A Look At Privia Health Group (PRVA) Valuation After Mixed Recent Share Performance

Privia Health PRVA | 0.00 |

Recent share performance and business context

Privia Health Group (PRVA) has drawn attention after recent share price moves, with the stock down about 1% over the past day and 6% over the past week, yet modestly positive over the past month.

The company operates as a physician enablement platform in the US, reporting annual revenue of US$2.25b and net income of US$21.76m. These figures give investors concrete data to weigh against the recent trading performance.

Set against a mixed recent trading pattern, where the 30 day share price return is 1.74% and the year to date share price return is down 2.98%, the 1 year total shareholder return has declined 9.18%. This points to interest that has cooled over time, even as some shorter term momentum has reappeared.

If you are weighing Privia Health Group against other opportunities in healthcare technology, it can be useful to see how the market is pricing companies building AI enabled tools for clinicians and payers. You can start with 32 healthcare AI stocks

With the stock down over 1 year yet modestly ahead over 3 months, and with an indicated intrinsic discount of about 43%, the key question is whether this is a genuine value gap or whether the market already reflects future growth.

Most Popular Narrative: 28.4% Undervalued

With Privia Health Group last closing at $22.76 against a narrative fair value of $31.80, the current setup centers on how earnings and margins might evolve over time.

The industry wide movement towards value based care, with associated shared savings and care management fees, is enabling Privia to grow its value based attributed lives at a double digit rate and to expand margins as risk sharing agreements mature, positively impacting earnings and long term EBITDA growth.

Curious what sits behind that future earnings jump and higher margin profile. The narrative leans on revenue expansion, profitability uplift and a premium earnings multiple. Want the full picture.

Result: Fair Value of $31.80 (UNDERVALUED)

However, this depends on Privia keeping fee for service collections on track and managing healthcare labor costs, both of which could pressure margins and earnings if they disappoint.

Another angle on valuation

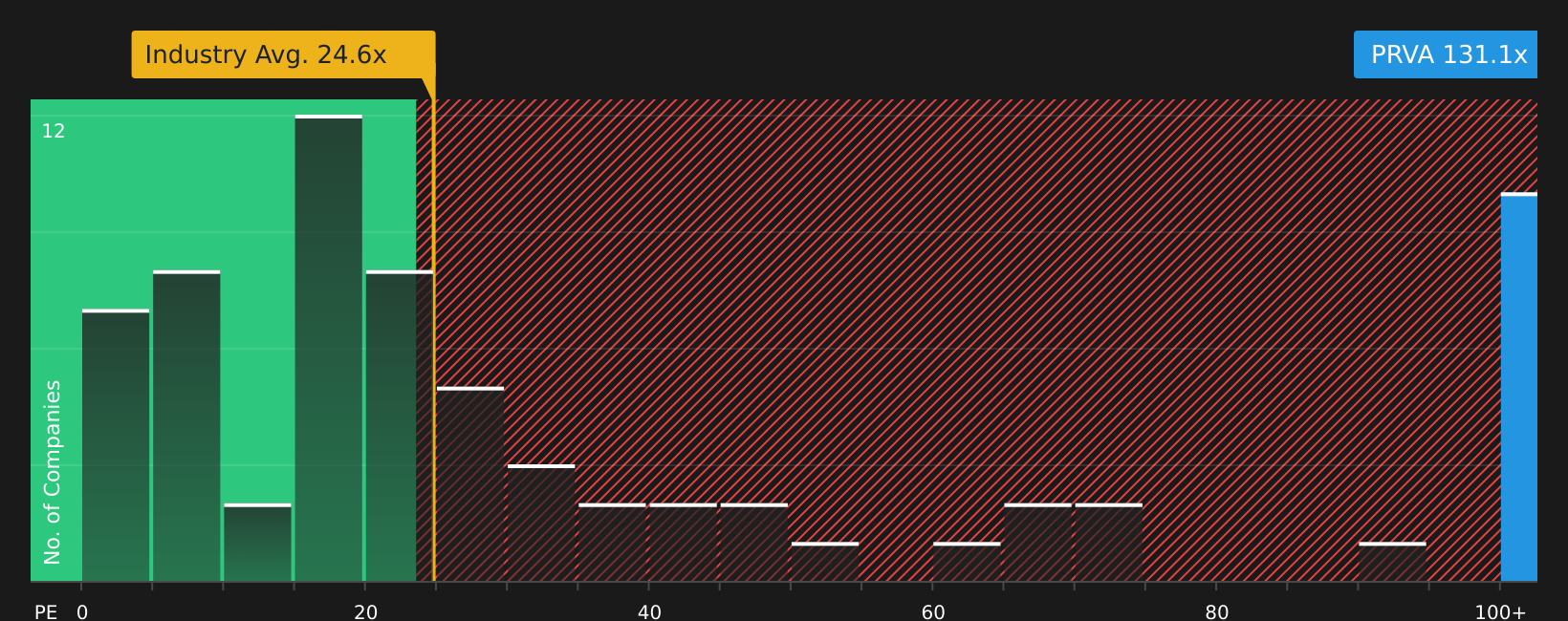

Analysts and the narrative fair value both suggest Privia looks undervalued, yet the current P/E of 131.8x is far above the healthcare industry on 22.1x, the peer average on 53.4x and a fair ratio of 30.4x. That gap points to meaningful valuation risk if expectations cool.

To see how this pricing compares across peers and where the ratio could drift over time, take a closer look at our valuation breakdown, starting with See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With the story so far pointing to both promise and pressure, this is the moment to review the numbers yourself and decide where you stand. You can start with 4 key rewards and 1 important warning sign.

Looking for more investment ideas?

Do not stop with a single stock. Use this moment to broaden your watchlist and stress test your thinking against other high quality opportunities.

- Target potential mispricings by scanning for companies with strong fundamentals that still look overlooked using the 48 high quality undervalued stocks.

- Strengthen your defense by focusing on businesses with resilient finances through the solid balance sheet and fundamentals stocks screener (44 results).

- Get ahead of the crowd by tracking lesser known opportunities that still show solid numbers with the screener containing 21 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.