A Look At RLI Corp (RLI) Valuation After A Year Of Weaker Share Price Performance

RLI Corp. RLI | 0.00 |

Recent Performance Snapshot

RLI Corp (RLI) has drawn attention after a period where the stock is down about 27% over the past year, with returns also weaker over the past 3 months and year to date.

At a last close of US$50.35 and a market value of about US$4.6b, the insurer combines property, casualty and surety operations, supported by US$1.9b in revenue and US$395.0m in net income.

RLI’s recent share price slide, including an 18.4% decline over the past 90 days and a weaker year to date, contrasts with a still positive 5 year total shareholder return of 22.26%. This suggests that momentum has faded after earlier gains.

If this shift in sentiment has you reassessing your portfolio, it could be a good moment to look beyond insurers and check out 21 top founder-led companies

With RLI stock down sharply over the past year and trading at an estimated 11.4% discount to an intrinsic value model, you have to ask: is there a genuine opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 13.2% Undervalued

At a last close of US$50.35 versus a narrative fair value of US$58.00, the current price sits below what this widely followed model implies.

RLI's increased investments in technology, digital tools, and higher acquisition expenses, while intended to improve future efficiency, are currently contributing to a higher expense base. If these investments do not generate commensurate growth or savings, expense ratios could remain elevated and compress net margins.

The valuation story depends on a tight balance between softer revenue assumptions, slimmer margins, and a richer earnings multiple. Readers may be interested in which of these levers really carries the model, and how much pressure they put on future profitability to make US$58.00 hold up.

Result: Fair Value of $58 (UNDERVALUED)

However, there is still a real risk that higher catastrophe claims and ongoing pressure from acquisition and reinsurance costs could leave profit margins tighter than analysts expect.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another View On Valuation

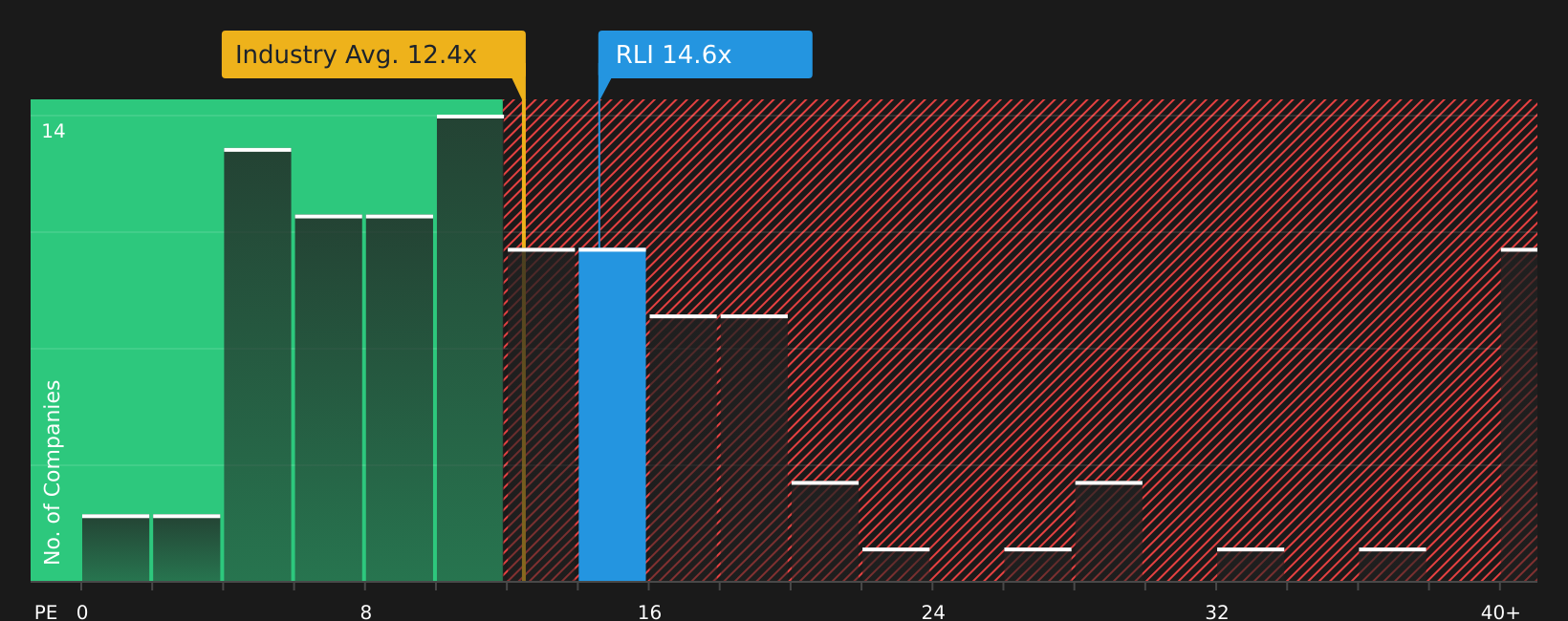

The earlier narrative frames RLI as about 13.2% undervalued relative to a fair value of US$58.00. However, the current P/E of 11.7x sits above the US Insurance industry at 10.3x, the peer average at 9.3x, and an estimated fair ratio of 8.2x. This points to valuation risk rather than a clear bargain. Which signal do you treat as more important when pricing that risk?

To unpack this earnings based view in more detail and see how it compares across peers, check the fuller valuation breakdown, including the fair ratio context, in the See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment clearly mixed, it helps to see the numbers for yourself and decide where you stand before the market moves on. To weigh both sides of the story in one place, take a look at the 2 key rewards and 2 important warning signs.

Looking for more investment ideas?

If RLI has you rethinking where your money works hardest, do not stop here, use this moment to scan other opportunities before the market moves first.

- Target quality at a discount by checking companies that look attractively priced with 47 high quality undervalued stocks

- Strengthen your income stream by reviewing stocks that may offer higher yields and resilient payouts with 10 dividend fortresses

- Prioritise capital preservation by focusing on companies with steadier profiles using the 65 resilient stocks with low risk scores

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.