A Look At Prologis (PLD) Valuation After Analyst Upgrades And Mixed Earnings Expectations

Prologis, Inc. PLD | 133.77 | +0.33% |

Recent analyst upgrades for Prologis (PLD), including a move to Sector Outperform at Scotiabank, are arriving just as the company heads into an earnings report with mixed expectations.

At a share price of $133.21, Prologis has logged a 30 day share price return of 4.01% and a 90 day gain of 7.36%. The 1 year total shareholder return of 26.01% and 5 year total shareholder return of 51.39% point to momentum that has been building rather than fading.

If Prologis has you looking more closely at real assets and income plays, it can be worth widening your search across solid balance sheet and fundamentals stocks screener (None results) to see what else stands out.

With the stock near recent analyst targets, a 1.98% discount to the US$135.85 consensus price, and solid multi year returns already on the board, you have to ask: is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 10% Undervalued

With Prologis last closing at $133.21 against a narrative fair value of $133.40, the story here hinges more on earnings quality and long run assumptions than on any big headline discount.

Limited new supply and a significant spread between market and replacement cost rents (over 20%), combined with a depleting development pipeline, position Prologis for future periods of robust rent growth and improved net operating income as market vacancy normalizes and pricing power returns.

Curious what kind of long term rent growth, margins, and earnings multiple are baked in to reach that fair value? The narrative leans on measured growth, richer profitability, and a premium P/E far above the wider industrial REIT group. Want to see exactly which assumptions have to hold for that to stack up?

Result: Fair Value of $133.40 (ABOUT RIGHT)

However, that story can shift quickly if slower leasing and elevated vacancy persist, or if bad debt and weaker energy incentives squeeze margins more than expected.

Another Angle on Valuation

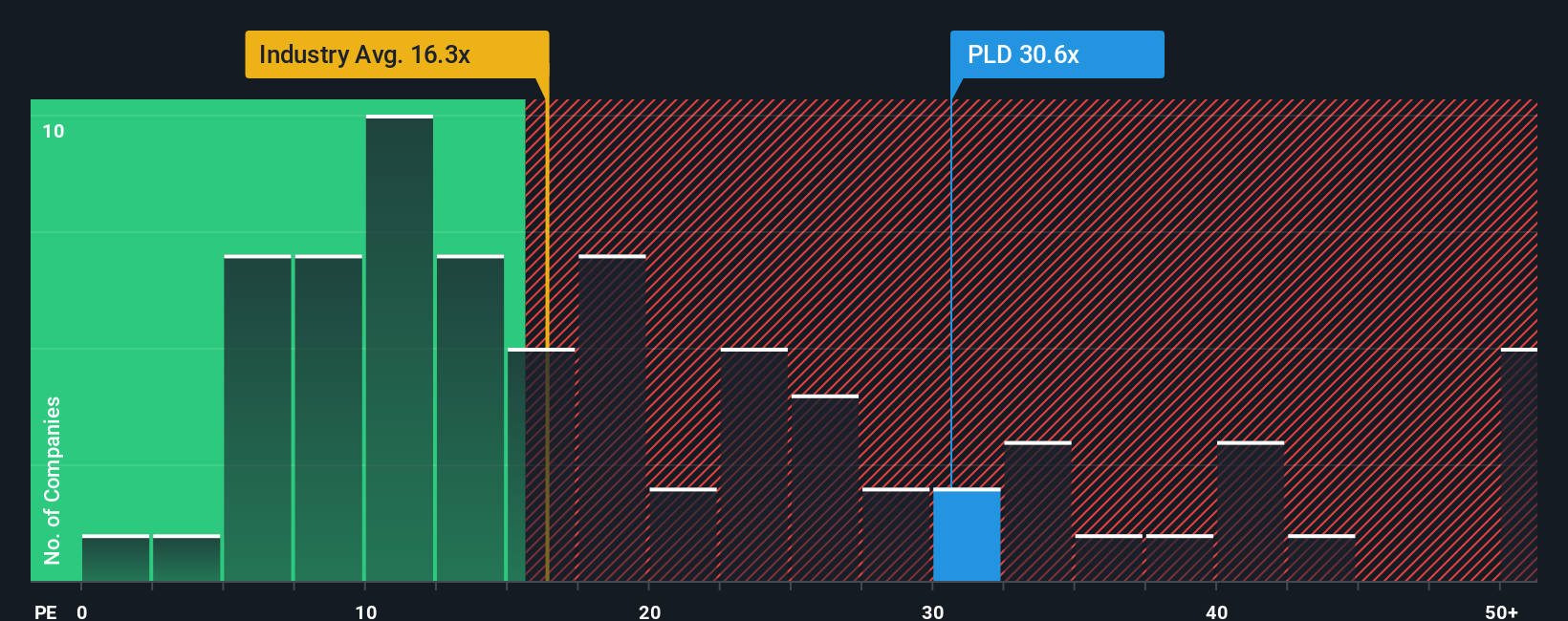

That narrative fair value of US$133.40 lines up almost exactly with where Prologis trades today, but the P/E ratio tells a tighter story. At 38.6x, it sits well above the global Industrial REITs average of 16.3x, the peer average of 33x, and even the Simply Wall St fair ratio of 34.1x.

In practice, that means the market already asks you to pay a clear premium for Prologis earnings, with less room for disappointment if growth or margins come in softer than expected. The question is, do you think the business quality and long term logistics demand justify that premium, or would you rather wait for a gap to open up?

Build Your Own Prologis Narrative

If you look at the numbers and come to a different conclusion, or prefer to test the assumptions yourself, you can build a custom view in minutes with Do it your way.

A great starting point for your Prologis research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you stop at one stock, you might miss something important. Use the Screener to line up a few fresh ideas that genuinely earn a spot on your list.

- Explore potential under the radar opportunities by checking out these 3531 penny stocks with strong financials that pass quality and financial strength filters.

- Consider the role of machine learning and automation with these 24 AI penny stocks that are already tied to real world use cases.

- Review potential mispriced opportunities among these 863 undervalued stocks based on cash flows where current prices sit below estimated cash flow based fair values.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.