A Look At Regency Centers (REG) Valuation After Strong Results Guidance And Dividend Reaffirmation

Regency Centers Corporation REG | 79.57 79.57 | +1.58% 0.00% Pre |

Regency Centers (REG) just paired record same property NOI growth and high shop occupancy with fresh 2026 earnings guidance and reaffirmed dividends, giving investors a new data point for assessing the REIT’s current valuation.

At a share price of $75.22, Regency Centers has paired its recent earnings, 2026 guidance and dividend affirmations with firm momentum, including a 7.5% 30 day share price return and a 10.7% year to date share price return, while its 5 year total shareholder return of 74.7% reflects a much longer period of value creation.

If this kind of steady REIT story has you thinking about where else capital might compound, it could be worth scanning our 22 top founder-led companies as a fresh source of ideas.

With REG now trading near its recent highs and sitting at a reported 24% intrinsic discount, the real question is whether investors are still getting underappreciated value here or whether the market is already baking in future growth.

Most Popular Narrative: 6% Undervalued

With Regency Centers last closing at $75.22 against a widely followed fair value view of about $80, the current setup hangs on a handful of key operating assumptions.

Regency's proactive capital deployment in high barrier to entry suburban markets (e.g., recent South Orange County acquisition and robust development/redevelopment pipeline) allow the company to capture higher rents, drive NOI growth, and grow NAV, with future earnings leverage from incremental projects as supply remains constrained.

Curious what earnings power that kind of pipeline implies. The narrative leans on steady revenue gains, fatter margins, and a richer profit multiple. The exact mix of those three inputs is what underpins that higher fair value.

Result: Fair Value of $80.05 (UNDERVALUED)

However, that upside case can fray quickly if grocery anchor health weakens, or if development and redevelopment projects demand more capital and face rising construction or regulatory costs.

Another View: Market Pricing Looks Full

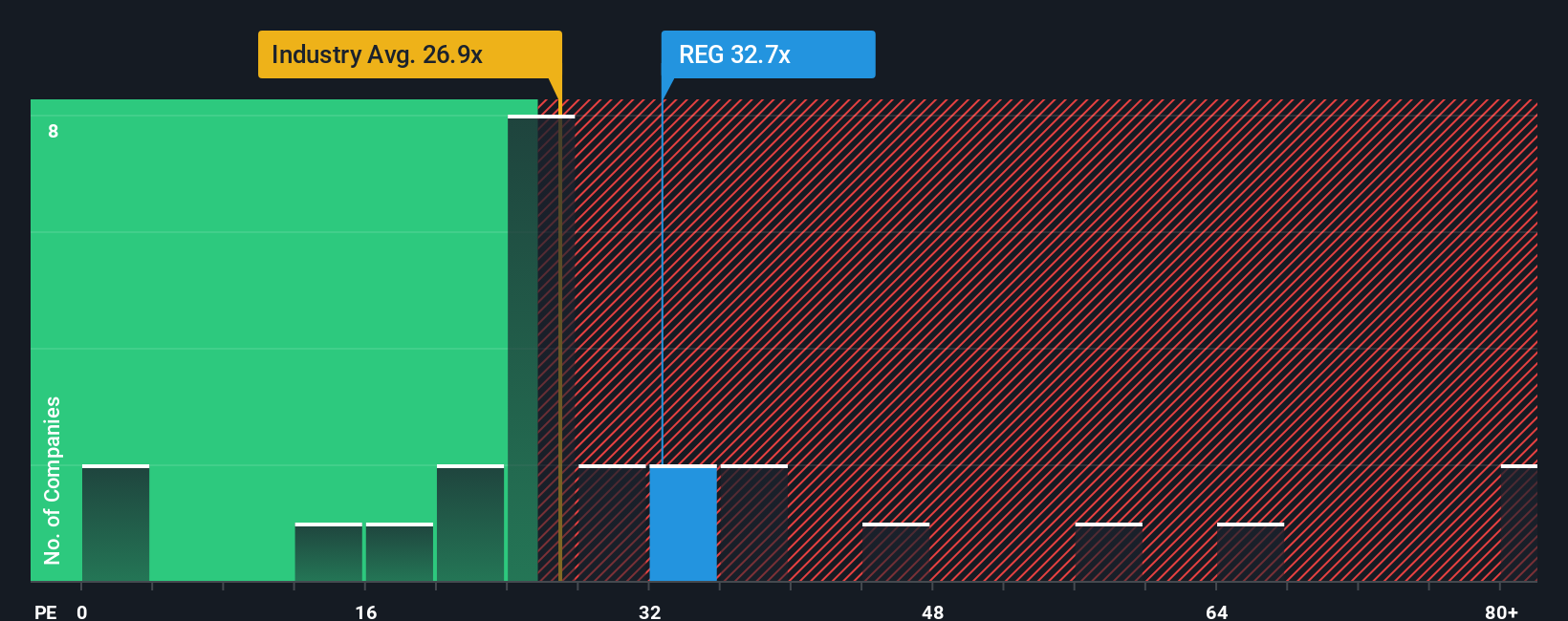

That 6% undervaluation story sits uncomfortably next to how the market is actually pricing Regency Centers today. The shares trade on a P/E of 34.5x, compared with 30.4x for the US Retail REITs industry, 25.1x for peers, and a fair ratio of 33.7x.

In plain terms, you are already paying a premium to both the sector and close comparables, with only a small gap to the fair ratio. That leaves less room for error if growth or margins track closer to the lower end of expectations. How much premium are you personally willing to pay for perceived quality and consistency here?

Build Your Own Regency Centers Narrative

If you see the numbers differently or prefer to stress test your own assumptions, you can build a complete Regency narrative yourself in just a few minutes: Do it your way

A great starting point for your Regency Centers research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If you are serious about putting your capital to work, do not stop at one REIT story when a few targeted screens could surface better aligned opportunities.

- Spot potential value by scanning companies our screener flags as 53 high quality undervalued stocks and see which names match your return expectations and risk comfort.

- Prioritise resilience by focusing on businesses highlighted in our solid balance sheet and fundamentals stocks screener (45 results) that may handle tougher conditions with more balance sheet flexibility.

- Get ahead of the crowd by reviewing companies surfaced in our screener containing 25 high quality undiscovered gems before they hit everyone else’s radar.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.