A Look At Public Storage (PSA) Valuation After Bank Of America’s Downgrade And Sector Headwinds

Public Storage PSA | 280.35 | +1.49% |

Public Storage (PSA) is back in focus after Bank of America shifted its rating from Buy to Neutral, citing a lack of near term operational catalysts and macro pressures on storage demand.

The recent downgrade comes after a period where momentum has been steady rather than explosive, with an 11.05% year to date share price return contrasted against a 1 year total shareholder return of a 1.16% decline. This hints at mixed sentiment around future growth and income potential despite Public Storage’s scale in self storage.

If this shift in tone on storage has you thinking about where else capital might work harder, it could be a good moment to check out 22 top founder-led companies as a fresh source of ideas.

With shares up 11.05% year to date, but the 1-year total return still showing a 1.16% decline and an indicated intrinsic discount of 37.91%, you have to ask: is this a reset opportunity, or is the market already pricing in future growth?

Most Popular Narrative: 7.2% Undervalued

With Public Storage last closing at $287 and the most followed narrative pointing to a fair value of about $309.22, the gap between price and story is clear enough to warrant a closer look at what is driving that view.

Strategic portfolio expansion, including $1.1 billion in recent acquisitions/development and successful lease-up of new and non-same-store assets, is expected to drive future revenue and NOI growth, positioning the company to benefit from ongoing industry consolidation and market share gains.

Want to see what kind of revenue growth, margin trajectory, and future P/E multiple have been baked into that fair value? The most followed narrative ties together storage demand trends, expansion spending, and earnings power in a way that may surprise you, especially when you line those assumptions up against today’s price and the current self storage cycle.

Result: Fair Value of $309.22 (UNDERVALUED)

However, there are still real pressure points here, including oversupply in key storage markets and rising costs for tax, insurance, and utilities that could squeeze margins if conditions soften.

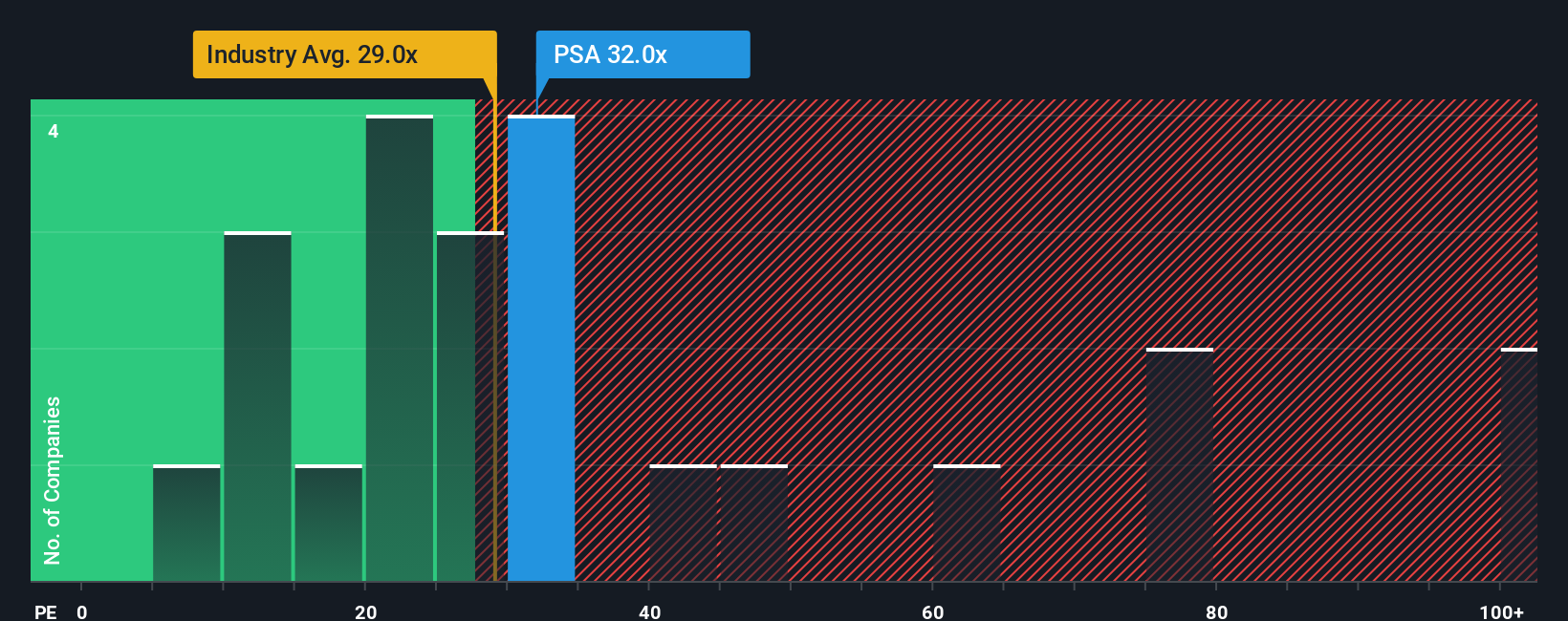

Another View: What The P/E Says

The narrative and intrinsic workup suggest Public Storage may be trading 37.9% below an estimated fair value. The current P/E of 29.7x sits above the North American Specialized REITs average of 26x and below a reference ratio of 34x. This raises the question of whether the current level represents a margin of safety or a potential value trap if sentiment weakens.

Build Your Own Public Storage Narrative

If you look at these numbers and come to a different conclusion, or simply want to test your own assumptions, you can build a custom narrative. Start from a blank canvas and shape the story your way with Do it your way.

A great starting point for your Public Storage research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If you are serious about putting your capital to work, do not stop at one storage REIT when the wider market is full of very different opportunities.

- Spot potential mispricing early by scanning our list of 52 high quality undervalued stocks that combine attractive pricing with quality fundamentals.

- Strengthen your income stream by reviewing 14 dividend fortresses, focused on higher yielding names built around more stable payout profiles.

- Sleep a little easier by checking 82 resilient stocks with low risk scores, where business quality and risk scores help you avoid surprises.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.