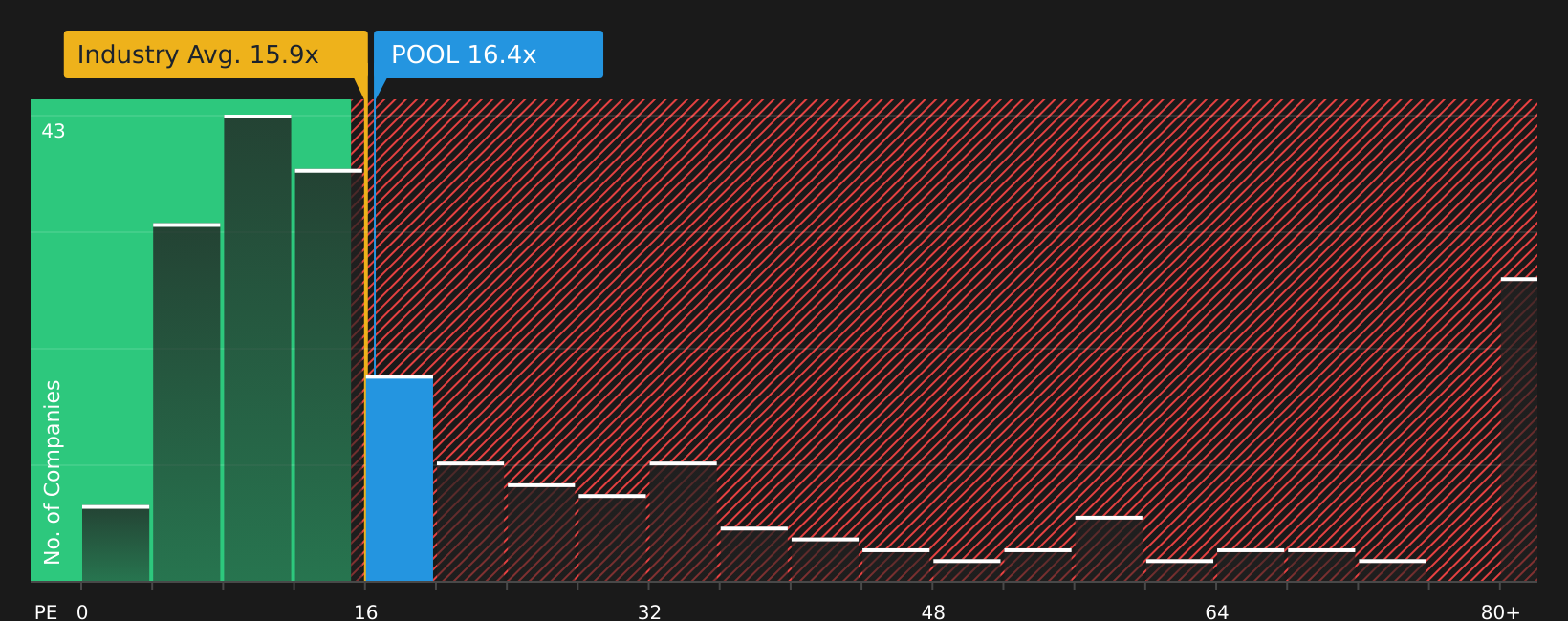

Another View: Earnings Multiple Sends a Different Signal

There is a catch. While the fair value work and SWS DCF model flag Pool as trading at a 24.3% discount to future cash flows, the current P/E of 18.8x sits above the Global Retail Distributors industry average of 16x and the fair ratio of 15.3x, which points to less room for error if earnings disappoint.

This kind of gap can matter in practice, because a move closer to the fair ratio or industry level would mean the share price doing more work than earnings to close that discount. The question is how much valuation risk an investor is really comfortable carrying.

Next Steps

With sentiment mixed across valuation, earnings expectations, and recent share price moves, this is a moment to look at the data yourself and decide where you stand. To see how the trade off between potential upside and known concerns stacks up in one place, review the 4 key rewards and 1 important warning sign

Looking for more investment ideas?

If Pool has your attention, do not stop here. Use the Simply Wall St Screener to uncover fresh opportunities that match the way you like to invest.

- Target consistency by checking out 70 resilient stocks with low risk scores that aim to keep volatility in check while still offering room for returns.

- Spot potential bargains early by scanning screener containing 25 high quality undiscovered gems where solid fundamentals have not yet attracted broad attention.

- Focus on financial strength with solid balance sheet and fundamentals stocks screener (44 results) so you are prioritising companies that might better withstand tougher conditions.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.